Market Data

March 23, 2017

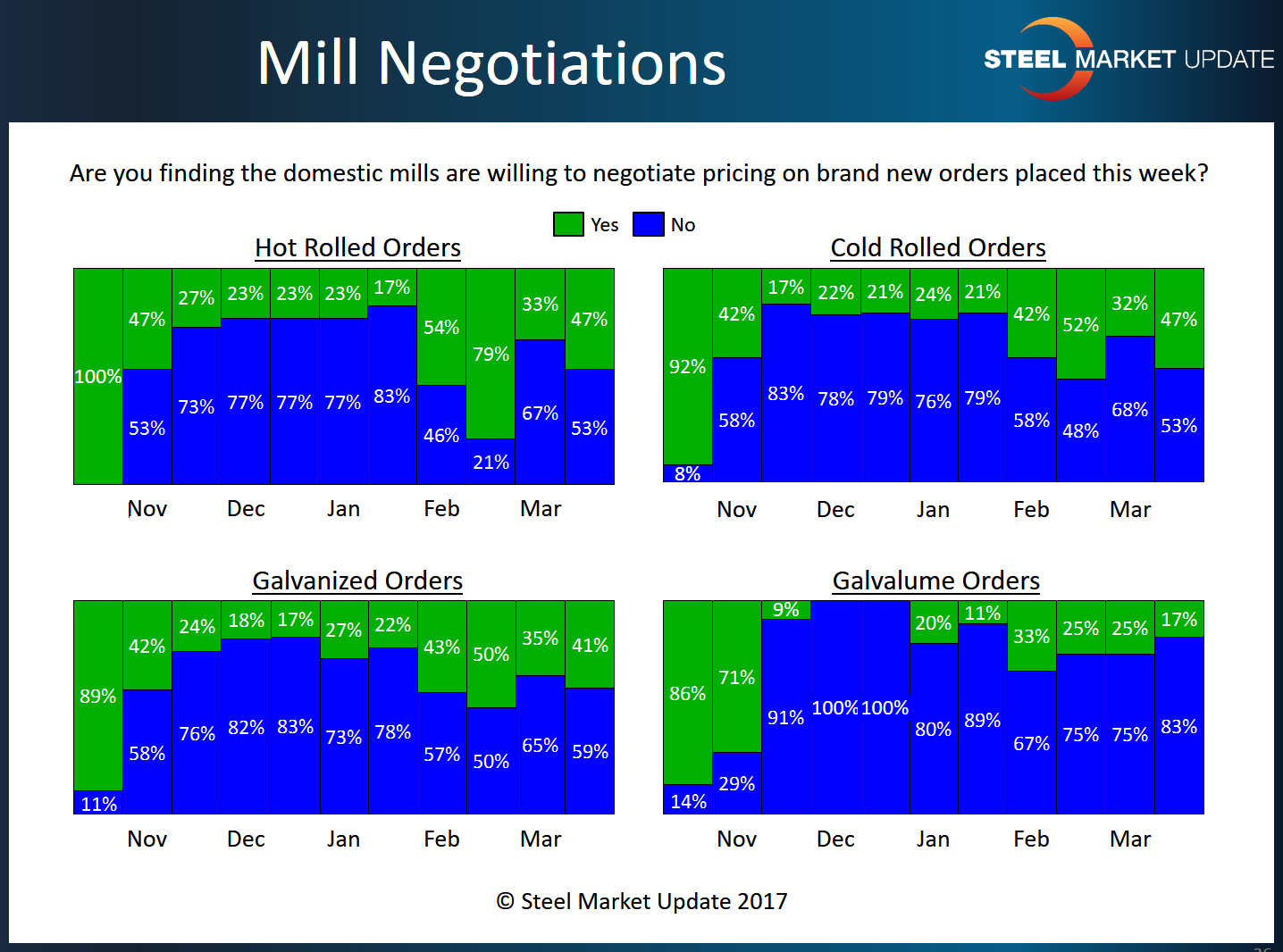

Steel Mills Somewhat Willing to Negotiate HR, CR, GI Pricing

Written by John Packard

The aggressiveness of the flat rolled steel mills was minimal on Galvalume steels this week but other products appear to be open for discussion, according to those taking the SMU flat rolled market trends analysis survey just completed earlier today (Thursday, March 23, 2017).

We found 47 percent of our respondents reporting the domestic mills as willing to negotiate HRC pricing. This is up from the 33 percent level we reported at the beginning of March. At the same time, it is a long way away from the 79 percent we saw one month ago.

Cold rolled results were similar with 47 percent of the respondents reporting the mills as willing to negotiate CRC prices. This is up from 32 percent recorded at the beginning of March and is just slightly below the 52 percent from mid-February 2017.

Galvanized results were similar to that of cold rolled with 41 percent of our respondents reporting GI suppliers as willing to negotiate pricing. This is up 6 percent from the beginning of the month and not that far from the 50 percent reported during the middle of February.

Finally, Galvalume is apparently the least negotiable flat rolled item right now as only 17 percent of our respondents were willing to negotiate AZ pricing.

A side note: The data for both lead times and negotiations comes from only service center and manufacturer respondents. We do not include commentary from the steel mills, trading companies, or toll processors in this particular group of questions.

To see an interactive history of our Steel Mill Negotiations data, visit our website here.