Market Segment

November 4, 2018

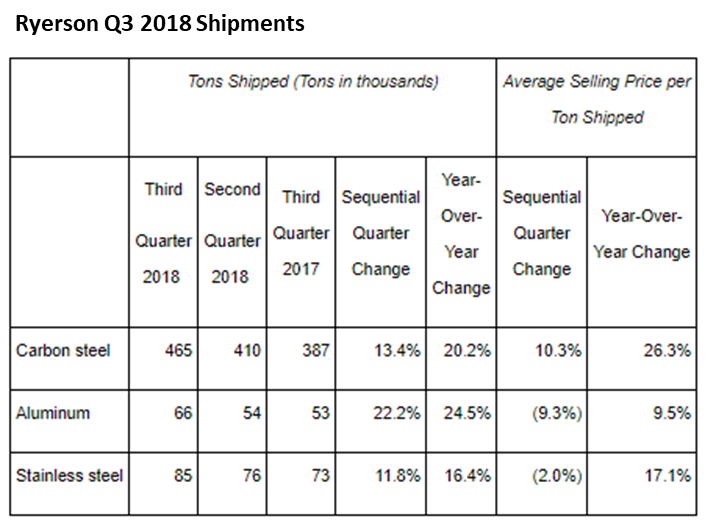

Ryerson Posts Strong Gain in Third Quarter

Written by Sandy Williams

Metals distributor Ryerson Holding Corp. reported a revenue gain of 44.6 percent year-over-year to $1.25 billion for the third quarter of 2018. Revenue was up 18.2 percent compared to the second quarter, driven by an increased average selling price and higher volume shipped.

Net income attributable to Ryerson Holding Corp. was $77.5 million for the third quarter of 2018 compared to $17.5 million in the second quarter and $1.7 million a year ago. Price per diluted share was $2.05 compared to $0.05 per diluted share in Q3 2017.

The company shipped 622,000 tons in the third quarter, up 14.6 percent from Q2 and 20.8 percent from a year ago. Average selling price per ton was $2,010, an increase of 3.2 percent from the second quarter. Average cost per ton was 4.3 percent higher than Q2 at $1,675 per ton.

Ryerson acquired Central Steel & Wire on July 2, which contributed $178.2 million in revenue to third quarter results. The acquisition of the long products facility increased company market share to 5 percent.

Shipments increased in the third quarter in the metal fabrication and machine shop sectors, but were flat to declining in Ryerson’s other end markets. The decrease was attributed to one fewer shipping day in the quarter and normal third-quarter seasonality. Additionally, tornados late in July disrupted operations at Ryerson’s Marshalltown, Iowa, facility and caused shipment disruption to customers in the Midwest.

“We’re off to a very promising start so far. Looking towards the fourth quarter, we anticipate still favorable demand and pricing dynamics relative to the prior year as U.S. economic indicators remain positive in the manufacturing economy,” said CEO Eddie Lehner. “Overall, we anticipate tons shipped in the fourth quarter of 2018 to decline less than the 7 percent average decline from the third quarter to the fourth quarter experienced during the past five years as measured by the MSCI.”

Inventory supply averaged 80 days in the third quarter, but is anticipated to return to 70-75 days as operations are further optimized at Central Steel and Wire.

During the earnings call, Ryerson management said the customer outlook remains strong for the coming quarter and new year. “I think in the second half of 2019 there’s still some key variables that are going to need to reveal themselves as to how robust 2019 turns out to be, or if it backslides at all,” said Lehner. “But the feedback we have at this time of going into 2019 is that demand trends are still good and pricing, although it’s trended down somewhat, is still fairly well supported.”

Transportation has been especially strong, said Kevin Richardson, President South-East region, particularly in the Class 8 truck market. “After a strong 2017, it looks like 2018 build rates are going to finish up 20 percent plus, and the forecast going into 2019 is for increased build rates even over the 2018 rates,” said Richardson. “So, that market in particular, which has long visibility in terms of the lead times, looks encouraging.”

Ryerson is expecting commodity prices to tail off and show up in spot average selling prices in the fourth quarter.

A decline in order activity was noticed in September and into October, which Lehner attributed to both seasonal slowdown and supply chain issues in the first half of the year. “There’s been chaos to the first half of the year in terms of supply chains and where material is coming from, how people are going to import or not import, and how they were going to get on domestic book. I do think that from Q3, things have slowed down a little bit because people were over-inventoried and they’re bringing inventories down to a more appropriate level in Q4 with the holidays coming up.

“If that’s all it is, it will be short-lived and then people will start replenishing as we get into January and February and gearing up Q1 and Q2 of next year,” Lehner added. “But if it turns out to be a little bit more than that and prices come down a bit further, then that may be protracted by a month.”

Richardson noted that utilization rates have been improving. “If you look through the entire supply chain, you can see utilization rates for the mills getting above 80 percent, and it’s been a long time since it’s been above 80 percent. The continuing shift is that less import has come in and the mills have gotten busier, which is obviously the intention of what the tariffs were geared to do.”

Lehner added that if the 80 percent rate is sustained through the fourth quarter, it could bring replenishment of inventory back sooner.

Lehner and Richardson agreed the labor market is tight. “I’ll say from my perspective it’s the tightest labor market I’ve ever managed through,” said Richardson. He added that if the labor markets are tight, it is a good sign for industrial America.