Plate market participants anticipate producer hikes

Plate market participants expect domestic producers to issue a $40-60 per short ton (st) price increase.

Plate market participants expect domestic producers to issue a $40-60 per short ton (st) price increase.

The Dodge Momentum Index (DMI) fell 6.2% in January to 272.7, retreating from December’s downwardly revised reading of 291.0, according to the latest data released by Dodge Construction Network.

Baker Hughes' latest rig count report shows oil and gas drilling picked up in the US this week, but slowed in Canada. Oil drilling in both countries is down from last year, while gas drilling has picked up, mainly in the US.

SMU’s Current Sentiment Index for scrap jumped again in February, according to the latest data from our ferrous scrap survey. And the Future Sentiment Index remained the same for the third consecutive month.

GrafTech International closed 2025 with firmer sales volumes and significant cost reductions. But the graphite electrode producer remained deep in the red as global oversupply and aggressive competitor pricing continued to pressure realized prices.

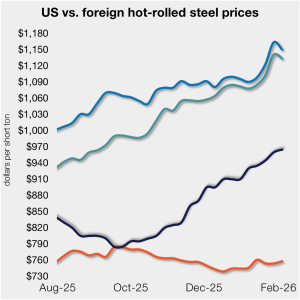

The price gap between US hot-rolled coil and landed offshore product narrowed this week, as price movements stateside and abroad diverged.

November steel exports tumbled 15% from October to the lowest monthly export rate since July 2020.

US rebar and wire rod prices rose month on month (m/m) alongside continued scrap increases, while merchant bar and structurals were unchanged.

One third of the steel buyers responding to our market survey this week reported that domestic mills are negotiable on new spot order pricing. Mills began to hold a firmer stance on prices towards the end of last year, tightening their grip in early January and holding it since.

Steel mill lead times marginally declined on sheet products this week but edged higher on plate, according to responses from SMU’s latest market survey. Overall, lead times remain one to two weeks longer than levels seen three months ago.

U.S. Steel plans to idle the No. 14 blast furnace at its Gary Works near Chicago for a reline for ~100 days from May to August.

Since my last column, confidence within the physical market has been restored. However, that does not mean necessarily confidence in the outlook for demand. More so, it's confidence that better pricing is not lurking around the corner. So where do we go from there?

The US domestic scrap market is largely settled on February pricing. Despite poor weather conditions that have been wreaking havoc on scrap flows and deliveries to consumers, the pricing initially agreed between dealers and steelmakers has been fairly conservative.

Sheet market participants said conditions this week were more stable than in past weeks, but they remain cautiously optimistic overall.

The United Auto Workers (UAW) and Volkswagen have reached a tentative agreement covering 3,200 workers at the automaker's Chattanooga, Tenn., assembly plant.

U.S. Steel plans to restart Battery #13 at its Clairton Coke Works on Feb. 5. Battery #13 was one of the batteries hot idled since a lethal explosion at Clairton on Aug. 11, 2025.

Market participant comments from this month's SMU ferrous scrap survey.

Flat-rolled steel prices inched upward again this week as mixed demand appeared to be offset by limited supplies.

General Motors Canada has laid off ~500 workers at its Oshawa Assembly facility in Ontario, as the plant moves to two shifts of production as of Monday, Feb. 2.

Steel imports remain weak in November and December according to recently released final US Commerce Department data. Many of the sheet and plate products we follow slipped to multi-year lows.

The US Department of Commerce has found that certain steel pipe rolled in Oman using Chinese hot-rolled coil is illegally circumventing anti-dumping and countervailing duties (AD/CVDs).

The export market from the US and Canada has held firm, while slightly strengthening ahead of the domestic buying for February shipment.

There is no evidence that unofficial talks are taking place to secure tariff reductions on Canadian aluminum or steel. One of the biggest challenges is simply understanding what the US actually wants from Canada.

Participants in the hot- and cold-rolled coil markets said winter storms in the East and Midwest may disrupt weekly order volumes and prices.

The latest count of operational oil and gas rigs increased in both the US and Canada this week, according to the latest data released from Baker Hughes.

All but one of the steelmaking raw materials we track increased in price over the last month

SSAB Americas delivered higher shipments and a stronger operating result in the fourth quarter of 2025. The company saw firm demand in key US end markets and a solid finish to the year despite a planned maintenance outage.

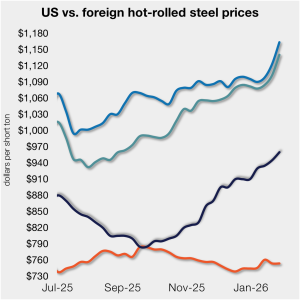

The price gap between US hot-rolled coil and landed offshore product inched higher, even as prices stateside and abroad mostly moved in tandem vs. last week.

The pig iron market has entered an upward phase now that ferrous scrap in both Europe and North America has also been increasing in price.

Sheet prices mostly continued their uneven but steady march higher this week, according to SMU’s latest check of the market.