Overseas

September 13, 2020

CRU: Chinese Sheet Prices Up on Strong Demand

Written by CRU Americas

By CRU Analyst Kevin Bai, from CRU’s Steel Sheet Products Monitor

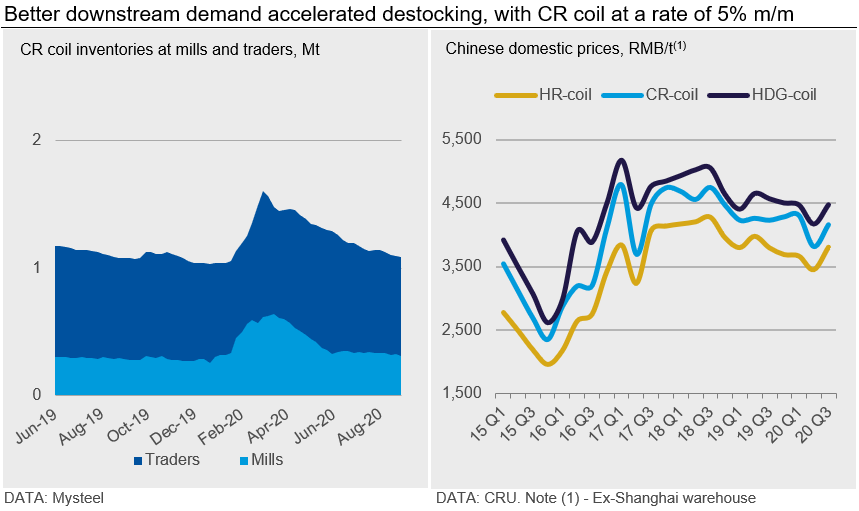

Domestic sheet prices in China continued to reach new highs for the year alongside further improvement in underlying sheet demand in combination with limited supply. Domestic CR coil prices went up by RMB290 /t to RMB4720 /t and HDG sheet by RMB140 /t to RMB4840 /t, ex-Shanghai warehouses, as CRU’s latest price assessments show.

Sheet demand in downstream sectors continued to pick up in the past month. Automobile sales continue to increase through August based on the latest data from the China Passenger Car Association. Retail vehicle sales have been strong given sales promotion as well as the government’s preferential policy on new electric vehicle purchases. Furthermore, these sales gains have kept car inventories at dealers relatively low compared with a year ago. Auto dealers remain confident that the demand recovery will continue over the near term, so there is a need to restock for dealers before the October National holidays.

The appliance sector, much like automotive, has continued to exceed expectations. Fueled by increasing export orders, white goods production increased significantly in July and people close to the industry told CRU that they are expecting another big month in August.

Lastly, in addition to these segments of durable goods manufacturing, demand for HR coil and steel strip intensive goods have also recovered. For sectors such as sheet-based structural and welded pipes, buying has resumed given rebuilding in the aftermath of flooding in the eastern and southern part of China. Indeed, pent-up demand at construction sites has supported these sheet-intensive sectors.

Sheet production at the mills has remained steady alongside HR coil margins of 10 percent as inventory destocking has continued (see chart). Meanwhile, hot metal supply has tightened slightly given production restrictions in Hebei as well as scheduled maintenance at some major mills such as Anshan and Maanshan. This supply tightness has caused CR coil prices to increase more than other products in our price basket.

Outlook: Near Term Seasonal Strength Before Late Q4 Reversal

For the near term, downstream sheet demand will continue to remain strong, supported by the seasonal pick-up traditionally seen around September-October. Meanwhile, increasing exports of steel-containing goods will continue to boost domestic sheet demand in the next month or two, as global markets rebuild their inventories of these goods following the Covid-19 restrictions. Consequently, we believe growth in demand will outpace the increase in supply so sheet prices will be supported, more so for CR coil and coated sheet.

Further out, the November and December period may be a time where prices reverse course as pent-up demand for steel-containing goods falls back as business activity settles into a post-Covid normal. This trend may emerge alongside a period of normal seasonal weakness, which may lead to a rapid decline in sheet prices. Currently, we have not included this in our base case forecast, but will assess the next move as we get more information on this matter.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com