Prices

January 11, 2015

Scrap exports for First 11 Months 2014 Down 15.7%

Written by Peter Wright

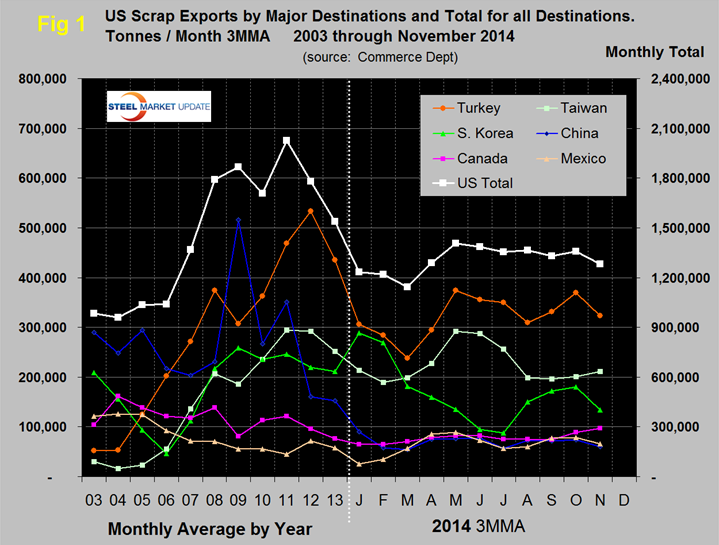

In the first eleven months of 2014, scrap exports totaled 14,251,000 tonnes (metric tons), down by 15.7 percent from the same period in 2013. In the single month of November exports were 1,347,000 tonnes, almost unchanged from October. Figure 1 shows that the three month moving average has been declining slightly for the last seven months though unusually consistent during that time and continued to be lower than the average in any year from 2008 through 2013.

The most obvious trends so far this year has been that Taiwan and Korea have been almost mirror images of each other. Turkey’s tonnage picked up in October then declined by 56% in November. The 3MMA of Turkey’s receipts have been fluctuating in a fairly narrow range for the last seven months. Year to date Turkey is down by 1.357 million tonnes or 28.7 percent. China’s tonnage has been quite consistently low this year on a 3MMA basis ranging from 53,000 to 90,000 tonnes per month. This is compared to over 500,000 tonnes per month in 2009 when they were the highest volume importer.

Shipments to secondary buying nations in November were the highest of the year with a total of 211,000 tons. Almost 70% of this went to the Middle-east with 16,000 tonnes to Bahrain, 43,000 tonnes to Kuwait and 78,000 tonnes to Saudi Arabia.

The November results confirm AMM’s report on November 25th when they wrote that scrap exporters just suffered another dismal week as demand and bid prices from major buyers remained weak. No bulk sales were reported into Turkey or Asia in the latest week which means that US exporters have sold only three cargoes in the first three weeks of November, two to South Korea and one to Turkey.

In YTD 2014 compared to the same period in 2013, the Far East as a whole is now down by only 0.3 percent as increases to Indonesia and Thailand have balanced the decreases to China, Malaysia and South Korea. The decline of the Japanese Yen is a big factor in Far East trade in general though at this point we don’t know to what extent it is influencing international scrap trade. Some nations have taken more tonnage this year than last, Indonesian purchases are up by 85% and Thailand which took almost nothing last year has received over four times as much US scrap this year as it did in 2013,

Mexico is up by 54,000 tonnes and Vietnam by 114,000 tons. Tonnage moving North over the Canadian border in November at 109,000 tonnes was the highest of the year and YTD was up by 5.5 percent from last year.

Scrap export prices are reported by the AMM every Tuesday for an 80:20 mix of #1 and #2 heavy melt in US $ per tonne FOB New York and Los Angeles for bulk tonnage sales. Prices on the both coasts were in free fall from August 25th until November 10th but in the eight weeks through January 5th prices on the West coast have remained unchanged at $277.50 as prices on the east coast after being flat from November 10th until December 15th have since climbed by $18 to $299.47. On January 5th shredded FOB the East coast was $20.94 below Chicago.