Analysis

December 5, 2025

CRU: Will carmakers switch back from aluminum to steel?

Written by David Leah

This news item was first published by CRU. To learn about CRU’s global commodities research and analysis services, visit www.crugroup.com.

Recent supply constraints, price increases, shifts in electric vehicle (EV) and emissions policy, and continued innovation in steel have revived the question of whether automakers might move some applications back from aluminum to steel. We expect some switching, but this change is nuanced, multiple factors must be considered, strategies will differ, and there is no one-size-fits-all solution.

Steel has lost share, but remains dominant auto material

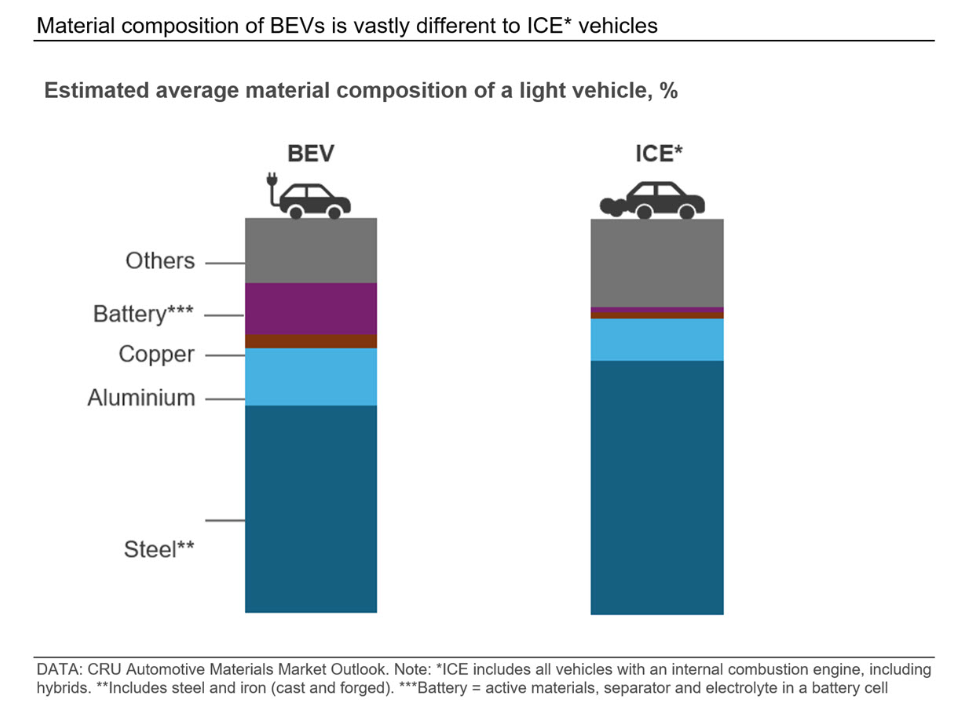

Steel remains the dominant automotive material despite losing share over the last decade. On a weighted-average curb-weight basis, steel (including cast and forged iron) accounts for around 64% of the curb-weight of an internal combustion engine (ICE) light vehicle and about 53% of a BEV.

On a weighted-average curb-weight basis, aluminum’s average content is around 11% of an ICE light vehicle and 15% in a BEV. Average aluminum content had increased, as automakers sort to improve efficiency, meet fleet-average CO2 and fuel economy targets, and offset battery mass. This has been especially true in Europe and North America, where regulatory pressure and vehicle sizes are typically higher. North American aluminum content is above the global average and some models, such as the Ford F 150, use extensive rolled aluminum in the body.

Policy changes have eased pressure to lightweight

Over the last year or so, several emissions and EV related policies have been delayed or watered down, easing the regulatory imperative to lightweight aggressively. Some OEMs may prioritize sales of ICE and hybrids, which are generally more profitable and less aluminum intensive than BEVs.

If this softer policy environment persists, aluminum demand will underperform compared to our previous forecasts, which were made with the stricter policy assumptions. However, that does not mean we will see a wholesale swing back to all steel designs. Such changes usually coincide with vehicle facelifts or new platform launches, and must be justified on cost, performance, and brand positioning.

