Mills

November 7, 2025

U.S. Steel posts strong Q3 as Nippon centers it in global growth strategy

Written by Laura Miller

Nippon Steel is positioning U.S. Steel as a cornerstone of its global growth strategy.

In its most recent financial statements, Nippon reported facing structural challenges in Japan and sluggish demand across global markets. Thus, the Tokyo-based steelmaker is shifting its focus towards regions with stronger growth potential and more stable demand fundamentals.

In its quest to reach 100 million metric tons of steelmaking production capacity, the company is actively expanding its presence in India, Thailand, and the United States. It selected the three strategic operational bases based on their market volume, resilience against Chinese export pressures, and appetite for high-grade steel.

Among these regions, Nippon highlighted the US as the most developed and demand-rich market, especially for premium steel products used in the automotive, energy, and infrastructure sectors.

The two companies unveiled an aggressive capital investment plan this week, with Nippon set to inject $11 billion into U.S. Steel‘s facilities over the next three years. The plans highlight Nippon’s faith in the US market and the company it spent almost $14 billion to acquire.

The acquisition of the iconic Pittsburgh-based steelmaker was finalized in June this year. However, Nippon decided to exclude USS’ earnings contribution from its fiscal 2025 results due to equipment issues at Clairton Coke Works, market softness, and a one-off loss of JPY232 billion (~US$1.5 billion) tied to the divestiture of equity interests in AM/NS Calvert.

USS contributions

U.S. Steel also released third-quarter financial information this week, showing stronger top-line momentum, especially in its Mini Mill and Tubular segments. But cost inflation and weaker European demand kept overall earnings in check.

As a whole, U.S. Steel posted net sales of $4.43 billion in the third quarter, a 15% rise from $3.85 billion a year earlier. Shipments reached 3.9 million short tons, a modest lift from the quarter before.

Net income came under pressure, though, falling 16% year over year to $100 million. Higher costs ate into margins, especially in the Flat-Rolled and Europe segments, the company reported.

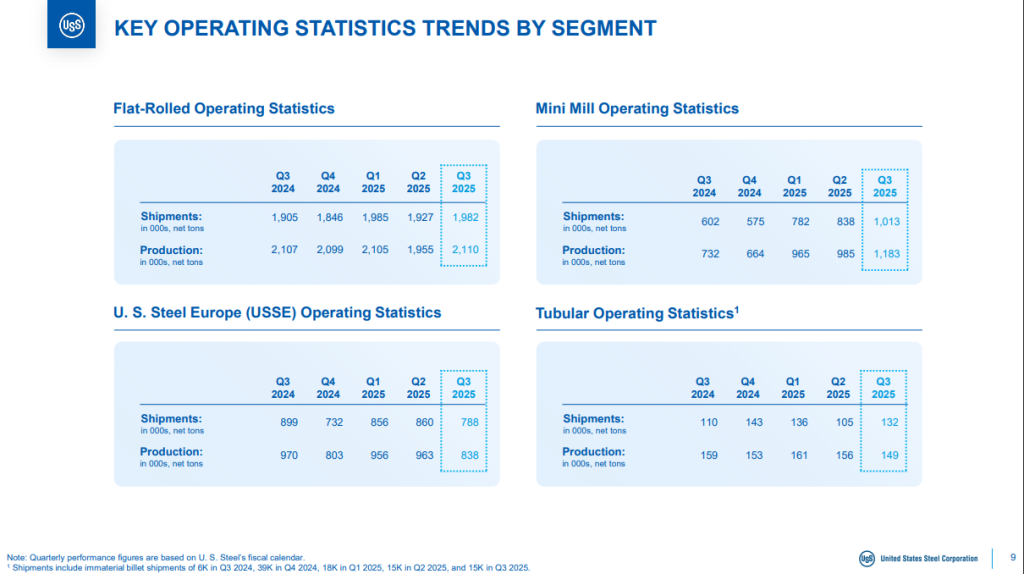

Flat-Rolled

Flat-Rolled Segment sales rose 6% year over year (y/y) to $2.51 billion. Shipments hit 1.98 million st, slightly higher than in the previous quarter and the same quarter last year.

EBITDA came in at $214 million, down from $222 million in Q2’25 and $246 million in Q3’24. Margins slipped to 8% as raw material and energy costs weighed on results.

Mini Mill

The Big River Steel segment in Arkansas was the company’s star performer in the quarter. BR2 continued to ramp up and was EBITDA positive in Q2’25 and Q3’25, USS noted.

Mini Mill segment sales jumped 86% y/y to $939 million, as shipments surged 21% quarter over quarter and 68% y/y to 1.01 million st.

EBITDA hit $135 million, a 33% sequential increase from $101 million and a huge jump from $22 million in Q3’24. Margins improved to 13%, driven by higher prices and BR2’s strong contribution.

U.S. Steel Europe

USSE sales fell 5% y/y to $708 million. Shipments dropped to 788,000 st, down from 860,000 st in Q2’25 and 899,000 st in Q3’24.

EBITDA slipped to $31 million from $39 million last year. Margins narrowed to 4%.

Demand remains soft, the company said, though lower raw material costs and currency tailwinds helped cushion the impact.

Tubular

Tubular segment sales rose 25% y/y to $272 million. Shipments climbed to 132,000 st, up 26% from the previous quarter and 20% from the year-ago quarter.

EBITDA improved to $26 million, compared with $9 million in Q3’24.

Margins increased to 10% due to better pricing and lower operating costs, although the nine-month picture revealed pressure from a weaker product mix.