Canada

February 9, 2026

Cliffs logs big loss in '25, sees better times in '26

Written by Laura Miller

Cleveland-Cliffs Inc.

| Fourth quarter ended Dec. 31 | 2025 | 2024 | Change |

|---|---|---|---|

| Net sales | $4,313 | $4,325 | -0.3% |

| Net earnings (loss) | $(243) | $(447) | 45.6% |

| Per diluted share | $(0.44) | $(0.92) | 52.2% |

| Twelve months ended Dec. 31 | |||

| Net sales | $18,610 | $19,185 | -3.0% |

| Net earnings (loss) | $(1,478) | $(760) | -94.5% |

| Per diluted share | $(2.91) | $(1.58) | -84.2% |

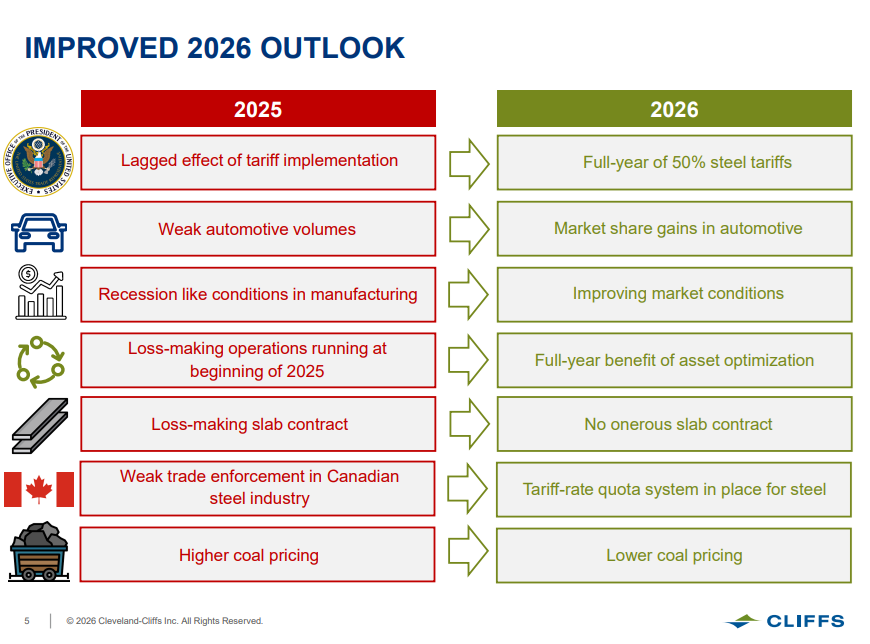

Cleveland-Cliffs Inc. continued to bleed red in the final quarter of 2025. But the steelmaker expects profitability to improve in 2026 with a troublesome slab contract behind it and more protections from imports in place.

Q4 and full-year 2025 earnings results

Cliffs logged nearly 3.8 million short tons (st) of external sales volumes in the fourth quarter of 2025, down 1.5% year over year. For the full year, the Cleveland-based steelmaker posted shipments of approximately 16.2 million st, up 4.1% from 2024. As for product mix, it was 40% hot-rolled (higher due to full-year contribution of Stelco), 28% coated (primarily galvanized), 15% cold-rolled, 9% slabs, 5% plate, and 3% stainless and electrical steels.

Q4’25 sales of $4.31 billion were essentially flat from a year earlier, while full-year sales of $18.6 billion were down 3%. All told, Cliffs posted a net loss of $243 million for the fourth quarter, improved from a loss of $447 million a year earlier. This brought the company’s annual net loss for 2025 to $1.48 billion, nearly double the $760 million annual loss in 2024.

“Our performance in 2025 was negatively affected by persistently weak production levels from the automotive sector throughout the entire year, an expiring five-year slab contract becoming value-destructive during its last year, and a newly adverse dynamic in the Canadian market,” Cliffs Chairman, President, and CEO Lourenco Goncalves said.

“Fortunately, as we started 2026, these negative situations have all improved. At the same time, the trade environment in the United States continues to move in a very constructive direction, setting the stage for dramatically improved results this year,” he added.

Cliffs expects Q4’25 to be the trough in its quarterly profitability, according to a presentation released with its 2025 earnings report.

“2025 was about fixing what needed to be fixed, making tough but necessary decisions, and positioning Cleveland-Cliffs for sustainable performance in a fundamentally improved market,” CFO Celso Goncalves, Lourenco’s son, said during an earnings conference call.

“As we move through 2026, we are operating with a leaner footprint, a stronger order book, improving price realization, declining unit costs, and a clear line of sight to higher utilization and cash generation,” he added.

Trade

Company executives portrayed trade as a central driver of Cliffs’ current challenges and future upside. On the earnings call, management repeatedly attacked steel imports for “poisoning” the US and Canadian markets and forcing idlings and shutdowns in 2025.