Aluminum has become relatively more expensive than steel

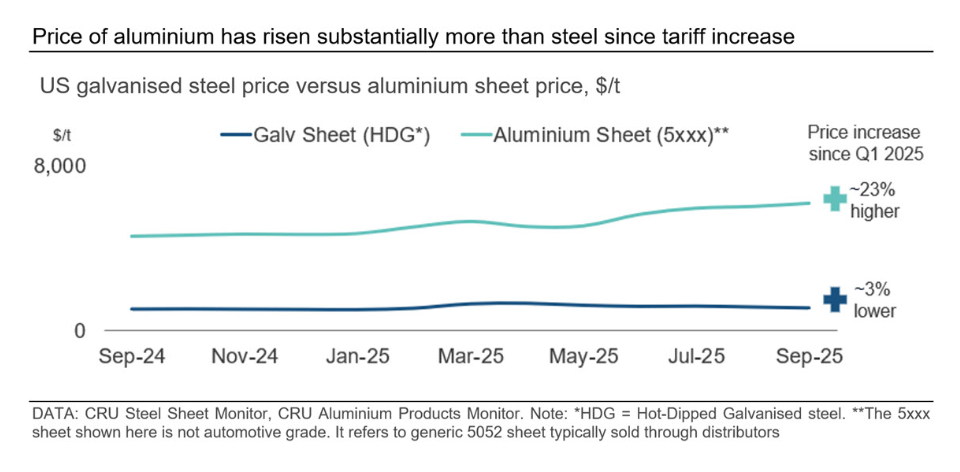

In the US, since Section 232 tariffs were re imposed, first at 25% and then at 50%, aluminum sheet prices have risen more than steel. Steel prices have been relatively stable on ample domestic capacity, whereas aluminum has been constrained by tighter supply and limited domestic production. Aluminum has always been more expensive than steel, with the exact delta depending on grade, product, and specification. Although aluminum is lighter and offers more part area per metric ton, on a per-vehicle basis it still tends to be the more expensive material choice than steel.

The recent widening in relative cost increases the incentive to reassess material choices. Higher aluminum prices make switching back to steel more attractive, especially as advanced high-strength steels offer better performance to mass ratios than conventional steel grades. Yet, any substitution is highly application specific and must respect crash performance, formability, corrosion, joining, and process integration. Also, aluminum prices have not risen as much relative to steel in other regions, such as Europe and China, in recent months.

Material and manufacturing innovations continue to evolve

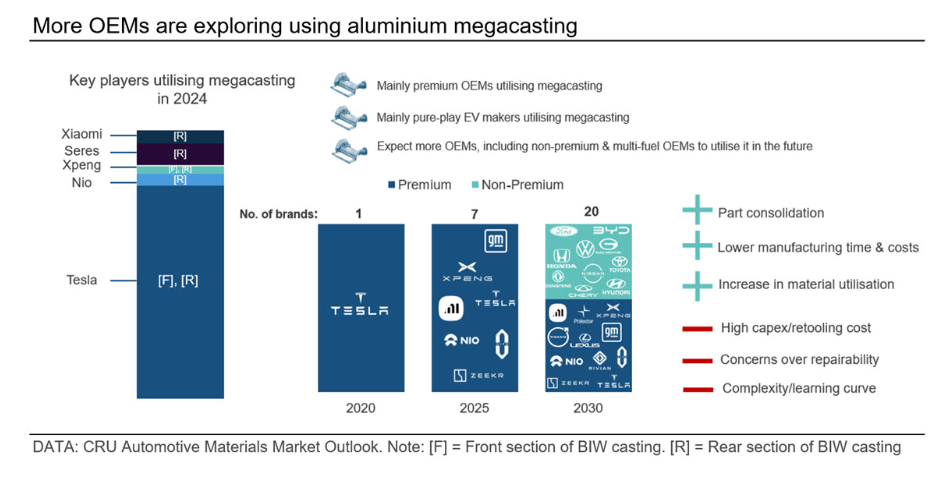

Aluminum’s demand from the automotive sector has been supported by higher usage of aluminum flat rolled products and extrusions in BEVs, given their light weight, energy absorption and relative ease of manufacturability. We have even seen some OEMs adopt aluminum megacastings, which consolidate multiple parts into a single large structural casting, reduce part count and assembly steps, and improve material utilization. This is particularly attractive in BEVs for rear underbody structures and closely aligns with “unboxed” manufacturing processes that a number of OEMs are exploring.

