Prices

March 28, 2017

SMU Price Ranges & Indices: Mostly Unchanged

Written by John Packard

As we moved around the industry trying to gauge where flat rolled steel prices are this week, we found most buyers as being optimistic but perhaps not as many as two weeks ago. There seems to be a growing question about whether the market has “peaked” or not. Everyone wants to know where prices will go from here and there are never any easy answers to that question.

A steel service center executive complained to us about the current high spot prices and their inability to close business at the new numbers, “Using those numbers it is very difficult to get business. I am convinced that we have peaked. Some moderation is in order.”

A steel buyer told us, “I am seeing pricing beyond HRC a little skewed depending on product. We are seeing the HRC market as pretty strong with the resurgence of the energy market. So not a lot of negotiating when it comes to that. CR seems fairly weak with the Russian offers and I am hearing there are South African offers also… Galvanize is 40.50 up depending on the product, what need the mill has, etc. Most of the mills are inquire only so they love to give an all in price and factor the price to what they need in their book.”

We heard from a manufacturing company that provided an interesting view of the current market, “We continue to see steadily rising domestic prices and rising extras. However, mills are negotiating and competing for our share of the domestic business. Offshore, pricing has been steady for the last couple months with threatened price increases not yet sticking.”

Two rays of hope were included in the comments received by Steel Market Update this week:

From a large agriculture equipment manufacturer, “Our business is just now starting to see a little light at the end of the AG tunnel, some plants are seeing some pick-up.”

This is from a large service center that supplies automotive and other large customers, “…We are buying spot when necessary – but still watching inventory and lead time — BUT the good news is that our shipments remain strong and I would say that overall business sentiment is very positive. I feel very good about shipments for April and May and am optimistic about June and July (which is all relative / rarely as strong as 1Q or early 2Q)… Auto releases and forecasts remain good (again all relative – but in most years we would kill for today’s numbers)…”

Here is how we see prices this week:

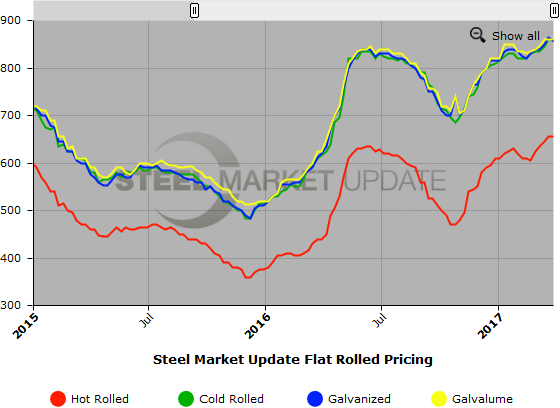

Hot Rolled Coil: SMU price range is $630-$680 per ton ($31.50/cwt-$34.00/cwt) with an average of $655 per ton ($32.75/cwt) FOB mill, east of the Rockies. Both the lower and upper ends of our range remained the same compared to one week ago. Our overall average is unchanged compared to last week. Our price momentum on hot rolled steel is pointing to Higher which means we expect prices to increase over the next 30-60 days.

Hot Rolled Lead Times: 3-6 weeks

Cold Rolled Coil: SMU price range is $840-$880 per ton ($42.00/cwt-$44.00/cwt) with an average of $860 per ton ($43.00/cwt) FOB mill, east of the Rockies. Both the lower and upper ends of our range remained the same compared to last week. Our overall average is unchanged compared to one week ago. Our price momentum on cold rolled steel is pointing to Higher which means we expect prices to increase over the next 30-60 days.

Cold Rolled Lead Times: 4-8 weeks

Galvanized Coil: SMU base price range is $41.50/cwt-$44.00/cwt ($830-$880 per ton) with an average of $42.75/cwt ($855 per ton) FOB mill, east of the Rockies. The lower end of our range decreased $20 per ton compared to one week ago while the upper end remained the same. Our overall average is down $10 per ton compared to last week. Our price momentum on galvanized steel is pointing to Higher which means we expect prices to increase over the next 30-60 days.

Galvanized .060” G90 Benchmark: SMU price range is $908-$958 per net ton with an average of $933 per ton FOB mill, east of the Rockies. Note that we are now using a $78 per ton ($3.90/cwt) extra for this product rather than $69 ($3.45/cwt) due to the revised US Steel galvanized price extras effective April 1, 2017.

Galvanized Lead Times: 5-10 weeks

Galvalume Coil: SMU base price range is $42.00/cwt-$44.00/cwt ($840-$880 per ton) with an average of $43.00/cwt ($860 per ton) FOB mill, east of the Rockies. Both the lower and upper ends of our range remained the same compared to last week. Our overall average is unchanged compared to one week ago. Our price momentum on Galvalume steel is pointing to Higher which means we expect prices to increase over the next 30-60 days.

Galvalume .0142” AZ50, Grade 80 Benchmark: SMU price range is $1131-$1171 per net ton with an average of $1151 per ton FOB mill, east of the Rockies.

Galvalume Lead Times: 5-8 weeks

Plate: SMU price range is $730-$770 per ton ($36.50/cwt-$38.50/cwt) with an average of $750 per ton ($37.50/cwt) FOB mill, east of the Rockies. The lower end of our range decreased $10 per ton compared to one week ago while the upper end fell $20 per ton. Our overall average is down $15 per ton compared to last week. Our price momentum on plate steel is now pointing to Higher which means we expect prices to increase over the next 30-60 days.

SMU Note: Below is a graphic showing our hot rolled, cold rolled, galvanized, and Galvalume price history. We will add plate prices to this graph once we have gathered a few months of data. To use the graphs interactive capabilities, you must view it on our website here. If you need help navigating the website or need to know your login information, contact us at info@SteelMarketUpdate.com or by calling 800-432-3475.