Analysis

May 15, 2020

Final Thoughts

Written by John Packard

The United States is beginning to go back to work. Automotive plants are scheduled to begin opening this week. The U.S. is working with Mexico to ensure automotive suppliers in Mexico are deemed “essential businesses” and return to work.

From my perch here in Florida, traffic has returned to normal, restaurants are open (50 percent of capacity) in all but a couple of counties, beaches are opening as are many stores. Exactly how big an impact there has been to the economy is unknown, but very much in debate.

That debate will continue Wednesday at 11 AM as our SMU Community Chat guest speaker will be John Anton steel, purchasing and pricing expert for IHS Markit. You can register for this free webinar by clicking here.

Being the parent of a professional musician and another in the food service business, their jobs are not returning anytime soon. I can only keep my fingers crossed that people remain smart, social distance, invest in a fun mask (and wear it when in public) and that someone in the world finds a vaccine that will work (and be safe).

Click here if you want to learn more about what each state is doing regarding remaining in lockdown or reopening.

In our latest flat rolled and plate steel market trends survey, we are seeing early signs of life, early signs of a growing optimism. Our SMU Steel Buyers Sentiment Index left the pessimistic portion of our index and is now +15 (based on a single week’s data point) for Current Sentiment. Future Sentiment never dropped below +10 (barely in the optimistic range) and has now rebounded to +30. Both are good signs that buyers and sellers of steel feel conditions are improving.

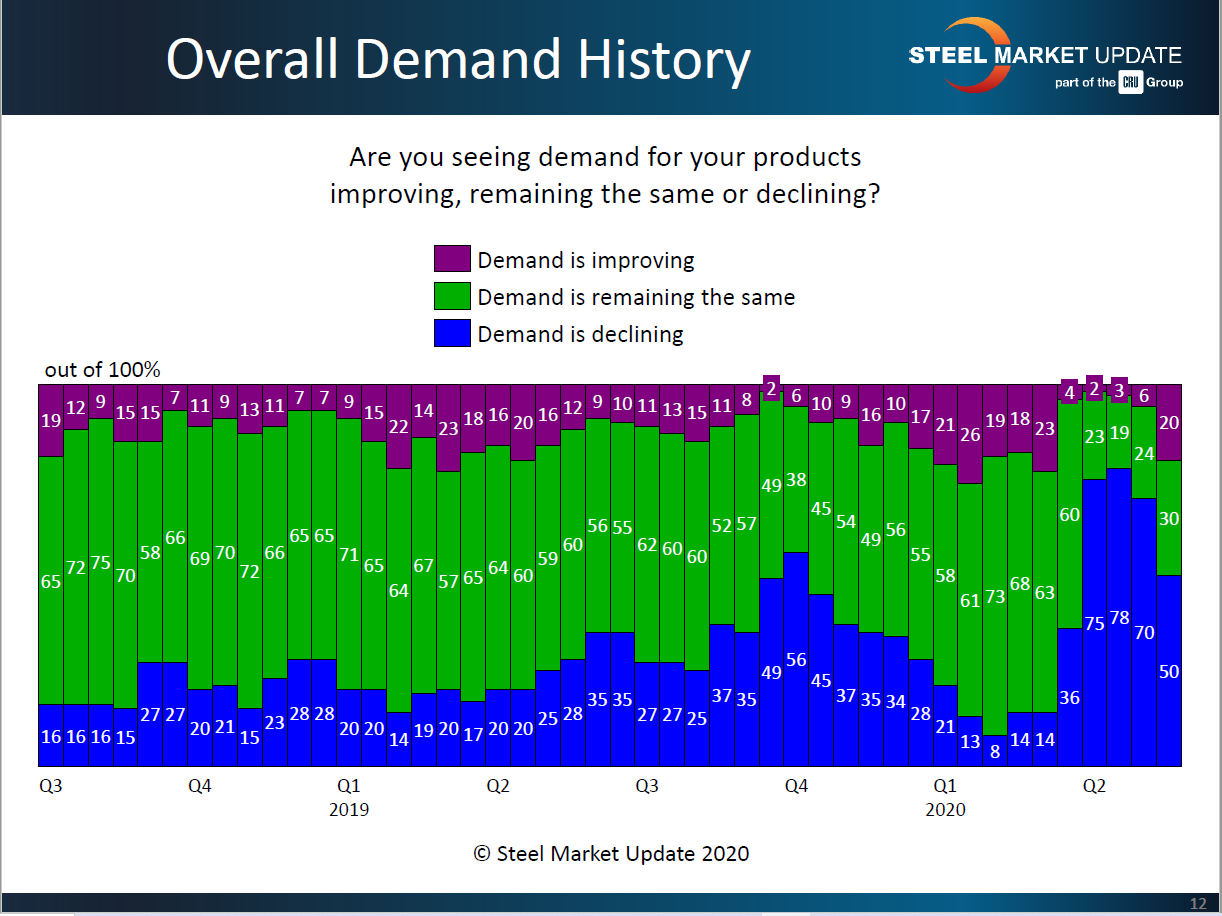

Demand is the area of concern for everyone. The data collected during our survey suggests there are hurdles to overcome ahead of us. We did see general demand improve…well, maybe a better way to say it is fewer respondents reported declining demand this past week than in the prior six weeks (see graphic below).

The vast majority of those responding to our survey last week (74 percent) believe the domestic mills will announce another price increase on flat rolled before the end of May.

One reason for another increase by the domestic mills can be seen in the responses we received regarding the amount of the first increase that is being collected now. Only 5 percent of those responding to our query reported mills as collecting the full increase. Slightly more than half of the respondents reported a portion of the increase was being collected.

Our Premium members can get the full details on these and many other questions asked last week by going to our website. On the Home Page (you must be logged in to your Premium account) click on the Analysis tab and pick “Latest Survey Results” from the drop-down screen. Executive members can view a sample survey, but are not able to see the latest and the full history of surveys that are on the site. If you would like information about how to become a Premium member, please contact Paige@SteelMarketUpdate.com

Paige Mayhair is also your contact if you would like to renew your membership, add new members (many companies are not utilizing all of the licenses they have available to them), upgrade your account or to add a new account. She can be reached at 724-720-1012.

I am in my office all week. You can reach me at John@SteelMarketUpdate.com.

As always, your business is truly appreciated by all of us here at Steel Market Update.

John Packard, President & CEO