Steelmakers have advanced significantly, expanding grades of AHSS, UHSS, and press hardened steels, improving formability and crash performance, and developing joining and corrosion solutions tailored to modern body structures.

Cleveland-Cliffs’ reported trials of producing exposed steel parts on lines originally set up for aluminum stampings point to lower retooling costs and shorter switching timelines for some parts. However, not every aluminum part can simply be “dropped in” as steel: press capability, surface quality, downstream joining, and corrosion performance still determine what is feasible.

BEV mix, battery costs and OEM strategies are evolving

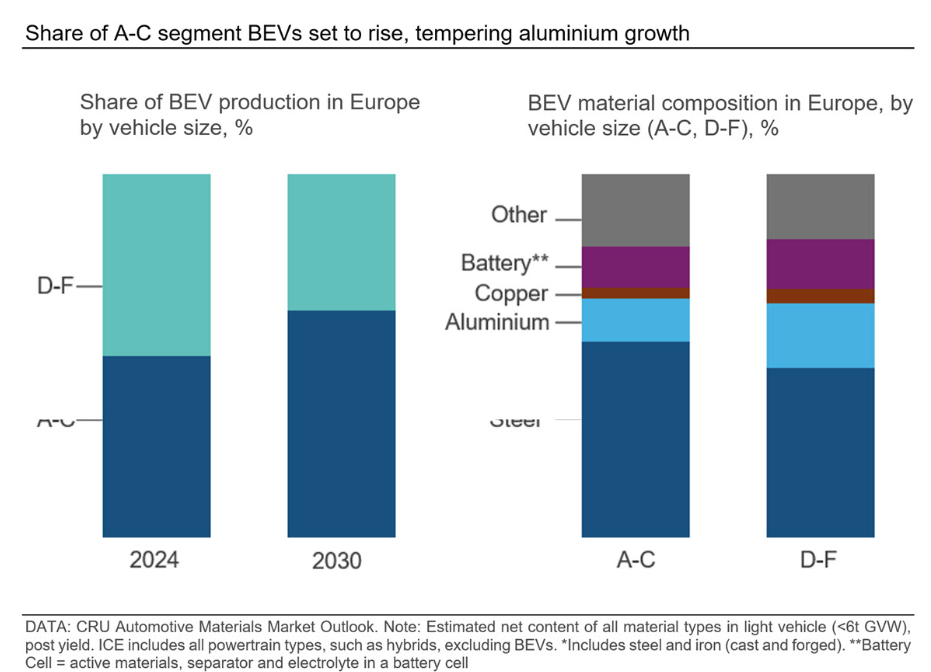

Segment mix is a key driver of material intensity. Early BEVs were concentrated in larger, premium D–F segments, such as the Tesla Model S/X and Jaguar I Pace, where the case for aluminum rich designs is strongest.

Over the forecast period, Europe is expected to see a shift toward smaller A–C class BEVs, rising from about 53% to around 65% of BEV production, bringing the BEV mix closer to the broader market. This shift to smaller, cost-sensitive vehicles tends to reduce average aluminum content per BEV and lift the relative share of steel. In China, where BEVs are already dominated by A–C segments, the D–F share is expected to rise, but aluminum intensity will likely remain below European and North American levels due to tighter cost constraints.

Falling battery costs also weaken the business case for lightweighting. When batteries are cheaper, the economic benefit of saving each kilogram is smaller, particularly once vehicles already achieve adequate range. This favors more cost-effective solutions – often advanced steels – over extensive aluminum use in high volume, mid-market BEVs.

