CRU

June 27, 2025

CRU: US stainless prices to rise on expanded S232 tariffs

Written by Brett Reed & Yuriy Vlasov

Stainless prices in the US market will rise, following price increases by major US producers. Our base case scenario incorporates higher US prices in the near term, despite the initial negative reaction by the market.

US stainless prices will go up in 2025 H2 and will stay elevated in 2026 as tariffs on stainless steel have recently doubled to 50% and expanded to end-user products. Following the recent base price increase by US mills, the market will eventually accept higher prices. Our base-case scenario incorporates some base price softness at the start of 2026 as new domestic capacities will come on stream. If left intact, the tariffs will lift domestic prices, allowing imports to gain market share, predominantly from low-cost regions in Asia.

Doubling tariffs primed mills to raise base prices

The initial reaction to the introduction of 25% tariffs in March 2025 from US domestic mills was somewhat muted, in sharp contrast to the immediate response from the US carbon market (see our Insight for more details: Sheet prices will soon peak as markets readjust to tariffs). Doubling tariffs to 50% and expanding it to the value of steel in a variety of imported household goods (see A 50% S232 tariff will raise US steel prices and shift trade flows) prompted domestic mills to raise base prices.

On 13 July, North American Stainless – the largest US stainless producer – announced higher base prices by reducing discounts by 8 points for generic austenitic grades (CR 304) and 9 points for generic ferritic grades (CR 430). Outokumpu USA – another leading player in the US market – followed suit, albeit with some delay, announcing a 4-point discount reduction for generic austenitic grades (CR 304) and a 9-point discount reduction for generic ferritic grades (CR 430). We estimate these measures will translate into base price increases of 11–22% and an all-in price increase of 5–10% against US domestic CR 304 prices assessed in May 2025.

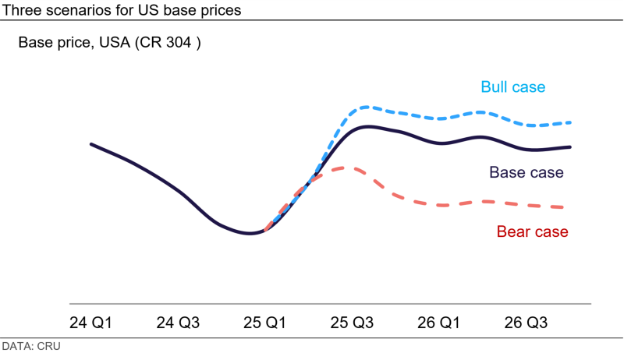

Base case: Section 232 tariffs are here to stay at 50%

Our current base case is that tariffs remain at 50%, which is why US prices remain notably higher than those elsewhere. In the near-term, trade deals are most likely to be reached with USMCA partners, Mexico and Canada, which will have a limited effect on prices in the US. Domestic producers will be able to maintain elevated prices throughout the forecast period as the 50% tariff on key exporting countries to the US is expected to remain in place. Despite these tariffs, imports from lower cost producing countries in Asia will still be able to compete in the US market, maintaining import volumes. We have seen exporters remain aggressive on offers to secure orders to the US, which we expect to continue.

We have also seen domestic mills increase prices for ferritic grades more aggressively than that of austenitic. Mills have shown a greater willingness to produce higher-priced and higher-margin austenitic grades as opposed to ferritic grades. This will open the door to stable, or even higher, import volumes of non-nickel bearing grades of stainless steel.

Bear case: Tariffs are reduced for key exporting countries

There remains the potential for more trade deals to be reached. It is unlikely that the 50% Section 232 tariff will be reduced entirely. It is more likely that individual countries can get their S232 tariff rate reduced, like that of the UK which is at 25%. If we see trade deals reached with key stainless exporting countries, especially those in Asia, prices in the US will come under pressure. Risks will remain as we’ve seen tariffs change overnight. However, exporters have shown a high degree of willingness to take on the risks associated to secure orders.

Bull case: Tariffs expand downstream

Our bull case is based on the scenario of tariffs expanding further downstream. If trade deals are not reached, there is the potential for additional tariffs on downstream products. We have seen steel derivatives under S232 expand, impacting key stainless containing goods with tariffs only applied to the steel component of these products. If retaliatory tariffs expand to the entire value of steel-containing products, the market will experience higher demand for stainless in the US through some degree of reshoring, providing upward support to prices. Escalating tariffs will affect the established logistical links, delivering additional upside to domestic prices in the US market.

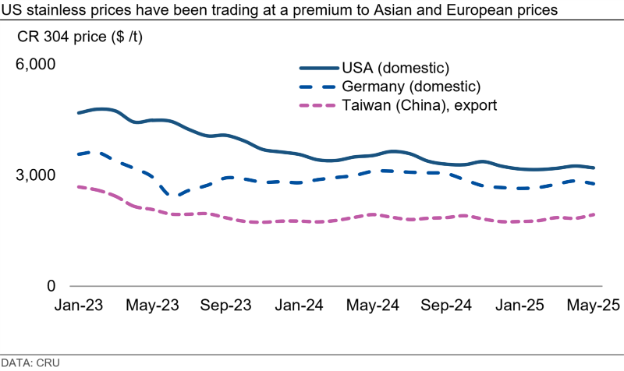

Imports to the US to remain, supported by economics

We forecast the US market to remain a net importer with low-cost Asian imports dominating the import supply. Based on our base case scenario, the structure of imports will change. The share of the Asian imports will expand at the expense of imports from high-cost geographies, such as Europe, Japan and Korea. This will be applicable to generic stainless grades that could be sourced from Asian mills.

