Market Data

July 16, 2019

Service Center Spot Prices to End Customers are Making the Turn

Written by John Packard

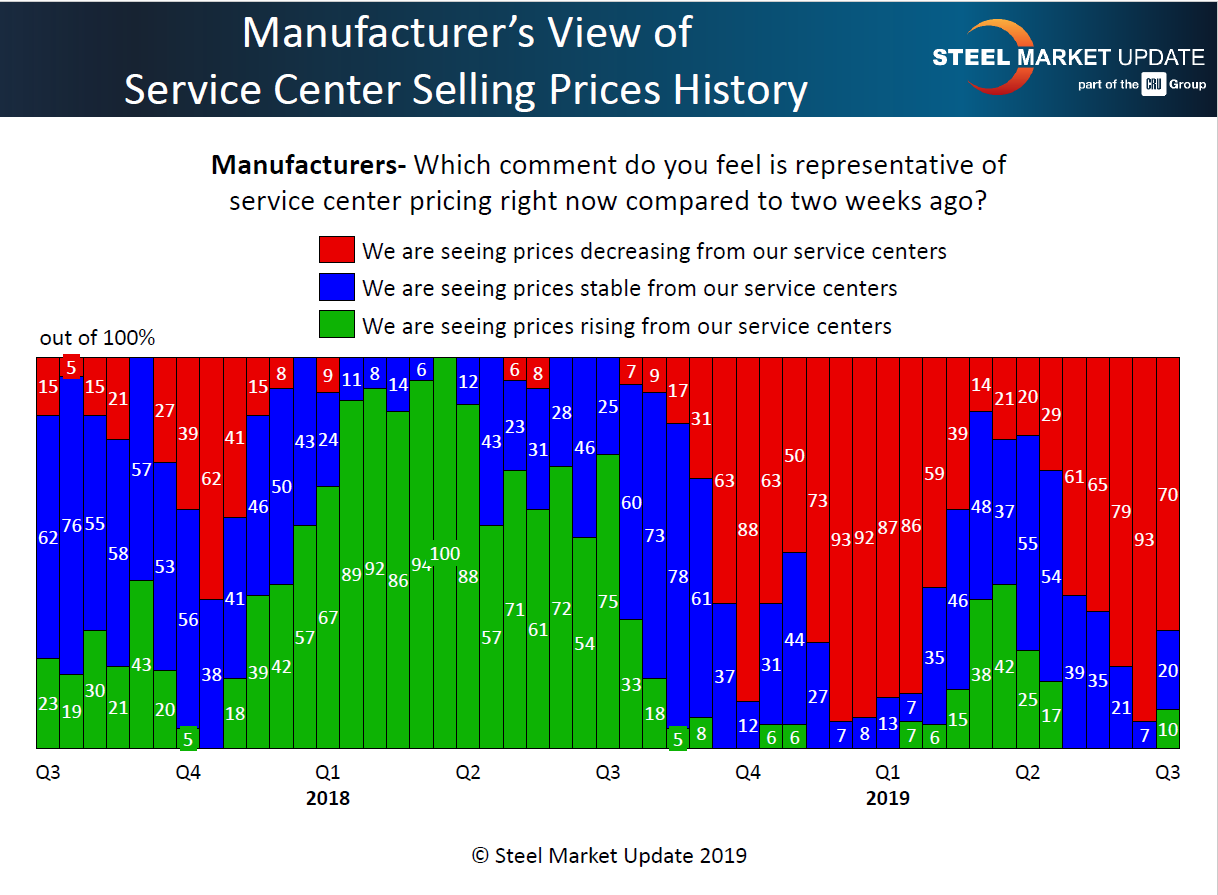

In Sunday’s issue of Steel Market Update, we adjusted our Price Momentum Indicator on flat rolled from Neutral to Higher. One of the justifications for that move was the Service Center Spot data we were collecting last week. In our analysis, we found a change in pricing mentality, not a 180 degree change, but a change nonetheless.

Manufacturing companies noted a change with 70 percent of them reporting distributor spot pricing as moving lower than what they saw two weeks earlier. This is 23 percentage points lower than what we saw in the middle of June (prior to any price announcements).

