Prices

December 27, 2016

SMU Price Ranges & Indices: Minor Adjustments

Written by John Packard

The data collected late last week and through the day today was spotty at best. However, we feel confident from the numbers we were able to collect to make some minor adjustments in our hot rolled and cold rolled indices. With the Holiday Week upon us SMU does not anticipate another round of price increases until the New Year. With the mill offers pushing the upper ranges (and in some case exceeding the upper ranges) of the last guidance numbers provided by the mills, another increase should come as no surprise.

We expect the next increase could be in the $40 to $50 per ton range based on what we are hearing out of the scrap dealers. Negotiations should begin in earnest as soon as the New Year Holiday is behind us.

Here is how we see prices this week:

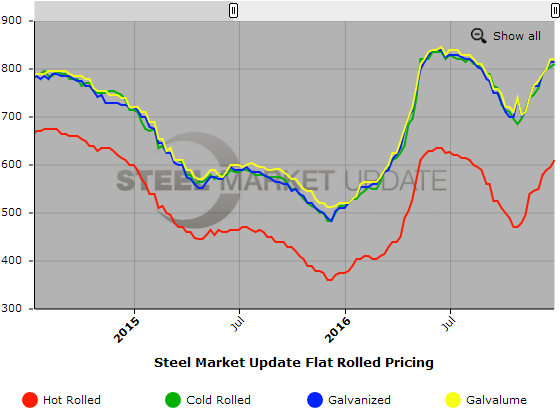

Hot Rolled Coil: SMU Range is $600-$620 per ton ($30.00/cwt-$31.00/cwt) with an average of $610 per ton ($30.50/cwt) FOB mill, east of the Rockies. The lower end of our range increased $20 per ton compared to one week ago while the upper end increased $10 per ton. Our overall average is up $15 per ton compared to last week. Our price momentum on hot rolled steel continues to be pointing toward Higher which means that prices are expected to move up over the next 30-60 days.

Hot Rolled Lead Times: 3-6 weeks

Cold Rolled Coil: SMU Range is $790-$830 per ton ($39.50/cwt-$41.50/cwt) with an average of $810 per ton ($40.50/cwt) FOB mill, east of the Rockies. The lower end of our range increased $10 per ton over last week while the upper end was unchanged. Our overall average is up $5 per ton over one week ago. Our price momentum on cold rolled steel continues to point toward Higher which means that prices are expected to move up over the next 30-60 days.

Cold Rolled Lead Times: 5-9 weeks

Galvanized Coil: SMU Base Price Range is $39.50/cwt-$42.00/cwt ($790-$840 per ton) with an average of $40.75/cwt ($815 per ton) FOB mill, east of the Rockies. Both the lower and upper ends of our range remained the same compared to one week ago. Our overall average is unchanged over last week. Our price momentum on galvanized steel continues to point Higher which means that prices are expected to move up over the next 30-60 days.

Galvanized .060” G90 Benchmark: SMU Range is $859-$909 per net ton with an average of $884 per ton FOB mill, east of the Rockies.

Galvanized Lead Times: 6-12 weeks

Galvalume Coil: SMU Base Price Range is $40.00/cwt-$42.00/cwt ($800-$840 per ton) with an average of $41.00/cwt ($820 per ton) FOB mill, east of the Rockies. Both the lower and upper ends of our range remained the same compared to last week. Our overall average is unchanged over one week ago. Our price momentum on Galvalume steel continues to point Higher which means that prices are expected to move up over the next 30-60 days.

Galvalume .0142” AZ50, Grade 80 Benchmark: SMU Range is $1091-$1131 per net ton with an average of $1111 per ton FOB mill, east of the Rockies.

Galvalume Lead Times: 7-12 weeks

SMU Note: Below is a graphic showing our hot rolled, cold rolled, galvanized, and Galvalume price history. To use the graphs interactive capabilities, you must view it on our website here. If you need help navigating the website or need to know your login information, contact us at info@SteelMarketUpdate.com or by calling 800-432-3475.