Market Data

April 19, 2018

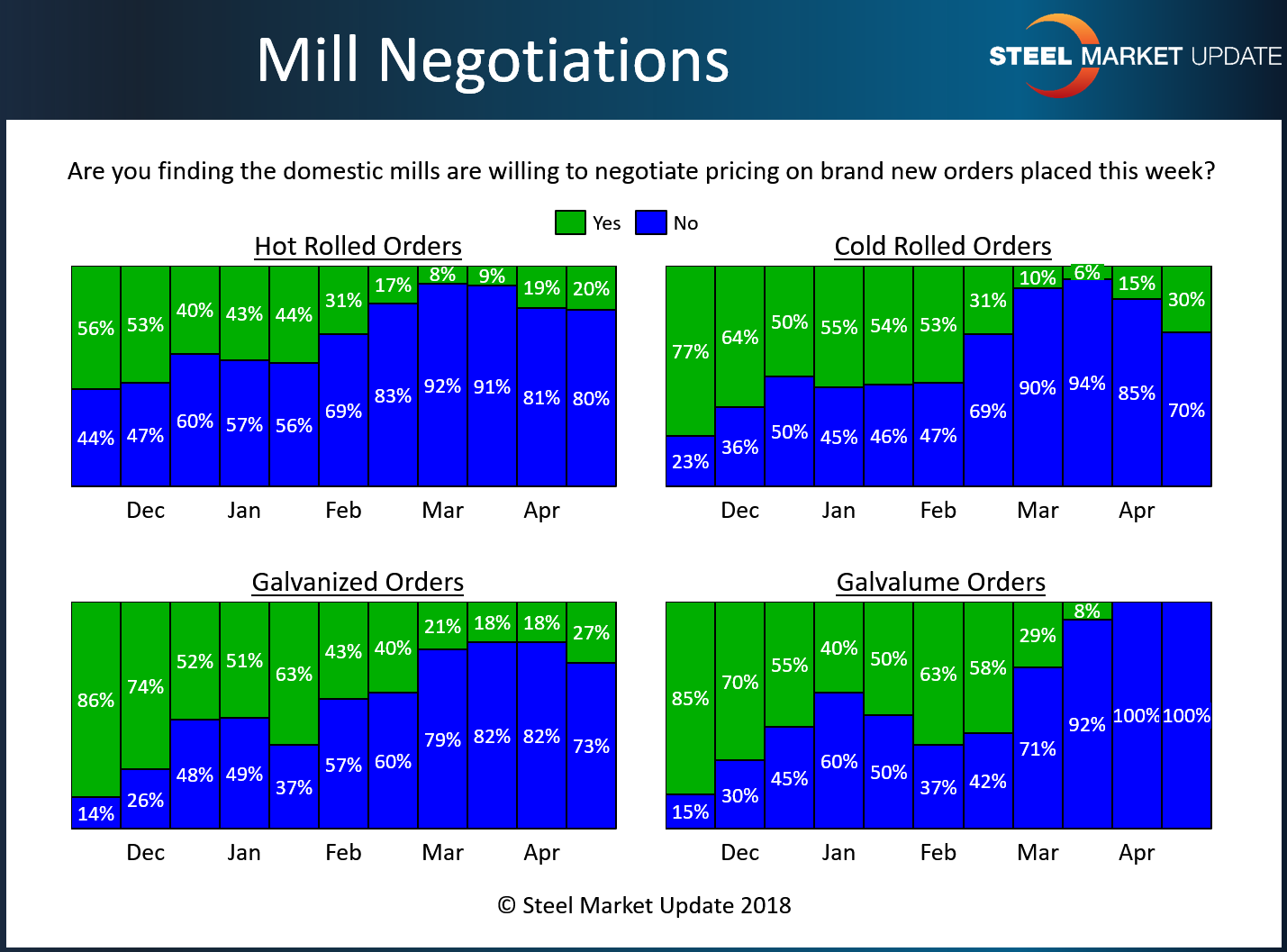

Steel Mill Negotiations: Signs of Price Talks Loosening?

Written by Tim Triplett

Are steel mills willing to negotiate spot prices on new orders in the current market conditions? For the most part mills are holding firm, but there may be some initials signs of a loosening in price negotiations, according to respondents to this week’s Steel Market Update market trends questionnaire.

Every two weeks, in a proprietary poll, SMU tracks how buyers and sellers of flat rolled steel represent the mill negotiation position. The latest data shows some mills may be slightly more willing to talk price, especially for large orders. But from a historical perspective, most steel mills continue to negotiate sparingly on hot rolled, cold rolled, galvanized and Galvalume spot pricing.

By market segment, 20 percent of hot rolled buyers said they have found mills willing to negotiate, compared with just 9 percent a month ago. But most, 80 percent, said the hot rolled mills are still standing firm.

In the cold rolled segment, 30 percent said they have found some mills willing to talk price. That’s up significantly from 15 percent two weeks ago and just 6 percent in mid-March. Still, 70 percent of respondents reported mill prices on cold rolled as non-negotiable.

In the galvanized sector, 27 percent reported that mills were sometimes willing to talk price on coated products, up from 18 percent in the prior weeks. But seventy-three percent say the galvanized mills are holding the line on pricing. Nearly all Galvalume buyers reported that mills are unwilling to compromise on Galvalume prices.

The mills still have the best negotiating position in a market where demand is strong and supply is tight. As one buyer commented: “If you consider the mills asking $45 and accepting $44, then yes, there is negotiation.”

Note: SMU surveys active steel buyers twice each month to gauge the willingness of their steel suppliers to negotiate pricing. The results reflect current steel demand and changing spot pricing trends. SMU provides our members with a number of ways to interact with current and historical data. To see an interactive history of our Steel Mill Negotiations data, visit our website here.