Product

January 28, 2013

2012 Imports Projected to be 17% Higher than 2011

Written by John Packard

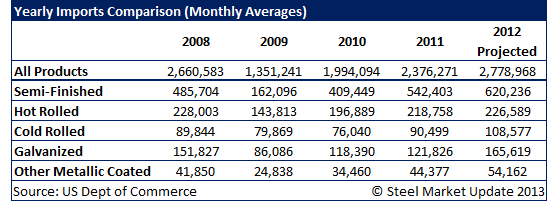

Based on the most recent data released by the Department of Commerce projects 2012 total steel imports to be 33,347,611 net tons – this represents an increase of just shy 17 percent versus the 28,515,247 net tons imported into the U.S. during 2011. Galvanized tonnage was up by 36 percent, Galvalume by 22 percent, cold rolled by 20 percent and semi-finished by slightly more than 14 percent. Hot rolled imports increased by slightly less than 4 percent.

To get a better view of imports take a look at the chart below and go back to 2008 which was the last year before the collapse of the economy. 2008 is the best year to compare 2012 imports.