Prices

February 18, 2017

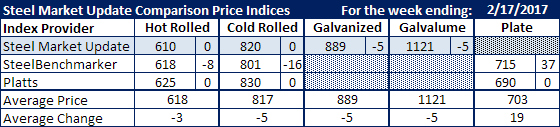

Comparison Price Indices: Not Much Happened Last Week

Written by John Packard

Flat rolled steel spot prices have recently given back some of the gains made since the first price announcements were announced by U.S. steel mills in late October. In the past 13 weeks flat rolled prices increased by $160 per ton or more depending on product and the starting point for any specific steel buyer. Over the past few weeks we have seen some erosion in spot prices. Last week we found stability in most of the indexes followed by Steel Market Update (note: SteelBenchmarker reports prices twice per month).

Benchmark hot rolled coil now averages $ 618 per ton with SMU taking the position of HRC prices averaging $610, SteelBenchmarket $618 and Platts $625 per ton ($30.50/cwt, $30.90/cwt and $31.25/cwt).

Cold rolled prices had an even wider variance with SteelBenchmarker at $801 per ton, SMU $820 per ton and Platts $830 per ton ($40.05/cwt, $41.00/cwt and $41.50/cwt).

Coated steels (galvanized and Galvalume) were down $5 per ton. Galvanized uses .060″ G90 while Galvalume is .0142″ AZ50, Grade 80.

Discrete plate prices averaged $703 per ton as SteelBenchmarker came in at $715 per ton while Platts remained at the $690 per ton they reported the week prior.

SMU Note: Galvanized prices include $69 in extras for a .060″ G90 product. Galvalume prices include $291 in extras for a .0142” AZ50 Grade 80 product.

FOB points for each index:

SMU: Domestic Mill, East of the Rockies.

SteelBenchmarker: Domestic Mill, East of the Mississippi.

Platts: Northern Indiana Domestic Mill except plate which is FOB Southeastern USA mill.