Market Data

June 8, 2017

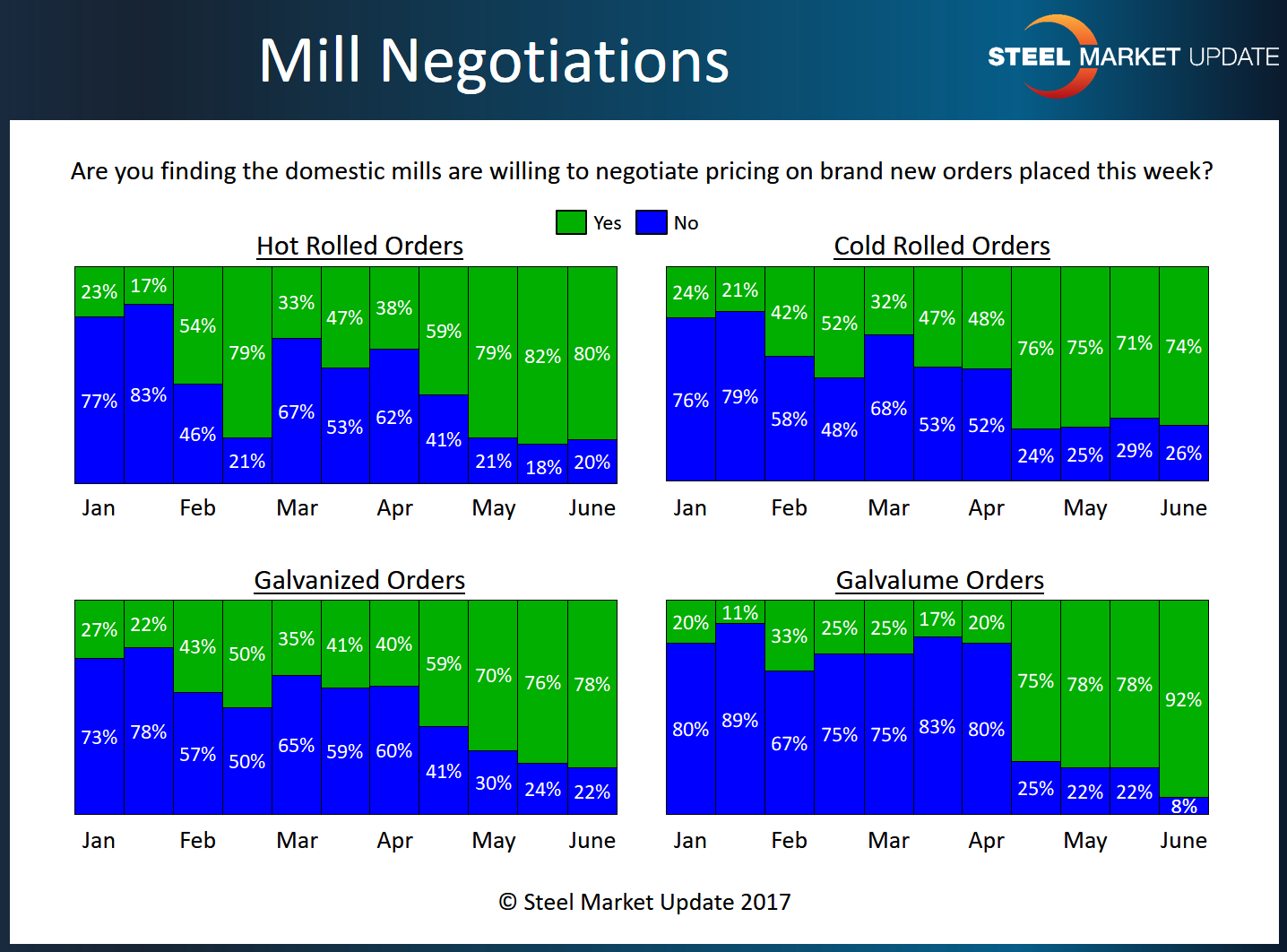

Mills Show Flexibility on Spot Price Negotiations

Written by Tim Triplett

Lead times are declining, which reflects a possible softening of demand, thus domestic mills appear to be more willing to negotiate spot pricing on hot rolled, cold rolled, hot-dipped galvanized and Galvalume steels than they were earlier in the year. About 70-80 percent of steel buyers responding to this week’s flat rolled steel market trends questionnaire report that mills have shown greater flexibility on pricing since around May 1.

SMU Note: The majority of our responses were provided prior to all of the domestic mills making their price announcements. We will watch lead times and price negotiations carefully in the coming days and weeks.

Steel Market Update sends a questionnaire to active flat rolled and plate steel buyers twice each month. Their responses provide an interesting look at changing spot pricing trends. We provide our members with various ways to analyze current and historical data using the graph below.

The graphic below is not associated with the steel mill lead times published by Nucor, ArcelorMittal, etc. The data comes from our market trends analysis and is an average by product. Each mill has their own lead times and we will do a separate analysis on those reports in Sunday evening’s issue of Steel Market Update.

SMU note: The data for both lead times and negotiations comes from only service center and manufacturer respondents. We do not include commentary from the steel mills, trading companies, or toll processors in this particular group of questions.

To see an interactive history of our Steel Mill Negotiations data, visit our website here.