CRU

January 15, 2021

CRU: Is Substitution a Threat to Aluminum (or Steel)?

Written by Greg Wittbecker

By Greg Wittbecker, Advisor, CRU Analysis

Whenever prices for key commodities such as aluminum, steel, wood or rubber start to really rise, there is a natural tendency for Procurement Officers to say, “let’s look at alternatives.” That’s their job, and if they weren’t looking at options to compensate for cost increases, they would be fired. However, we are living in different times and those old tapes (what’s a tape?) just don’t resonate like they used to!

No Place to Hide in This Inflationary Cycle

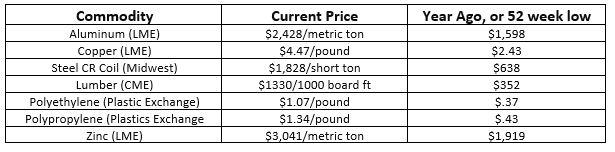

Comparisons of leading raw materials year on year or versus 52-week lows show breathtaking rises across the board. That in and of itself is reason for a Chief Procurement Officer to pause when considering “Plan B” to move away from an existing substrate of aluminum or steel.

Copper’s premium to aluminum is over 4:1 and if anything, copper is losing share to aluminum in magnet wire for light duty appliance motors, grounding cables, and medium voltage distribution as cost is trumping copper’s better conductivity.

Zinc’s premium to aluminum is working against the galvanizing market that might be tempted to poach 5000 alloy aluminum for corrosion applications.

Wood versus aluminum (or steel), forget it. Dimensional lumber for windows and doors is out of sight. In high-end construction it won’t matter, but in the entry-level and mid-price range, aluminum and steel will compete nicely against wood and vinyl.

Putting aside the price comparisons, there’s an entirely new consideration that really positions aluminum and steel very well…and that’s sustainability.

ESG Criteria for Materials Makes Aluminum and Steel Hands Down Winners

Life used to be so simple. Find the cheapest material that would meet the engineering requirements from Operations and then go beat up prospective suppliers for the lowest price. That’s all changed now.

Not only is price important, but so is whether the material is sustainably produced, and then what happens to it at end of life? The aluminum and steel industries are fierce competitors, but one thing we have in common is a great sustainability story.

Virtually any form of aluminum can be recycled. Our pre-consumer aluminum scrap is virtually 100% recovered. Aluminum from post-consumer recovery in the form of auto shredding and used beverage containers (UBC) enjoys a good rate of recovery (although we can do better on UBC than our current 50% recovery rate, but the solution is for another article).

The steel industry has a long and proud history of recycling. Surging EAF production underscores the sustainability of steel.

Some of our mutual competitors can’t rival us. Plastics is a classic example. The recycling rate for PET beverage bottles is around 25% and millennials are rejecting the package. Aluminum beverage can demand is soaring as millennials embrace aluminum as a sustainable package. The soft drink, energy drink and even water brand-owners are paying attention. No one would have believed 10 years ago that you’d see still water in an aluminum can, but you do now and that’s in direct response to the customer demand for a sustainable product.

So, when the substitution word comes up in an industry discussion, aluminum and steel are doing just fine on a price competitiveness basis. If people want to press the issue harder, ask them about the recycling track record of that substitute such as plastics or even carbon fiber. They have no comeback relative to aluminum and steel.

Greg Wittbecker joined CRU in January 2018 after retiring from Alcoa, where he was Vice President of Industry Analysis and Managing Director of Alcoa Beijing Trading, based in Shanghai, China. His career spans 35 years in the aluminum industry, having also held senior commercial and management roles at Cargill, Wise Metals and Koch Supply and Trading. Greg brings perspective on the entire aluminum supply chain from bauxite to aluminum finished products and will be a regular contributor to SMU going forward. He can be reached at gregory.wittbecker@crugroup.com

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com