Market Data

November 7, 2013

SMU MoMo Index Remaining Steady

Written by Brett Linton

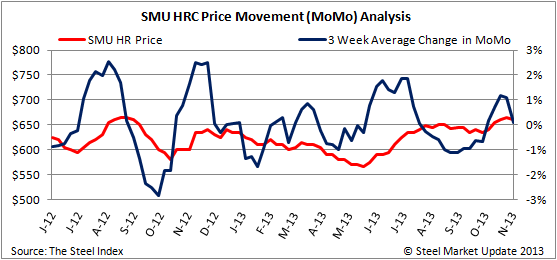

The Steel Market Update Price MoMo Index for flat rolled steel in the U.S. remained positive this week for the 4th week in a row after 4 consecutive weeks of being in negative territory. MoMo, a trailing indicator, is based upon the current hot rolled coil price weighed against the previous 12-week average spot price as recorded by Steel Market Update. MoMo was measured at 1.90 percent this week, meaning that the current HRC price is above the average price from the previous 12 weeks.

The change in MoMo can be a useful indicator in depicting the severity of price movements. Looking at this change on a 3-week moving average, we see that the trend in HRC price fluctuation has began to flatten out after a sharp increase over the last 3 weeks. The 3-week average change in MoMo is 0.07 percent, meaning that the change in HRC prices over the previous 12 weeks has been is very small.

The graph below demonstrates the relationship between the SMU hot rolled coil price and the three week moving average change in MoMo. Our HRC price range for this week is $640-$680/ton with an average price of $660/ton.