Prices

September 18, 2022

CRU Aluminum: Price and Premiums Still Looking for a Floor

Written by Greg Wittbecker

Long liquidation as opposed to short selling?

I spoke this week at two diverse industry groups: the Aluminum Extruders Council (AEC) and the Institute of Scrap Recycling Industries (ISRI).

While differing in their sector concentration, the audiences had the same questions:

• What’s going on with the London Metal Exchange (LME) aluminum price?

• Why are US Midwest physical premiums still falling?

I was not trying to be glib with my responses to both groups when I said, “We have replaced the greed cycle with the fear cycle.”

Both the LME and our regional physical markets seem to be in the grip of an overwhelming sense of dread over both global and US economics. We spend all our time looking for the ugly indicators and ignoring any evidence that might indicate the sell-off in prices is ending.

The LME is fixated on European demand destruction and ignoring supply destruction

The World Bank came out on Sept. 15 and talked about a global recession in 2023 on the back of central banks raising key lending rates. This comes on the heels of the IMF World Economic Outlook in July shaving GDP estimates across the board, with Germany looking especially bearish.

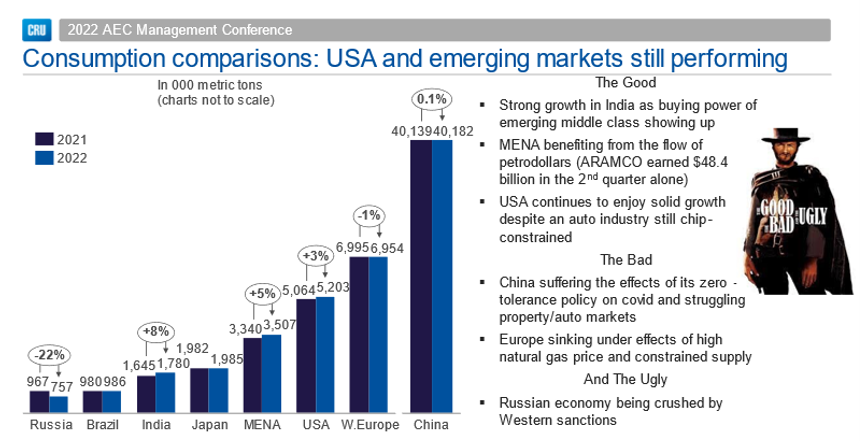

CRU DOES think that things in Europe look difficult, and we have western European aluminum demand shrinking by 1% in 2022 before starting to recover in 2023. And it still won’t be back to 2021 consumption levels.

But we also see the US doing well and emerging markets even better. The slide below from my AEC remarks graphically shows the wide disparity in growth rates around the world.

I want to dwell on Europe for a bit because I think it is important to examine the demand situation in the context of European smelter closures.

A 1% decline in western European primary aluminum demand = 70,000 metric tons per year. By contrast, we see more than one million tons of smelter closures in Europe. You don’t have to be a math genius to see we are changing our supply versus demand balance more abruptly on the supply side. Smelter closures translate to more than 14% of our demand. When I see the LME ignoring this, it makes me wonder if people seriously believe Europe will fall 14%? I know the gas situation is dire, and lots of industrial production could be at risk. But I also think Europe, and especially Germany, will be highly resourceful in keeping its industrial output going.

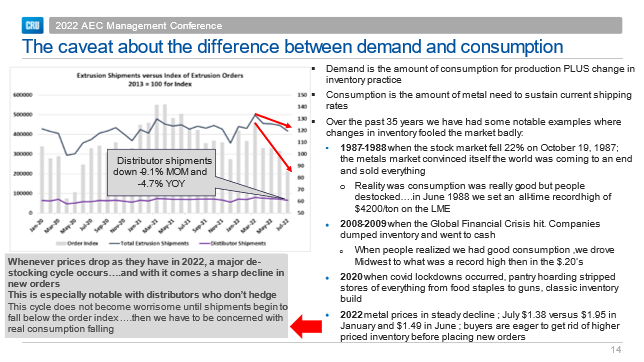

We are the midst of a massive destocking cycle thanks to the price collapse

People spend a lot of time studying orders as a clue to demand. That’s a good idea, but not if they make orders the sole indicator of real consumption. As the slide below details, demand is a function of real consumption plus inventory behavior. There is no question that the aluminum-price rout since January 2022 has been painful for anyone holding unsold inventories. Distributors are the best example of inventory “longs” who can’t or won’t hedge their holdings It’s great when prices are rising and painful when they are falling. Now is very painful, and they react to that by not replacing their shipments with new orders. I suspect all of you in the steel service center sector can relate to this too.

On the one hand, we are seeing aluminum orders down month on month and year on year. On the other hand, shipments are still higher year on year. That tells me we are in the middle of a classic destocking cycle.

Physical traders still in the midst of long liquidation versus short selling

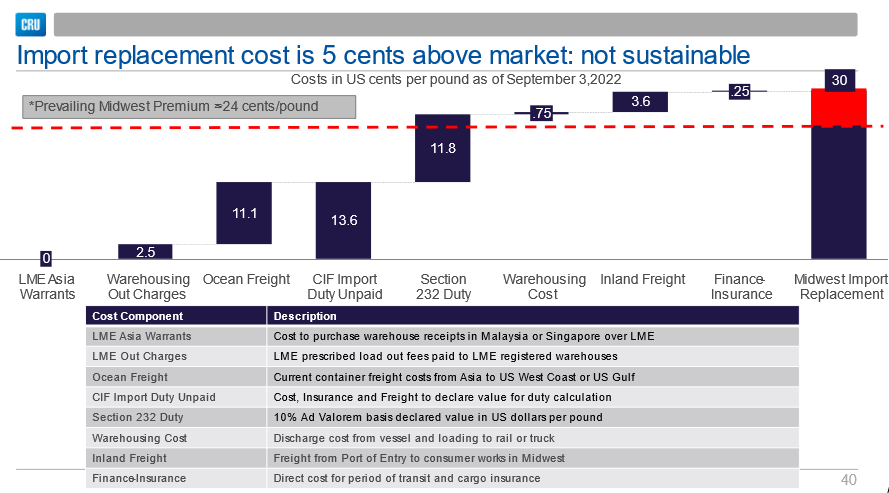

Midwest premiums are approaching 24 cents/pound premium to LME. That continues to widen the gap between seaborne, import replacement, and “the market.” The slide below gives you the detail behind this replacement cost.

Traders that I have spoken to in the last week agree with the math, and few see a good risk/reward to continuing to push premiums lower. But some accept the fact that the “weak longs” want out. And until they are finished selling, the market will not find a floor.

However, the caveat here is that once the destocking cycle ends, consumers will need to replace what they are continuing to ship out the back door. That could portend a nice snap back in Midwest premiums and might prompt the LME bears to sit up and pay attention to the supply destruction coming at us much faster than demand destruction.

By Greg Wittbecker, Advisor, CRU Group, Gregory.Wittbecker@CruGroup.Com