Overseas

May 28, 2020

CRU: Steel Prices Lack Direction Without View of Demand

Written by George Pearson

By CRU Prices Analyst George Pearson, from CRU’s Steel Monitor

In the U.S. Midwest, sheet prices have continued to strengthen while plate prices have weakened further. HR coil prices increased for the third consecutive week, albeit by just $5 /s.ton to $487 /s.ton. The volume-weighted average of transactions remains below recent mill targets of $500 /s.ton, with the overall range of activity being $460-510 /s.ton. Even so, mills have again raised their price target to $540 /s.ton. Overall spot transaction volume has been low, with buyers continuing to report that business activity is down such that current inventories are allowing them to live within their contracts and only make limited spot orders.

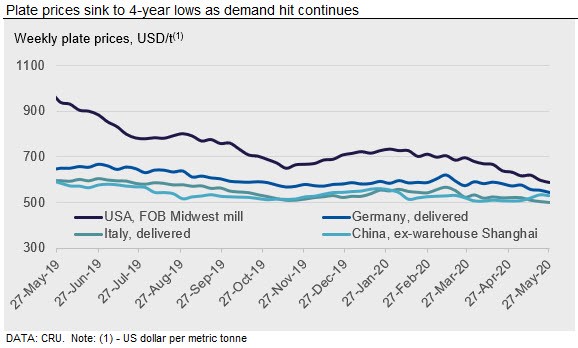

The spread between CR and HDG coil prices has decreased, as CR coil fell by $20 /s.ton while HDG coil gained $11 /s.ton. While mills had attempted to lift plate prices by $40-50 /s.ton, prices fell this week by $9 /s.ton to $533 /s.ton. Plate prices have now fallen by $132 /s.ton since their recent peak in January and they are now at their lowest level since November 2016. We believe this will be the low point for plate as higher-priced activity starts to emerge this week.

European sheet prices have fallen sharply for the second consecutive week. German prices were down by €8-23 /t, while Italian prices fell to a slightly lesser degree. This is primarily because German prices held up for longer than those in Italy, which fell faster and earlier. German HDG coil dropped most significantly, down €23 /t w/w. Auto demand is still extremely weak and sellers that normally supply HDG to the auto market are looking to shift tonnes to industrial customers instead. This is increasing HDG availability for those buyers and creating competition.

The resumption rate of European businesses has increased and construction works are taking place again. Even so, mills and service centers are still delivering orders that were placed before the lockdown and any spot orders are for small packages. There is little visibility of forward orders and what demand will look like beyond five to six weeks. There is some concern that companies are finishing parts of projects that were in progress before the lockdown, which may not continue thereafter. Mill lead times in Europe have decreased, with some at less than five weeks for HR coil. India has diverted sales to Asia in recent weeks and is no longer offering aggressively in Europe. Turkish prices have also increased slightly, reducing their competitiveness in Europe.

Chinese steel price softened this week after strong increases for several weeks; HR coil fell by RMB40 /t to RMB3550 /t and rebar by RMB50 /t to RMB3540 /t. Government stimulus measures announced following the “two sessions” meetings were below expectation, which led to less positive market sentiment. Furthermore, the government announced that it would not set a GDP growth target for 2020. Trade volumes decreased on more bearish sentiment and market participants became more cautious.

Despite still rising steel production, destocking continues in China as demand continues to rise. New and existing construction projects have accelerated their progress to compensate for two months of lost activity during the lockdown and to complete works ahead of hotter and wetter weather during the rainy season, especially in southern China. Total rebar inventory fell by 7 percent w/w and HR coil fell by 4 percent. Looking ahead, steel output growth is to slow due to high capacity utilization rates, weakened sentiment and falling prices. Even so, the still-high inventory level will continue to weigh on prices. This is compounded by uncertain future steel demand, and prices are expected to decrease in the coming weeks.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com