Market Data

March 23, 2017

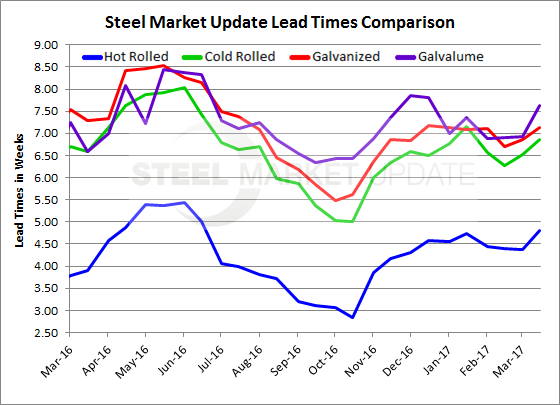

Steel Mill Lead Times Moving Out

Written by John Packard

Flat rolled lead times, which had been stuck in a rut over the past couple of months, have started to move out according to those responding to our flat rolled market trends survey. We are now seeing average lead times on hot rolled close to five weeks (4.81 weeks). We also saw movement in cold rolled, galvanized and Galvalume lead times.

Lead time is the amount of time, referenced in weeks, that it takes a new order to be produced by the domestic steel mills.

In the case of hot rolled, lead times had been averaging less than 4.5 weeks but that changed this week as our survey respondents reported the average as being closer to 5 weeks (4.81 weeks). This is almost one week longer than what we saw in the middle of March 2016.

Cold rolled lead times are also moving out (extending) and are closing in on 7 weeks (6.85 weeks). One year ago CR lead times were reported to be averaging 6.60 weeks.

Galvanized lead times move out and are now being reported as averaging slightly more than 7 weeks (7.13 weeks). This is in-line with the 7.29 weeks reported for GI last year at this time.

Galvalume lead times moved out the furthest from 6.93 weeks at the beginning of March to 7.62 weeks this week. One year ago AZ lead times averaged 6.60 weeks.

We remind our readers that the lead times referenced in this article have nothing to do with the lead times being quoted by individual steel mills. Our lead times are based on an average of the responses to our flat rolled steel market trends survey. We recommend that buyers speak with their suppliers to get the exact lead times for your products.

A side note: The data for both lead times and negotiations comes from only service center and manufacturer respondents. We do not include commentary from the steel mills, trading companies, or toll processors in this particular group of questions.

To see an interactive history of our Steel Mill Negotiations data, visit our website here.