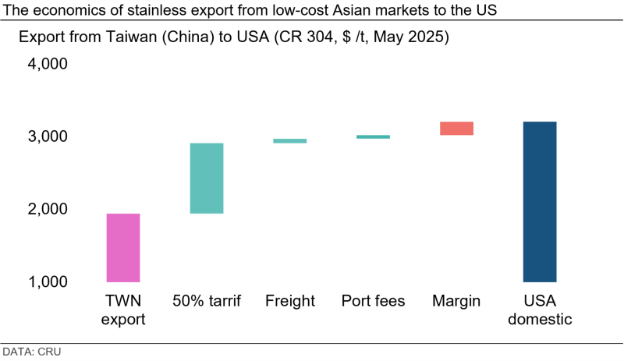

Our analysis indicates that even at 50% tariffs, the imports from low-cost Asian destinations, such as Taiwan (China), Indonesia, China, Malaysia, etc., will remain profitable. Even with a 50% imporWe consider the tariffs to be used mainly as a negotiation token rather than the tool for domestic market development, given the speed at which the tariffs were imposed, doubled and expanded downstream. The example of UK, negotiating 25% tariffs, indicates to us that any potential trade deals are to be done within the inner circle of close trade partners (Canada, Mexico) and close economic allies (European Union, Japan, South Korea). t tariff and $110 /t freight and port costs, exports of CR 304 from Taiwan (China) will carry an attractive margin against US domestic price. This trade is restricted by long lead times (9–10 weeks) while domestic mills have shorter lead times (4–6 weeks).

We consider the tariffs to be used mainly as a negotiation token rather than the tool for domestic market development, given the speed at which the tariffs were imposed, doubled and expanded downstream. The example of UK, negotiating 25% tariffs, indicates to us that any potential trade deals are to be done within the inner circle of close trade partners (Canada, Mexico) and close economic allies (European Union, Japan, South Korea).

Tariffs did not stop the shrinkage of the US market

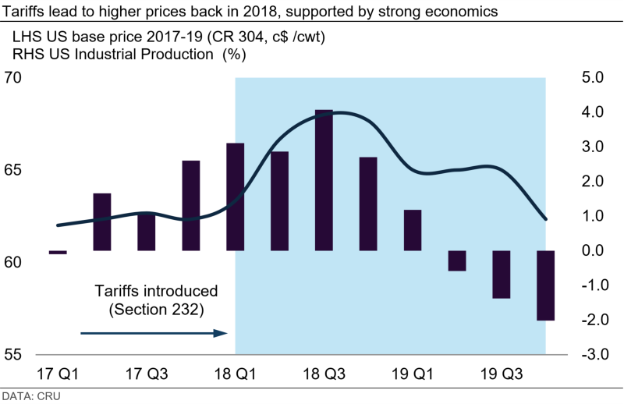

The US stainless market is not new to import tariffs. On 8 March 2018, the US Government imposed 25% tariffs on imported steel and aluminum under Section 232 of the Trade Expansion Act of 1962. As a result, stainless base prices increased by 5–7% over the next two quarters, after which they declined. The economic background in the US at that time was much stronger than now, with US industrial production staying above 3% during 2018. The current economic outlook for the US market is quite different today. CRU’s latest Global Economic Outlook published on 30 May downgraded its economic forecast for the US, expecting a negative industrial production in 2025 and 2026 Q1. Given the weak economic environment, the US market will show more resistance towards announced price hikes.

The introduction of S232 was made with the idea of stimulating domestic production. The result was somewhat different – US crude stainless production declined by 30% from 2017 to 2024. Higher domestic stainless prices led to a shrinkage of the US addressable end-user market, prompting many end-users to transfer their operations outside the US.

Will we see history repeat itself?

Back in 2018, Section 232 tariffs did not incentivize end-users to grow production within the US. With higher prices set to hit the US market, importing finished goods from lower cost markets remains optimal. This surge in prices has left many users looking for alternative options, whether it’s offshoring production or substituting stainless steel with alternative materials. It is likely we will see higher imports of finished goods weighing on stainless consumption in the US as producers chase higher margins over volumes. This will pose challenges for the domestic market as new CRC capacity comes online in early 2026.

We forecast positive industrial production growth from 2026 Q2, supporting domestic demand. However, persistently high prices will drive buyers to seek cost savings, whether it’s through imports, offshoring or even substituting stainless for lower cost material.

This piece was first published by CRU. To learn about CRU’s global commodities research and analysis services, visit www.crugroup.com.