Executives also strongly endorsed Section 232 tariffs of 50%. They said higher tariffs drove improved market conditions along with melted-and-poured rules that favor domestically produced steel.

Cliffs executives described Canada as having become a “dumping ground” for steel from foreign producers seeking to avoid US tariffs. This hurt Canadian pricing until Ottawa imposed import restrictions late in 2025. These steps, while “insufficient,” have stopped the “bleeding,” Lourenco said.

“As a result, we have seen Canadian pricing and shipments improve in the last month,” he added.

Automotive

US vehicle production declined in 2025 for the third consecutive year, which hurt Cliffs’ shipments and utilization. Despite that, management sees the decline as cyclical rather than structural. And they view a return to pre-Covid US vehicle production levels as “inevitable” thanks to policy-driven reshoring to the US.

Throughout 2025, Cliffs “geared up” for the expected rebound in auto production by signing multi-year fixed-price contracts with all major automotive OEM customers. This secured high-margin business that will “flow through into 2026,” company executives said.

Cliffs’ leaders stressed that the company already has the installed capacity to serve higher auto demand. And so the company does not need to build new plants but can absorb additional auto volumes within its existing footprint.

Lourenco reasoned that increased US-made auto production was key to lifting Cliffs’ capacity utilization across several downstream facilities.

Management also described a major opportunity to replace aluminum with Cleveland-Cliffs’ steel in automotive applications. They said they had demonstrated across three OEMs that advanced steels could be stamped on existing aluminum-forming equipment. That way, OEMs don’t need new tooling or capital investment to switch.

Cliff executives also described the US aluminum supply chain as fragile and unreliable. They think that means an opportunity to use US-made steel to replace aluminum on exposed automotive components.

Slab contract

The company’s “onerous” slab contract with ArcelorMittal expired at the end of 2025. The contract came with Cliffs’ acquisition of ArcelorMittal USA in 2020. It was based on Brazilian slab prices because Brazil was the largest slab exporter at the time. Management said the contract “worked” for four of the five years. But in 2025, the Brazilian slab price decoupled from US hot-rolled coil prices, turning the contract “into a disaster,” company executives said.

Cliffs tried to renegotiate the contract but was unsuccessful, so they took a hit. Now that the contract has ended, Cliffs can use melting capacity previously allocated to low-margin slab sales to produce higher margin flat-rolled products. Lourenco estimated a ~$500 million gain simply by replacing the semi-finished slabs with finished steel business.

But the company remains open to selling slabs on the open market. There is one condition: “as long as we can agree on a pricing construct that makes sense,” Gonclaves said.

POSCO partnership

Cliffs executives said the company’s top strategic priority is a previously announced partnership with POSCO, a South Korean steelmaker. They see the partnership as a way to deepen industrial cooperation, while helping POSCO meet melted and poured requirements in the US market.

POSCO is still conducting due diligence, Lourenco said. But he stressed that it was POSCO that approached Cliffs, not the other way around. He saw that as highlighting Cliffs’ bargaining strength.

“Both parties are focused on structuring a transaction that is highly accretive and strategically compelling for each company,” Lourenco he added. “The duration of these negotiations reflects the seriousness and potential scale of opportunity.”

The two companies are targeting the first half of 2026 for signing a definitive agreement. “One thing to keep in mind,” Lourenco noted, “our Cleveland-Cliffs board of directors will not approve any deal that’s not accretive to our shareholders.”

Capex

In 2025, Cliffs recorded its lowest capital expenditures in a single year, spending only $561 million.

Company executives estimated capex for 2026 to be ~$700 million. That reflects “more normalized maintenance capital, as well as some pre-work and a coke plant upgrade ahead of the Burns Harbor furnace C reline plan for 2027,” Celso noted.

For 2027, Cliffs estimate capex will be ~$900 million. It will be higher mostly because of the Burns Harbor reline.

Outlook

Cleveland-Cliffs cited multiple reasons for an improved outlook for 2026.

While shipments slipped to 3.8 million st in Q4’25, Cliffs expects Q1’26 shipments to “improve back to the 4 million ton level, again, driven by improved demand and less maintenance time at our mills,” Celso said.

Cliffs anticipates incremental automotive volume this year, driven by higher US vehicle production and market share gains from the company’s multi-year contracts with automakers.

Celso summed up the company’s position heading into 2026: “Our order book is solid. Demand is improving. Lead times are going out. Prices are rising. Costs are still coming down. Tariffs are in place. The slab contract is gone. Manufacturing is coming back. Unemployment is low. Rate cuts are here. Tax refunds are coming. Stelco is contributing. Autos are looking to replace aluminum with steel. POSCO is collaborating. Our employees are incentivized, and our operations and commercial teams are working together towards the same goal – to maximize profitability in 2026.”

“My expectation for full-year 2026 shipment levels is in the 16.5 (million) to 17 million ton range, an improvement from 2025 as we run our mills at higher utilizations,” he said.