CRU

September 27, 2024

CRU: North American zinc supply at increased risk of disruption

Written by Helen O’Cleary

Refined output will decline y/y in H2

North America’s refined zinc output was flat y/y in H1 2024, but we estimate it will decline 3.0% y/y in H2. This is due mainly to a sizeable disruption allowance to cover the planned maintenance closure at Glencore’s Valleyfield smelter (305,000 mt/y) in Quebec. Assuming the cell house replacement and post-maintenance ramp-up go according to plan, we expect North American refined zinc output to fall 1.5% y/y in 2024.

We understand that contingency planning means output losses will be covered, and no impact on the market balance as a result of the closure is envisaged. However, given the complexities of ramping up a smelting operation after a maintenance closure, there are potential downside risks to supply. With no news yet on the reopening of Nyrstar’s Middle Tennessee mines in the US, which were put on care and maintenance in November 2023, there is also the potential for lower output from the Clarksville, Tenn., smelter (125,000 mt/y).

North American steel mill demand has waned

The first US interest rate cut in four years came earlier this month, with the Fed announcing a 50-bps cut. However, no immediate relief is expected for US steel mills, which continue to struggle with weak end-use demand. Although automotive demand is stable, orders from some other sectors have weakened further. The pressure from low-priced imports of coated sheet prompted four US steel mills to launch a petition for import duties on coated sheet from 10 countries. The petition covers around 77% of total US imports of these products in 2023, so it could have a significant impact on the market if duties are imposed on all the countries.

Demand is also lackluster in other sectors, with diecast alloyers reporting weakness and oxide demand still slow. General galvanizing demand has held up a little better, although there has also been some competition from imports.

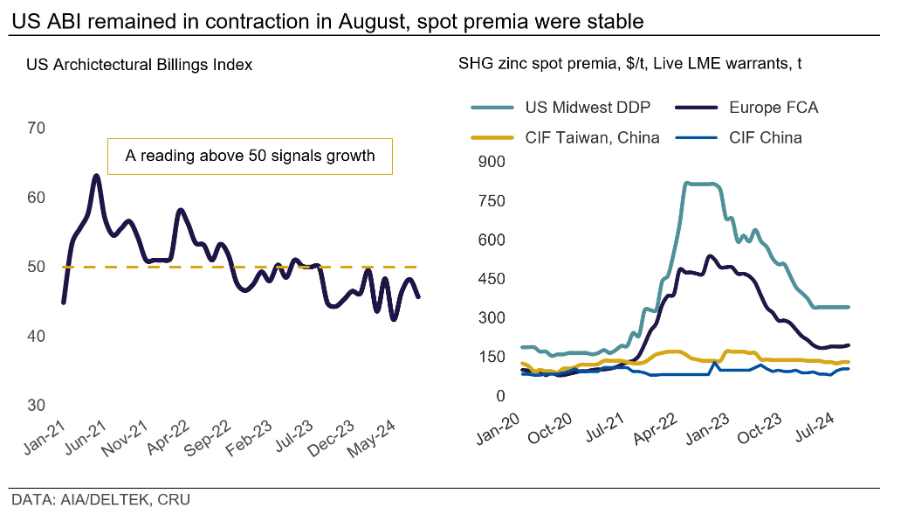

US housing starts and permits ticked up m/m in August, with starts up 3.9% y/y but permits down by 6.5%. Meanwhile, the forward-looking AIA/Deltek Architect Billings Index signaled that business conditions remained soft for non-residential projects and inquiries in August.

US spot premia unchanged

The US spot market has remained stable over the past month, with little on either the demand or supply side to move the needle on premia. We are rolling over our assessment at 15.5 ¢/lb.

Learn more about CRU’s services at www.crugroup.com.