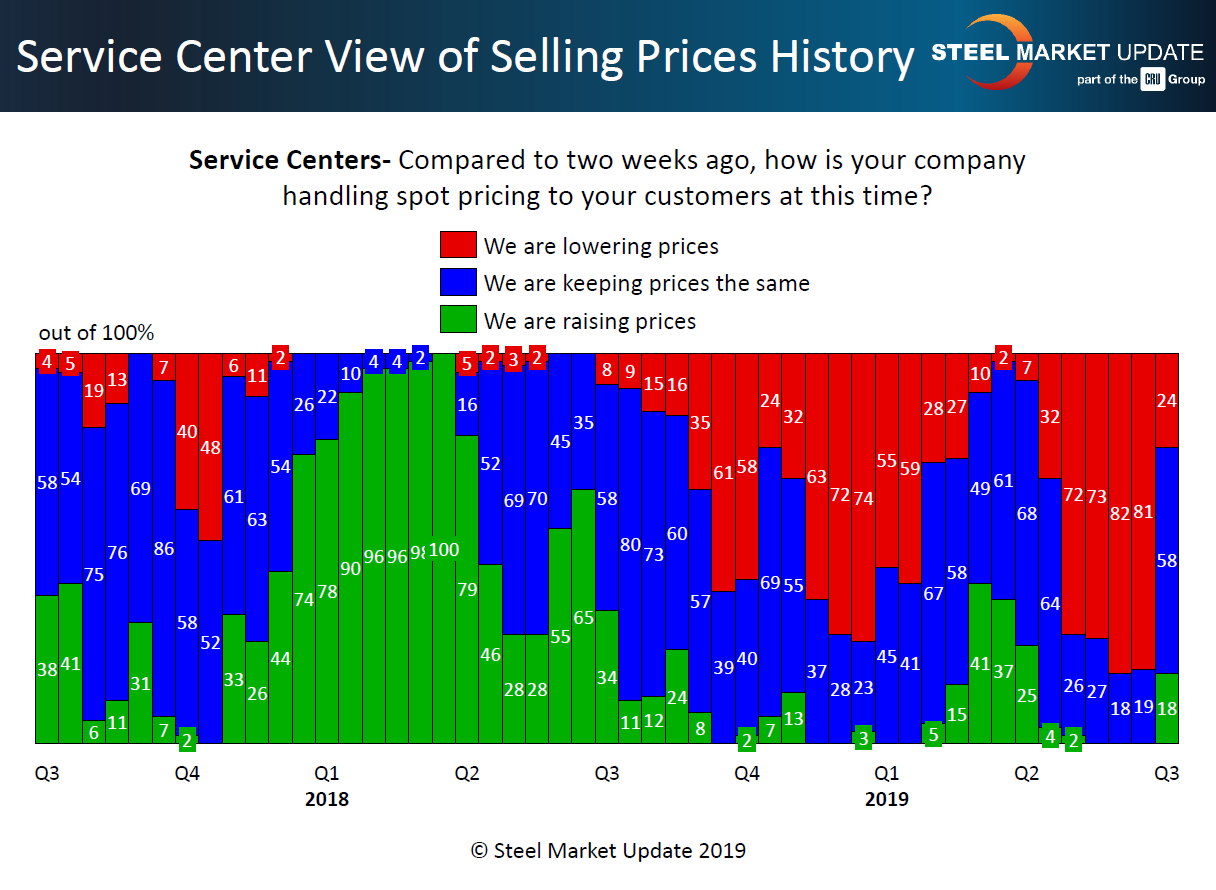

The change in direction, according to the service centers participating in last week’s survey, was even more dramatic as only 24 percent of the distributors reported their company as lowering spot pricing to their end customers. This is 57 percentage points lower than what was reported in the middle of June.

What is important from this point are the green bars on the two graphics shown above. In SMU’s opinion, in order for the price increases to not only stick but gain traction, the distributors need to begin raising spot prices to their customers. As noted in Sunday’s article, earlier this year we had a “dead cat bounce,” which you can clearly see in the green bars during the later portion of first-quarter 2019. If we see the same tepid support of the increases over the next four to six weeks, this will most likely be another “bounce” event. What the domestic mills want to see is what we had in late fourth-quarter 2017 and into first-quarter 2018. At that time prices were rocketing higher.

The higher the green bars representing price increases coming out of the steel service centers, the more chance prices out of the domestic mills will be moving in concert (not vice versa).