Plate

October 17, 2017

SMU Flat Rolled & Steel Plate Price Indices Indicate Slippage

Written by John Packard

Prior to the ArcelorMittal USA price increase announcement, Steel Market Update analysis of steel prices found flat rolled steel prices continuing their slow slog south (prices are moving lower). The pace has not accelerated, but there are questions as to whether some of the steel mills are cutting “quiet” deals in order to fill their fourth-quarter order book without giving the steel away.

One service center put it to us this way: “If you have index contracts, those prices aren’t that attractive, so my guess is some cheaper pricing must be out there to motivate anyone wanting to buy big volume right now. My guess is in the next two weeks there will be a lot of ‘quiet deals’ being done on volume to get December books full. For those who have learned that they can live comfortably with 2 months of inventory, even a so-called ‘deal’ right now isn’t that attractive, considering we could be entering a phase of lower input cost for an extended period.”

We will have to wait and see if the ArcelorMittal price increase announcement has any impact on lead times or price negotiations with steel buyers. Steel Market Update is keeping our SMU Price Momentum Indicator as pointing toward lower prices over the short term. We will adjust the indicator to neutral as soon as another steel mill follows the ArcelorMittal lead. AM USA has done something interesting with their increase as they have identified the “minimum” base prices for hot rolled ($625 per ton), cold rolled ($825 per ton) and hot-dipped galvanized ($825 per ton). You can compare those base prices against what we are publishing for flat rolled steel prices for this week.

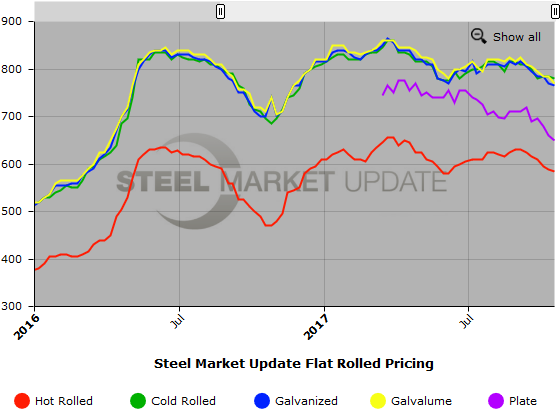

Here is how we see steel prices this week:

Hot Rolled Coil: SMU price range is $560-$610 per ton ($28.00/cwt-$30.50/cwt) with an average of $585 per ton ($29.25/cwt) FOB mill, east of the Rockies. The lower end of our range remained unchanged compared to one week ago, while the upper end declined $5 per ton. Our overall average is down $2.50 per ton compared to last week. Our price momentum on hot rolled steel is pointing to Lower indicating prices are expected to decline over the next 30 days.

Hot Rolled Lead Times: 2-5 weeks (ARTICLE CONTINUES BELOW)

{loadposition reserved_message}

Cold Rolled Coil: SMU price range is $750-$810 per ton ($37.50/cwt-$40.50/cwt) with an average of $780 per ton ($39.00/cwt) FOB mill, east of the Rockies. The lower end of our range declined $10 per ton compared to one week ago, while the upper end remained unchanged. Our overall average is down $5 per ton compared to one week ago. Our price momentum on cold rolled steel is pointing to Lower indicating prices are expected to decline over the next 30 days.

Cold Rolled Lead Times: 4-8 weeks

Galvanized Coil: SMU base price range is $36.50/cwt-$40.00/cwt ($730-$800 per ton) with an average of $38.25/cwt ($765 per ton) FOB mill, east of the Rockies. The lower end of our range remained the same compared to one week ago, while the upper end declined $10 per ton. Our overall average is down $5 per ton compared to last week. Our price momentum on galvanized steel is pointing to Lower indicating prices are expected to decline over the next 30 days.

Galvanized .060” G90 Benchmark: SMU price range is $808-$878 per net ton with an average of $843 per ton FOB mill, east of the Rockies. A note to our readers who also review other galvanized indexes: Right now, not all indexes are using the same G90 zinc coating extra on benchmark .060″ material. SMU uses $78 per ton, while at least one other index is using $86 per ton, which reflects the price change made by NLMK USA. SMU has not yet made a change as we wait for U.S. Steel, ArcelorMittal USA and Nucor to make adjustments to their extras.

Galvanized Lead Times: 3-8 weeks

Galvalume Coil: SMU base price range is $37.00/cwt-$40.00/cwt ($740-$800 per ton) with an average of $38.50/cwt ($770 per ton) FOB mill, east of the Rockies. The lower end of our range fell $20 per ton compared to one week ago, while the upper end declined $10 per ton. Our overall average is down $15 per ton compared to last week. Our price momentum on Galvalume steel is pointing to Lower indicating prices are expected to decline over the next 30 days.

Galvalume .0142” AZ50, Grade 80 Benchmark: SMU price range is $1,031-$1,091 per net ton with an average of $1,061 per ton FOB mill, east of the Rockies.

Galvalume Lead Times: 5-8 weeks

Plate: SMU price range is $620-$680 per ton ($31.00/cwt-$34.00/cwt) with an average of $650 per ton ($32.50/cwt) FOB delivered. The lower end of our range decreased $20 per ton compared to one week ago, while the upper end remained the same. Our overall average is down $10 per ton over the past week. Our price momentum on plate steel is pointing to Lower indicating prices are expected to decline over the next 30 days.

Plate Lead Times: 3-5 weeks

SMU Note: Below is a graphic showing our hot rolled, cold rolled, galvanized, Galvalume, and plate price history. To use the graph’s interactive capabilities, you must view it on our website here. If you need help navigating the website or need to know your login information, contact us at info@SteelMarketUpdate.com or 800-432-3475.