Prices

April 28, 2014

March Raw Steel Production

Written by John Packard

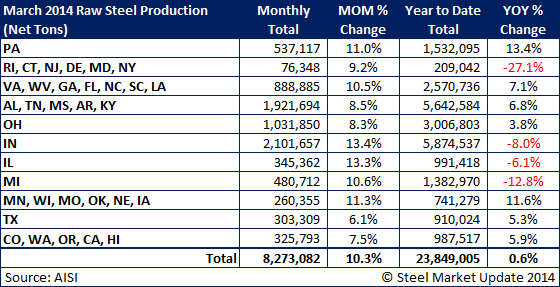

According to the American Iron and Steel Institute (AISI) domestic raw steel production totaled 8,273,082 net tons (all products). Of the total 60 percent was produced by electric arc furnaces and the balance by blast/BOF furnaces. Carbon steel products totaled 7,681,790 net tons with 4,665,056 tons being produced by EAF’s and the balance, 3,016,734 tons by fully integrated mills.

Through the first three months 2014 total steel production was 23,849,005 tons (all products). Carbon steel products totaled 22,100,611 tons, and increase of 95,455 tons more than the first three months 2013.

Capacity utilization rates for the month of March were adjusted to 77.7 percent and for the year, 77.1 percent.

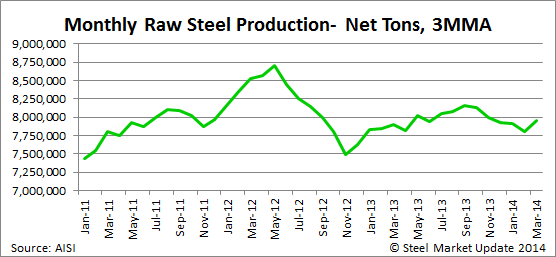

Below is a graph showing the monthly production levels on a three month moving average. After following a downward slope since September 2013, production levels increased in March to an average of 7,949,668 tons