Market Data

December 19, 2018

Steel Mill Lead Times: Bouncing Along the Bottom

Written by Tim Triplett

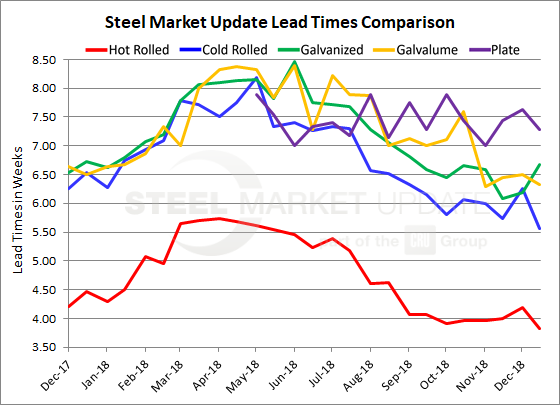

Mill lead times suggest that demand for flat rolled steel products continues to bounce along the bottom as the year comes to a close, with no clear direction yet for the first quarter.

Lead times for steel delivery are a measure of demand at the mill level—the shorter the lead time, the less busy the mill. The less busy the mill, the more likely they are to negotiate on price. Lead times for hot rolled now average less than four weeks, cold rolled less than six weeks and coated steel around six and a half weeks.

Hot rolled lead times now average 3.83 weeks, down from 4.19 weeks in early December. Current lead times for hot rolled are below the 4.47 weeks at this time last year and nearly two weeks shorter than the 2018 peak of 5.73 weeks in April. The last time HR lead times were shorter was in October 2017.

Cold rolled lead times also are unusually short. Cold rolled orders currently have a lead time of 5.57 weeks. Except for brief periods in October and November, Steel Market Update has recorded CR lead times under six weeks on only one other occasion in the past two years.

Demand for galvanized steel appears to be the strongest of the flat rolled products, with a current lead time of 6.67 weeks, the most extended it has been in the past three months. It remains well below this year’s peak of nearly eight and a half weeks in June, however.

Lead times for Galvalume now average 6.33 weeks, little changed since reaching the low point of the year in early November.

Note: These lead times are based on the average from manufacturers and steel service centers who participated in this week’s SMU market trends analysis. Our lead times do not predict what any individual may get from any specific mill supplier. Look to your mill rep for actual lead times. Our lead times are meant only to identify trends and changes in the marketplace. To see an interactive history of our Steel Mill Lead Times data, visit our website here.