Market Data

December 10, 2018

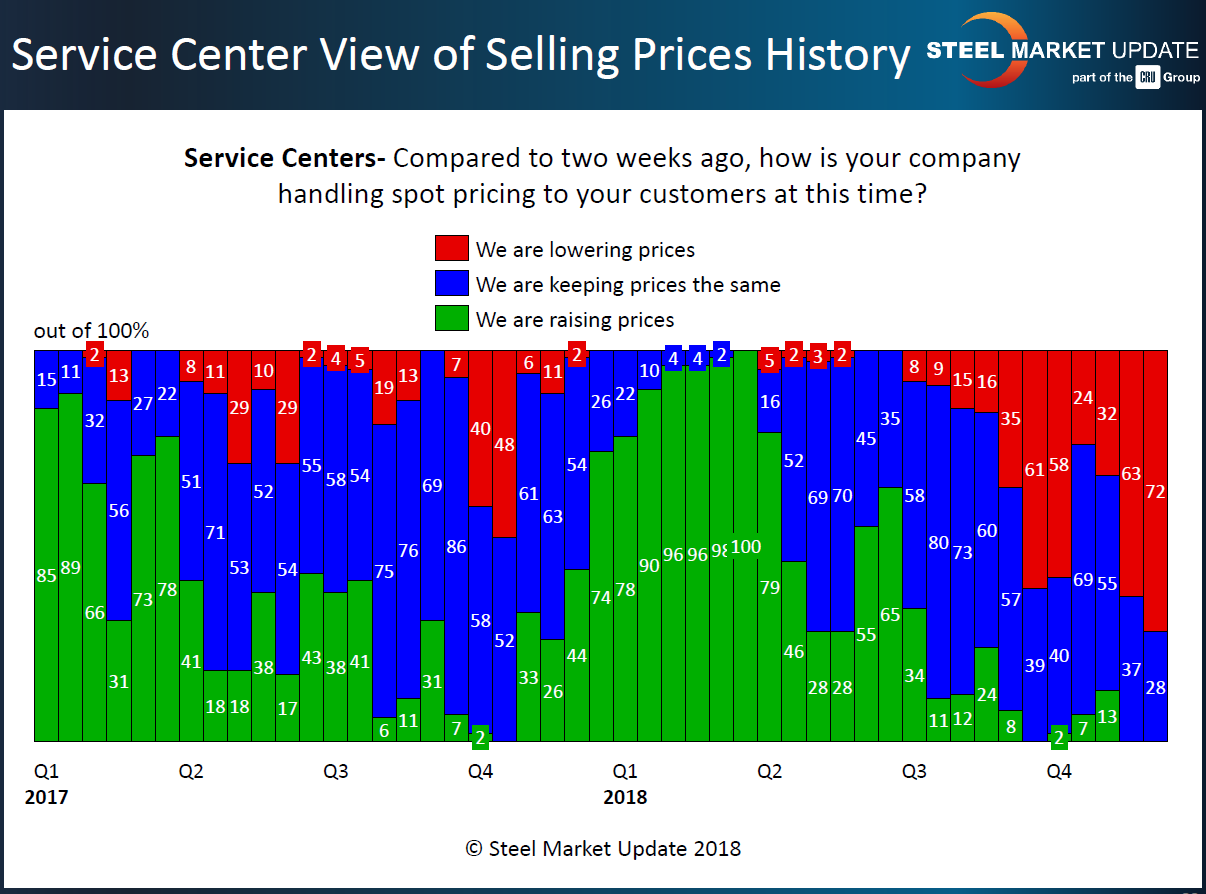

Service Centers Take Another Step Closer to “Capitulation”

Written by John Packard

Flat rolled steel service centers who responded to last week’s SMU flat rolled and plate steel market trends questionnaire are reporting in increasing numbers their service center as lowering spot prices to their customers. One month ago (early November) only 32 percent of the flat rolled distributors were reporting lower spot pricing to their customers. Now, we have seen that percentage grow to 72 percent. This is within a hair of what SMU has identified as the point of capitulation. In the past we have suggested that when 75 percent or more of the distributors advise their company as dropping steel prices, that was the inflection point or capitalization point. This is the point in time when so many service centers are dumping inventory at ever lower prices, thus devaluing inventory, that the process is putting the company at risk. It is the point of pain that can only be relieved by a change in pricing direction, which inevitably comes from the domestic steel mills raising prices.

What SMU does not know is how the markets will react when the U.S. government is so involved in setting pricing through tariffs, along with antidumping and countervailing duties.

With 93 percent of the manufacturing companies reporting their service center suppliers as lowering spot prices, in their minds the distributors are already at an inflection point. However, SMU does not rely solely on the comments of the manufacturing community alone; our capitulation indicator is based on the responses of the distributors themselves. It is the distributors who have to cry uncle (Uncle U.S. Steel, Uncle Nucor, etc.) and let the steel mills know they are willing and able to raise spot prices should the domestic mills go on the offensive.

SMU expects that as long as domestic mill spot prices, along with international prices, continue to drop, the flat rolled steel service centers will continue to follow and lower their spot pricing. Our readers should also note that capitulation may not be universal the moment our index hits 75 percent. Many times the distributors have to experience pain for some time before pushing for price increases by the domestic steel mills.