CRU

July 17, 2026

CRU Outlook: Global steel export prices will remain under pressure

Written by Juliana Guarana

This item was first published by CRU. To learn about CRU’s global commodities research and analysis services, visit www.crugroup.com.

Steel export prices will remain under downward pressure across most major regions, due to seasonal demand weakness, intensifying competition, and the redirection of trade flows following the EU’s revised tariff-rate quota (TRQ) system.

In the APAC region, Chinese steel export prices are expected to remain depressed over the coming month as construction steel demand is likely to weaken as the hot weather and the rainy season are set to continue across key destination markets. In parallel, domestic steel prices are likely to remain subdued and continue to weigh on export offers. In addition, increasing competition for overseas orders will limit Chinese mills’ ability to maintain previous price levels. However, cost support and already reduced margins are expected to limit the downside in China’s steel export prices, particularly for long products.

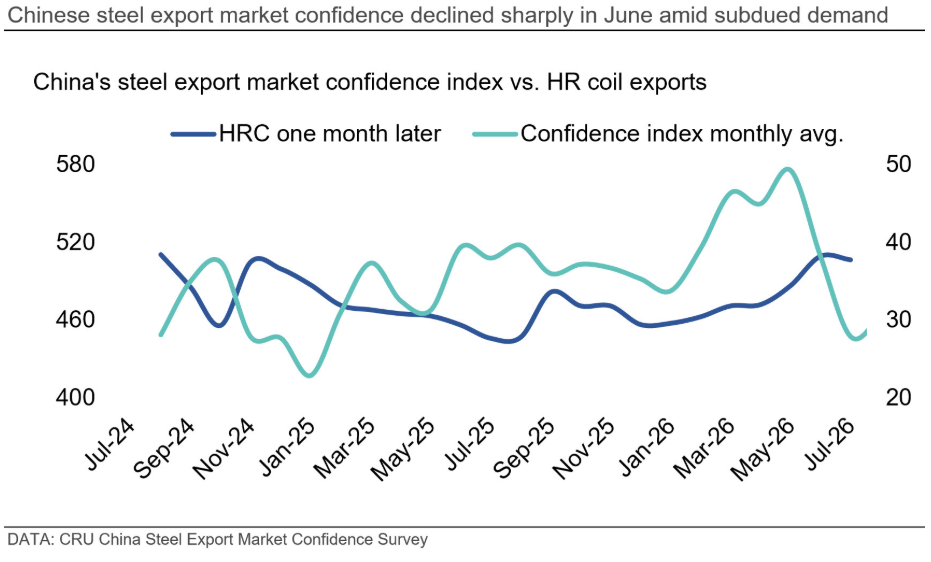

CRU’s China steel export market confidence index declined sharply in June (see chart below), indicating that mills and traders are cautious about trading conditions and price prospects.

Similarly, in Southeast Asia, the downward price trend is expected to continue in the coming weeks due to seasonally weak steel demand. Also, competition within the region is set to increase as suppliers to the EU will redirect more volumes into Southeast Asian markets following the reduction in overall European import quota under the revised TRQ system.

In India, the downward pressure in steel export offer prices is expected to intensify in the coming month due to seasonally weaker domestic demand and prices, which are likely to push mills to increase exports allocation. In addition, given the lack of export prospects to Europe due to the new TRQ system and increased competition within the Asian market, Indian suppliers are expected to reduce their price offers to attract sales. The depreciating Indian rupee is likely to partially offset the impact of this price reduction. In parallel, sheet imports into the country are likely to decline further as Indian buyers are set to avoid exposure during the ongoing anti-dumping investigations against Chinese, Japanese, and Russian hot-rolled flats and electrical steels.

In Europe, the new TRQs will further shift regional demand towards domestic mills and away from imports. Higher capacity utilization at domestic assets, which are, on average, higher cost than imports, is set to support higher steel prices in the region (see related Insight here). As some TRQ for Q3 are already exhausted, higher landed import prices including the out-of-quota duty of 50% are also expected to support steel domestic prices in the region. However, weak regional demand is likely to keep price rises limited in the immediate future.

In Turkey, steel export prices are expected to decline in the coming weeks due to weak seasonal demand in the MENA region and as TRQs for some Turkish steel products have already been exhausted.

In the US, domestic sheet prices are expected to continue rising in the coming months. Supply is set to remain below the levels required to satisfy local demand due to low imports and domestic maintenance outages that will not end until September. Landed import prices will remain significantly lower than US domestic steel prices in the coming month and import volumes into the country are expected to continue to trend upwards amid low domestic availability.

In Brazil, slab export prices are expected to face downward pressure in the coming weeks. Despite steady demand from US and European buyers, lower Asian steel prices are expected to weigh on global slab benchmarks.