Analysis

September 17, 2013

NAFTA Automotive Production

Written by Peter Wright

NAFTA Automotive production in August rebounded to 1.436 million units after the summer shut down. The annual rate in August was 17.243 million units. On a rolling 12 month basis production was 15.719 million units, up 5.9 percent from the 12 months through August a year ago. Growth has been slowing as production approached then equaled the pre-recession level of 2004 through 2006 (Figure 1).

Production share of the three NAFTA members has been changing for 2 ½ years. The US share has been trending up, Canada has been trending down and Mexico has been erratically flat (Figure 2). The Detroit big 3 production share in August 2013 was 52.6 percent, the same as in August 2012.

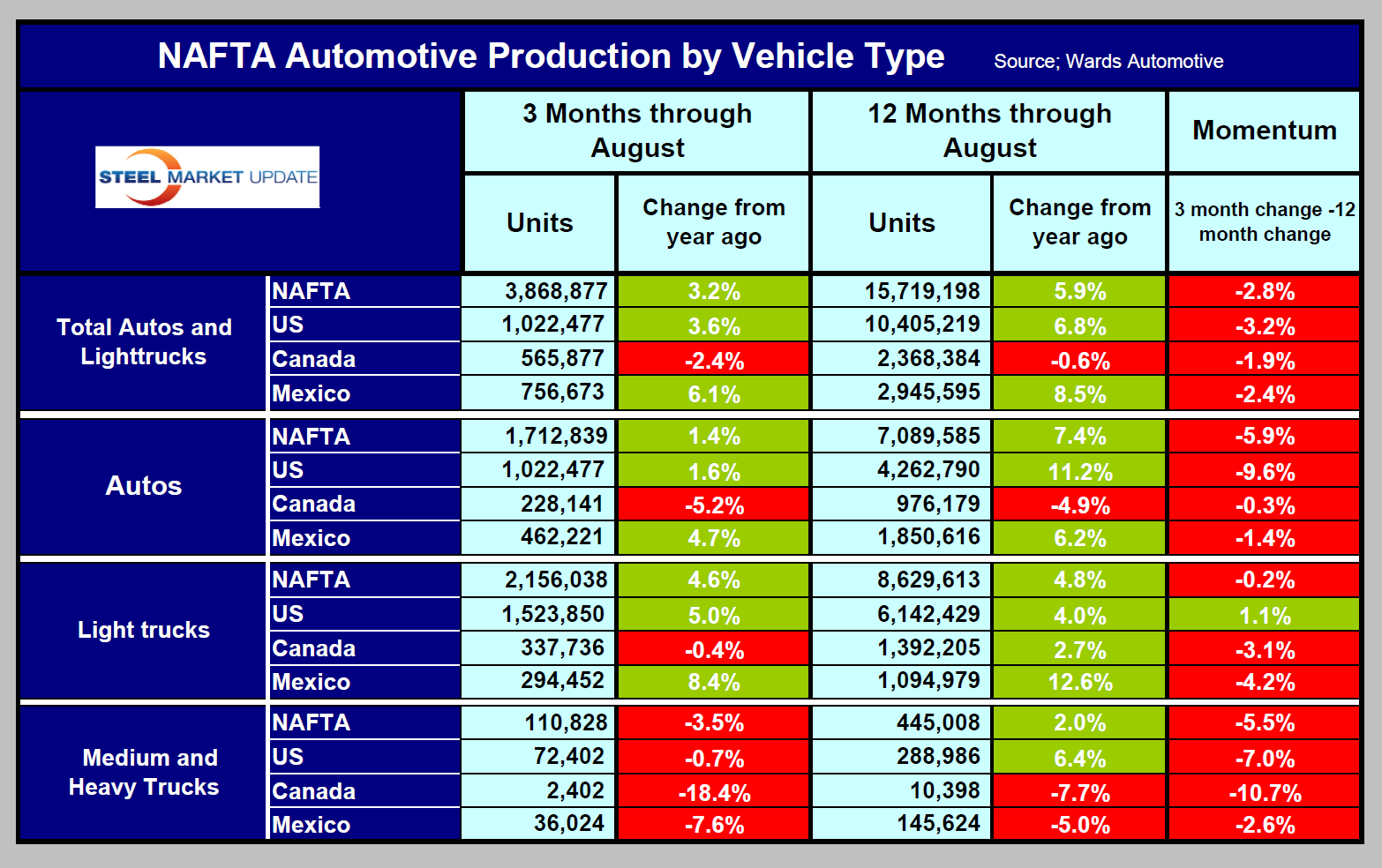

In 12 months through August year / year, US total light vehicle production was up by 6.8 percent, Mexico up by 8.5 percent and Canada down by 0.6 percent. There has been a change in product mix between the US and Mexico with US growth favoring autos as Mexico has favored light trucks (Table 1). Canada had negative growth in autos but eked out a small gain in light trucks. The trend reported previously by SMU in which the automotive companies are downplaying Canadian production continued through August.

Automotive sales in the US increased to 16.1 million units in August. Year-to-date sales are averaging 1 million units higher than the average for 2012. The average age of vehicles reached a record high in 2012 and pent up demand is being alleviated. Also technological improvements, particularly in fuel economy are contributing to stronger sales. Sales are expected to reach 15.5 million units for the year. The release of pent-up demand will drive sales through the end of 2014, when sales are expected to hit 17 million units before coming down to a more sustainable pace of about 15.5 million units.

{kind=link}

{kind=link}