Prices

February 26, 2017

Comparison Price Indices: Adjusting to a New Move Higher?

Written by John Packard

A number of steel mills increased flat rolled steel prices, or provided price guidance higher than what was being collected in the spot markets, this past week. Steel buyers are telling SMU that there is a good chance the erosion of steel prices will cease because of these moves by the domestic steel mills. Steel prices have not yet jumped in one direction or another as the market absorbs what was announced and balances those words against the quotes actually coming out of the steel mills.

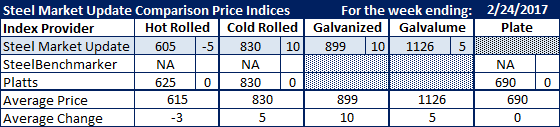

Flat rolled steel prices were mixed based on Platts and our own hot rolled, cold rolled, galvanized and plate indices (SteelBenchmarker did not report this past week as they only report prices twice per month).

Hot rolled prices dropped $5 per ton on the SMU index while Platts saw hot rolled coil as stable at $625 per ton. We noted in our writings this past week that our expectation is for hot rolled prices to bottom at $605 per ton and move higher from here.

Both Platts and SMU agree on the cold rolled average being $830 per ton which is unchanged from the week prior to last week.

Galvanized .060” G90 was up $10 per ton while Galvalume increased by $5 per ton on the benchmark item we follow which is .0142” AZ50, Grade 80.

Platts plate prices remained the same as the prior week at $690 per ton average.

SMU Note: Galvanized prices include $69 in extras for a .060″ G90 product. Galvalume prices include $291 in extras for a .0142” AZ50 Grade 80 product.

FOB points for each index:

SMU: Domestic Mill, East of the Rockies.

SteelBenchmarker: Domestic Mill, East of the Mississippi.

Platts: Northern Indiana Domestic Mill.

Note that SteelBenchmarker produces numbers twice per month. On the weeks they produce numbers we will include them in the average. The weeks where they do not produce numbers (NA = not available) we will not include their outdated numbers in the CPI average.