Market Data

August 17, 2017

SMU Survey Results: Lead Times Flat

Written by John Packard

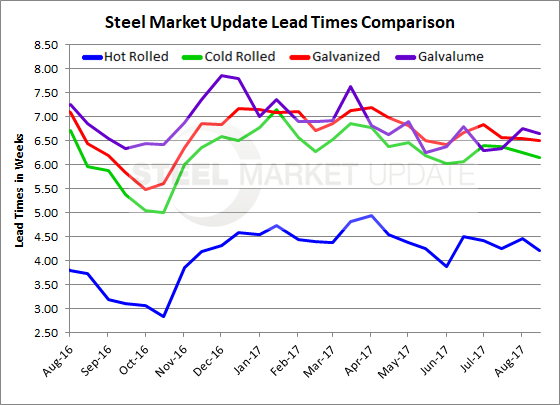

Flat rolled lead times, the amount of time it takes for the steel mills to produce an order if placed today, have flattened out and are essentially unchanged over the past few months, according to data collected by Steel Market Update from manufacturers and steel service centers earlier this week.

On Monday, Steel Market Update (SMU) sent out invitations to more than 650 steel executives to participate in our mid-August flat rolled steel market trends analysis. We asked the manufacturing companies and steel service centers participating to respond to what they were seeing for lead times on hot rolled, cold rolled, galvanized and Galvalume steels.

We understand lead times at individual mills can vary greatly based on order flows, production and maintenance issues, etc. Our goal here is to look at the trend we get by averaging the responses provided to us during the inquiry process.

Hot rolled lead times have been averaging slightly more than four weeks for many months. This week, the SMU HRC average lead time was 4.20 weeks. In mid-May it was 4.26 weeks. One year ago, HRC lead times averaged just under 4.0 weeks at 3.73 weeks.

Cold rolled lead times are acting much the same as in hot rolled. CRC lead times are now averaging right around six months (6.15 weeks), almost the same as mid-May when we reported 6.19 weeks. One year ago, CRC lead times were at six weeks (5.97 weeks).

Galvanized lead times have been hanging around six and a half weeks (6.5) for a number of months. Last year, we reported GI lead times at 6.45 weeks.

Galvalume lead times are slightly higher than what was being measured in the middle of May. Our mid-August average is 6.64 weeks. One year ago, AZ lead times were averaging 6.85 weeks.

Note: These lead times are based on the average from manufacturers and steel service centers who participated in this week’s SMU market trends analysis. Our lead times do not predict what any individual may get from any specific mill supplier. Look to your mill rep for actual lead times. Our lead times are meant only to identify trends and changes in the marketplace. To see an interactive history of our Steel Mill Lead Times data, visit our website here.

Written by: John Packard, Publisher, Steel Market Update