Prices

November 22, 2016

SMU Price Ranges & Indices: Still Moving, Even During Holiday Week

Written by John Packard

Flat rolled steel prices continue to move as the steel buyers absorb the three increases announced by the domestic steel mills going back to October 21st. Most buyers are telling Steel Market Update that this week is relatively quiet due to the Thanksgiving Holiday but the mill remain steadfast in their resolve to garnish higher prices on hot rolled, cold rolled, galvanized and Galvalume steel products. As one service center executive put it to SMU earlier today, “They [steel mills] are showing no mercy with these price increases.” They went on to say that with the new administration being sympathetic to the steel industry the expectation has to be for even higher prices as we move into 2017.

Here is how we see prices this week:

Hot Rolled Coil: SMU Range is $510-$580 per ton ($25.50/cwt- $29.00/cwt) with an average of $545 per ton ($27.25/cwt) FOB mill, east of the Rockies. The lower end of our range declined $10 per ton over one week ago while the upper end increased $20 per ton. Our overall average is up $5 per ton over last week. Our price momentum on hot rolled steel has been adjusted to Higher which means that prices are expected to move higher over the next 30-60 days.

Hot Rolled Lead Times: 2-5 weeks

Cold Rolled Coil: SMU Range is $710-$780 per ton ($35.50/cwt- $39.00/cwt) with an average of $745 per ton ($37.25/cwt) FOB mill, east of the Rockies. The lower end of our range decreased $10 per ton over last week while the upper end rose $20 per ton. Our overall average is up $5 per ton over one week ago. Our price momentum on cold rolled steel has been adjusted to Higher which means that prices are expected to move higher over the next 30-60 days.

Cold Rolled Lead Times: 4-8 weeks

Galvanized Coil: SMU Base Price Range is $37.00/cwt-$39.50/cwt ($740-$790 per ton) with an average of $38.25/cwt ($765 per ton) FOB mill, east of the Rockies. The lower end of our range rose $20 per ton over one week ago while the upper end increased $30 per ton. Our overall average is up $25 per ton over last week. Our price momentum on galvanized steel has been adjusted to Higher which means that prices are expected to move higher over the next 30-60 days.

Galvanized .060” G90 Benchmark: SMU Range is $809-$859 per net ton with an average of $834 per ton FOB mill, east of the Rockies. Note that the USS price extra we use for this product has increased from $60 per ton in extras to $69 per ton.

Galvanized Lead Times: 4-9 weeks

Galvalume Coil: SMU Base Price Range is $37.00/cwt-$39.50/cwt ($740-$790 per ton) with an average of $38.25/cwt ($765 per ton) FOB mill, east of the Rockies. The lower end of our range increased $20 per ton over last week while the upper end increased $30 per ton. Our overall average is up $25 per ton over one week ago. Our price momentum on Galvalume steel has been adjusted to Higher which means that prices are expected to move higher over the next 30-60 days.

Galvalume .0142” AZ50, Grade 80 Benchmark: SMU Range is $1031-$1081 per net ton with an average of $1056 per ton FOB mill, east of the Rockies.

Galvalume Lead Times: 4-7 weeks

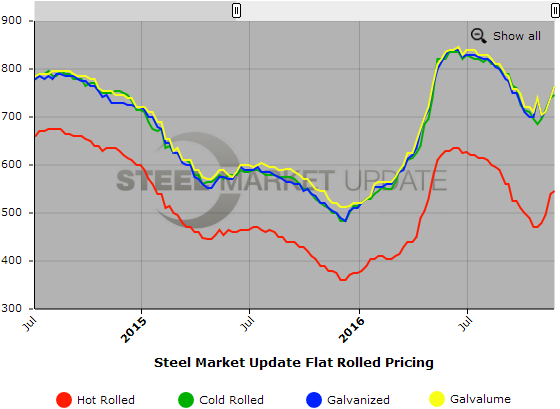

SMU Note: Below is a graphic showing our hot rolled, cold rolled, galvanized, and Galvalume price history. To use the graphs interactive capabilities, you must view it on our website here. If you need help navigating the website or need to know your login information, contact us at info@SteelMarketUpdate.com or by calling 800-432-3475.