Prices

February 18, 2018

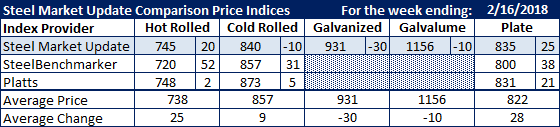

Comparison Price Indices: Wild Week

Written by John Packard

Flat rolled steel prices had a mixed week as benchmark hot rolled came close to $750 per ton for the first time since Jan. 17, 2012. We are seeing a shrinking of the spread between spot base prices for hot rolled and those of cold rolled and coated steels.

Hot rolled prices rose on all three indexes followed by Steel Market Update. However, the rate of change was significantly different from index to index. SMU has our HRC average at $745 per ton, which is up $20 per ton compared to the week ending Feb. 9. Platts came in at $748 per ton (up $2 week-over-week) and SteelBenchmarker took their HRC average up $52 per ton, but their $720 per ton is still well below Platts and SMU indices.

Cold rolled is all over the board with SMU being the lowest at $840 per ton ($42.00/cwt) followed by SteelBenchmarker at $857 per ton and Platts at $873 per ton.

Galvanized .060” G90 was also seen as being lower this past week than what SMU reported the week prior. Our average was down $30 per ton to $931 per ton. Galvalume .0142” AZ50, Grade 80 was also lower and is now averaging $1,156 per ton.

Plate prices were seen as higher across the indices. SMU has plate at $835 per ton delivered, Platts at $831 per ton delivered and SteelBenchmarker at $800 per ton FOB the mill.

SMU Note: Galvanized prices include $86 in extras for a .060″ G90 product. Galvalume prices include $291 in extras for a .0142” AZ50 Grade 80 product.

FOB points for each index:

SMU: Domestic Mill, East of the Rockies.

SteelBenchmarker: Domestic Mill, East of the Mississippi.

Platts: Northern Indiana Domestic Mill.

Plate price FOB points are different for each of the indexes:

SMU: FOB Delivered to the Customer (includes freight)

Platts: FOB Midwest Mill (includes freight)

Note that SteelBenchmarker produces numbers twice per month. On the weeks they produce numbers we will include them in the average. The weeks where they do not produce numbers (NA = not available) we will not include their outdated numbers in the CPI average.