Prices

September 6, 2016

SMU Price Ranges & Indices: Minor Tweaks After Last Weeks Big Move

Written by John Packard

Due to our Steel Summit Conference last week we did not produce our price ranges and averages until Thursday (September 1st). Since then there has been very little movement but we did tweak galvanized and Galvalume numbers slightly. We will be watching to see if the pace of price erosion gains traction from here or if the mills are able to fill their order books without further bloodletting.

Here is how we see prices this week:

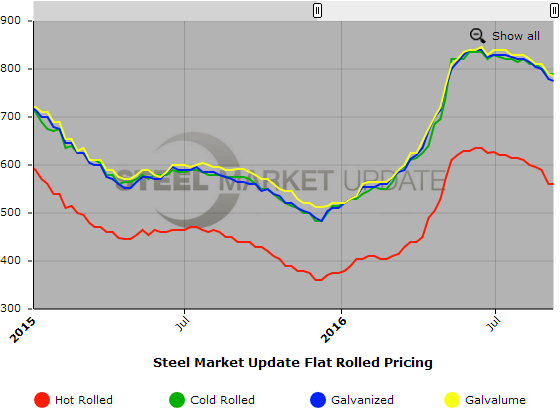

Hot Rolled Coil: SMU Range is $530-$590 per ton ($26.50/cwt- $29.50/cwt) with an average of $560 per ton ($28.00/cwt) FOB mill, east of the Rockies. Both the lower and upper ends of our range remained the same compared to last week. Our overall average is unchanged over last week. Our price momentum on hot rolled steel is for prices to trend lower over the next 30 days.

Hot Rolled Lead Times: 2-5 weeks

Cold Rolled Coil: SMU Range is $770-$810 per ton ($38.50/cwt- $40.50/cwt) with an average of $790 per ton ($39.50/cwt) FOB mill, east of the Rockies. Both the lower and upper ends of our range remained the same compared to last week. Our overall average is unchanged over last week. Our price momentum on cold rolled steel is for prices to trend lower over the next 30 days.

Cold Rolled Lead Times: 4-7 weeks

Galvanized Coil: SMU Base Price Range is $37.50/cwt-$40.00/cwt ($750-$800 per ton) with an average of $38.75/cwt ($775 per ton) FOB mill, east of the Rockies. The lower end of our range decreased $10 per ton compared to one week ago while the upper end remained the same. Our overall average is down $5 over last week. Our price momentum on galvanized steel is for prices to trend lower over the next 30 days.

Galvanized .060” G90 Benchmark: SMU Range is $810-$860 per net ton with an average of $835 per ton FOB mill, east of the Rockies.

Galvanized Lead Times: 2-8 weeks

Galvalume Coil: SMU Base Price Range is $38.00/cwt-$40.50/cwt ($760-$810 per ton) with an average of $39.25/cwt ($785 per ton) FOB mill, east of the Rockies. The lower end of our range decreased $10 per ton compared to last week while the upper end remained the same. Our overall average is down $5 over one week ago. Our price momentum on Galvalume steel is for prices to trend lower over the next 30 days.

Galvalume .0142” AZ50, Grade 80 Benchmark: SMU Range is $1051-$1101 per net ton with an average of $1076 per ton FOB mill, east of the Rockies.

Galvalume Lead Times: 4-8 weeks

SMU Note: Below is a graphic showing our hot rolled, cold rolled, galvanized, and Galvalume price history. To use the graphs interactive capabilities, you must view it on our website here. If you need help navigating the website or need to know your login information, contact us at info@SteelMarketUpdate.com or by calling 800-432-3475.