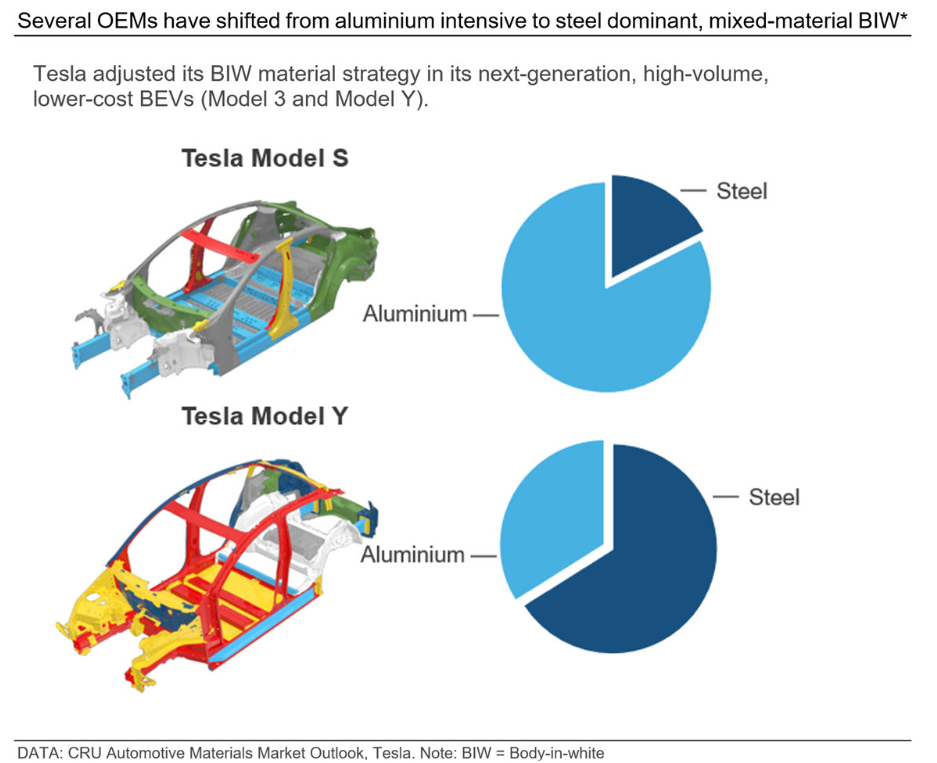

OEMs are already adjusting. Tesla’s Model 3 and Model Y use less aluminum overall than the Model S and Model X, switching to a high steel, mixed material structure to improve manufacturability, reduce costs, and considering the different market positioning of these models. Within aluminum, flat-rolled product intensity in BEVs is set to decline (from a high base) while cast aluminum’s share should increase, driven by megacastings. Tesla and others have also moved back toward more steel in the BIW and closures on newer platforms. More OEMs could follow a similar pattern: more targeted use of aluminum where it adds the most value, combined with greater reliance on steel in mainstream structures.

Steel to regain share, though substitution varies

We do not expect a wholesale return to all steel designs, even with recent market and policy shifts. Mixed-material designs will remain the preferred approach, although outcomes will vary by OEM, product form, component and grade. Platform architectures are long lived, and aluminum remains essential for offsetting battery weight, improving efficiency, and providing robust crash protection, particularly for BEVs.

We expect some changes in material composition, particularly as the BEV mix evolves, affecting average aluminum intensity. Cost sensitive, high volume BEVs are likely to use more steel, and next generation, premium BEVs may also look to use less aluminum for certain parts relative to their predecessor platforms.

Changes are also expected to the aluminum product form mix, with rising use of castings in BEVs displacing other aluminum products and, in some cases, threatening steel’s share. Nonetheless, despite shifts in aluminum product mix and some substitution towards steel, overall aluminum demand from the auto sector is still set to rise alongside BEV growth, with aluminum intensity in a BEV remaining higher than in an ICE vehicle. Switching costs have fallen and steel is set to regain some market share in BEVs, but the extent varies by region, vehicle segment, component type, product

For more information or to request a demo of the new Automotive Materials Market Outlook, please get in touch.