Prices

July 2, 2017

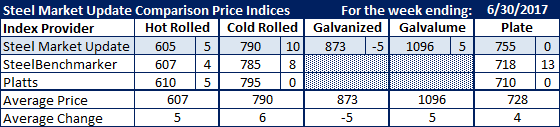

Comparison Price Indices: Small Movements

Written by John Packard

Flat rolled steel prices inched higher this past week on the indexes followed by Steel Market Update (SMU). We saw just about everyone take benchmark hot rolled prices higher by $5 per ton. SMU took our HRC average from $600 to $605, Platts took theirs from $605 to $610 and SteelBenchmarker took theirs from $603 to $607 per ton. The $5 per ton spread from top to bottom is quite tight for these three indexes.

Cold rolled prices moved on two of the indexes (SMU and SteelBenchmarker) and remained the same on one (Platts). The spread between indexes narrowed with the range being $785 to $795 per ton.

Steel Market Update showed their galvanized price average as being lower by $5 per ton with .060″ G90 averaging $873 per ton ($43.65/cwt including the G90 extra for .060″).

Galvalume was up $5 with .0142″ AZ50, Grade 80 averaging $1,096 per ton ($54.80/cwt includes extras).

Plate prices were stable at SMU, up $13 per ton on SteelBenchmarker and stable at Platts. Please note: SMU prices are freight prepaid and delivered to the customer, while the Platts and SteelBenchmarker numbers are FOB the mill and do not include freight.

SMU Note: Galvanized prices include $78 in extras for a .060″ G90 product. Galvalume prices include $291 in extras for a .0142” AZ50 Grade 80 product.

FOB points for each index:

SMU: Domestic Mill, East of the Rockies.

SteelBenchmarker: Domestic Mill, East of the Mississippi.

Platts: Northern Indiana Domestic Mill.

Plate price FOB points are different for each of the indexes:

SMU: FOB Delivered to the Customer (includes freight)

Platts: FOB Southeaster Mill (does not include freight)

Note that SteelBenchmarker produces numbers twice per month. On the weeks they produce numbers, we will include them in the average. The weeks where they do not produce numbers (NA = not available) we will not include their outdated numbers in the CPI average.