Prices

July 9, 2019

Mill Capacity Utilization Remains Below 80 Percent

Written by Tim Triplett

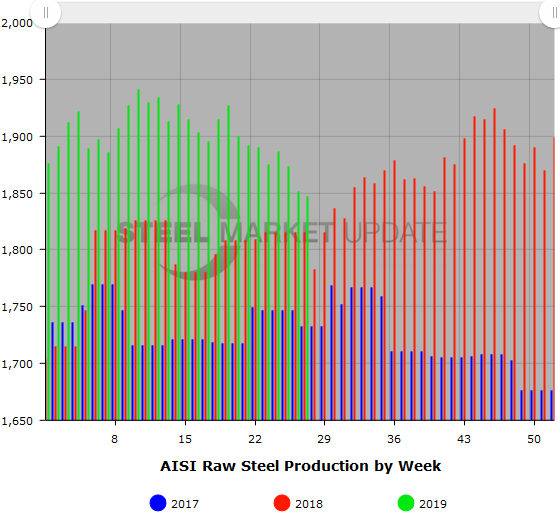

The U.S. mill capability utilization rate saw a slight dip again last week to 79.4 percent–below the 80 percent level steelmakers had hoped to maintain. Raw steel production for the week ending July 6 totaled 1,847,000 net tons, the lowest level seen since last fall. Production was down 0.2 percent from the previous week, but was still 1.8 percent higher than the same week last year, reported the American Iron and Steel Institute.

Adjusted year-to-date production through July 6 totaled 50,458,000 net tons at an average capability utilization rate of 81.2 percent. That’s up 5.3 percent from the 47,918,000 net tons during the same period last year when the capability utilization rate was 76.7 percent.

Following is production by district for the July 6 week: North East: 207,000 net tons; Great Lakes, 688,000 net tons; Midwest, 203,000 net tons; South, 679,000 net tons; and West, 70,000 net tons, for a total of 1,847,000 tons. Production declined in the Northeast and Great Lakes regions, but saw small increases in the Midwest, South and West, compared with the prior week..

The raw steel production tonnage provided in this report is estimated. The figures are compiled from weekly production tonnage from 50 percent of the domestic producers combined with monthly production data for the remainder. Therefore, this report should be used primarily to assess production trends. The AISI monthly production report provides a more detailed summary of steel production based on data supplied by companies representing 75 percent of U.S. production capacity.

Note: Capability for third-quarter 2019 is approximately 30.6 million tons compared to 30.8 million tons for the same period last year and 30.3 million tons for second-quarter 2019.