Prices

April 20, 2014

SMU Comparison Price Indices: Are We Peaking?

Written by John Packard

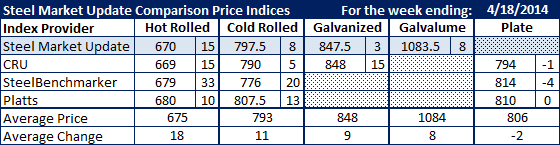

All of the steel indices followed by Steel Market Update saw flat rolled steel prices increase this past week. Benchmark hot rolled coil saw the spread between the indices shrink while the average HR price increased by $17 per ton. Cold rolled was one item where the price spread increased across the various steel indexes with SteelBenchmaker having the lowest average at $776 per ton and Platts at the high end at $807.50 per ton. Both CRU and SMU saw galvanized .060” G90 at $848 per ton. SMU had Galvalume average pricing rising by $8 per ton to $1084 for .0142” AZ50 Grade 80.

With hot rolled averaging $673 per ton ($33.65/cwt) and the last increases announced at $685 and $700 per ton, are we close to the peak of the cycle or will it move higher from here? One item to consider is the spread between foreign offers and domestic pricing as well as lead times.

As one large manufacturing company put it to Steel Market Update over the weekend, “Several mills are still selling spot around $33. Most are pushing higher but now that lead-times have pushed out foreign is a legitimate option, and not just Russian.”

SMU sources have pegged the latest foreign hot rolled offers at $580 (+/-) per ton the port of Houston and $630 per ton (+/-) on the West Coast. A spread of $100 per ton is quite attractive for hot rolled product, especially for those who are located within a reasonable distance from a port.

FOB Points for each index:

SMU: Domestic Mill, East of the Rockies.

CRU: Midwest Mill, East of the Rockies.

SteelBenchmarker: Domestic Mill, East of the Mississippi.

Platts: Northern Indiana Domestic Mill.