Prices

November 8, 2015

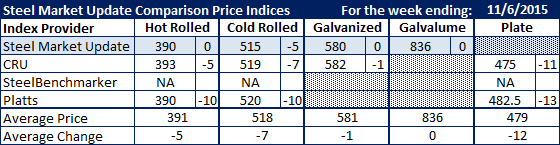

Comparison Price Indices: SMU, CRU and Platts

Written by John Packard

The various flat rolled steel indexes followed by Steel Market Update are falling in line and reporting hot rolled, cold rolled, galvanized and plate prices the same. We find this interesting as the various steel price collection techniques are slightly different from one another. Could this be a harbinger that flat rolled prices are close to a bottom (or just a coincidence)?

Over the past few months there have been discrepancies between the various indexes although there have been no doubts as to the direction prices were headed. This past week the indexes followed by Steel Market Update (SMU) and that reported flat rolled steel prices last week were within a few dollars of each other on all flat rolled and plate products.

Benchmark hot rolled coil (prior to any extras or freight) price averages ranged from $390 per ton ($19.50/cwt) at SMU and Platts to a high of $393 per ton at CRU. SteelBenchmarker did not report prices this past week as they only report twice per month.

Cold rolled prices dropped on all three indices with SMU the lowest at $515 per ton followed by CRU ($519) and Platts ($520).

Galvanized prices barely budged last week with SMU reporting .060” G90 galvanized as averaging $580 per ton with CRU at $582 per ton for the same product.

Galvalume prices for .0142” AZ50, Grade 80 remained the same last week at $836 per ton.

The variance between Platts and CRU on plate shrunk last week. CRU was down $11 to $475 per ton while Platts dropped from $495 to $482.50 per ton (we round up to $483 in our CPI table).

FOB Points for each index:

SMU: Domestic Mill, East of the Rockies.

CRU: Midwest Mill, East of the Rockies.

SteelBenchmarker: Domestic Mill, East of the Mississippi.

Platts: Northern Indiana Domestic Mill.

Note that SteelBenchmarker produces numbers twice per month. On the weeks they produce numbers we will include them in the average. The weeks where they do not produce numbers (NA = not available) we will not include their outdated numbers in the CPI average.