Prices

May 20, 2014

Global Steel Production and Capacity Utilization in April 2014

Written by Peter Wright

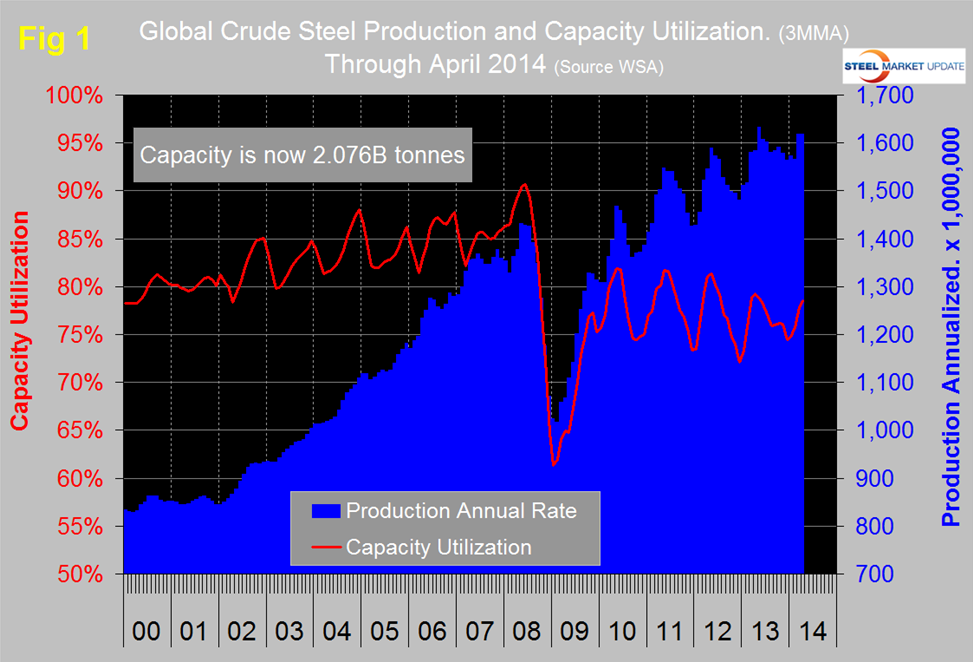

Production in April on a tons/day basis was another all-time high at 4.574 million tonnes. The three month moving average (3MMA) of production in April was at an annual rate of 1.619 billion tonnes with a capacity utilization of 78.5 percent, also a 3MMA, (Figure 1).

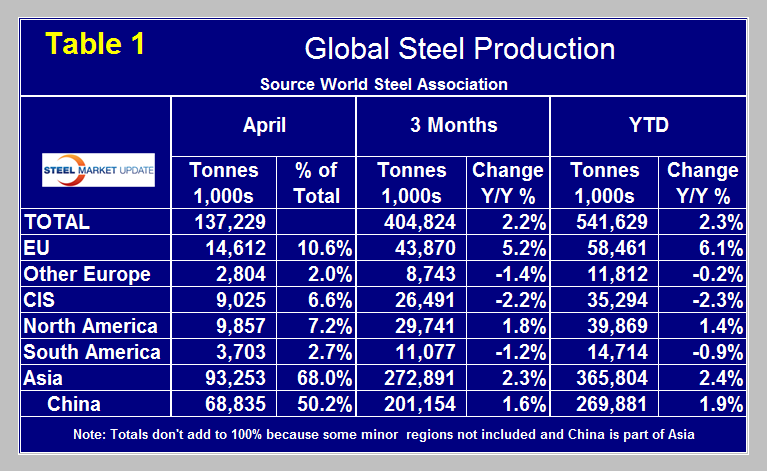

Capacity is now 2.076 billion tonnes. Table 1 shows regional production in April with regional share of the global total, also three months production through April and YTD production. In three months through April year over year (y/y) growth was 2.2 percent. All regions except the CIS, other Europe and South America had positive y/y growth in three months through April with the European Union continuing to lead the way. Growth of output in the NAFTA was 1.8 percent. The growth of China’s steel output has slowed for each of the last six months on a 3MMA basis and in April was 1.6 percent down from 12.4 percent in March last year. It is still too soon to tell if the growth of China’s production really is being reigned in but the signs are encouraging. North America and China produced 7.2 percent and 50.2 percent of the global total in April respectively.

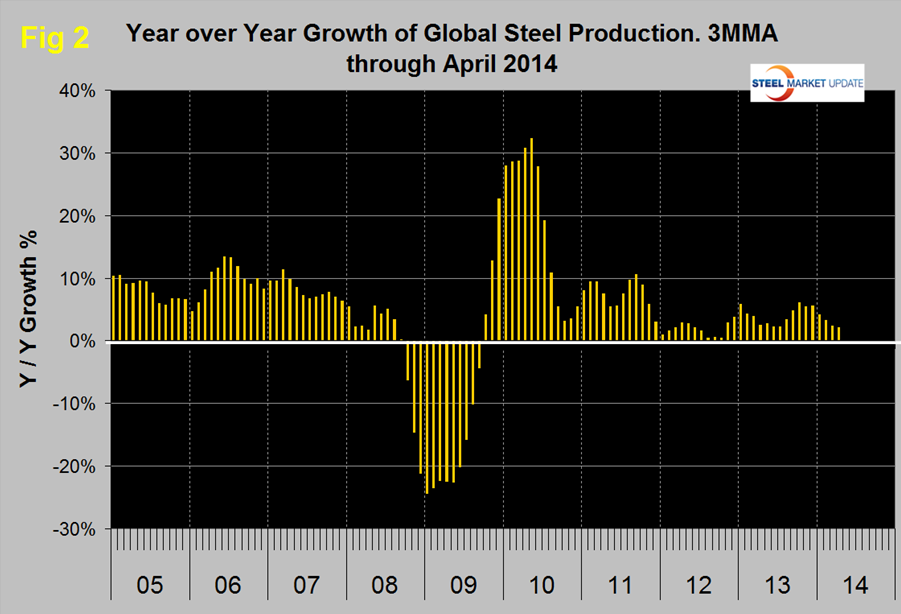

Figure 2 shows the y/y growth of global production. Growth has slowed for each of the last four months but the current 2.2 percent rate is not out of line with the last 28 months of history.

JP Morgan News release, May 5th: The growth rate of the global manufacturing sector eased to a six-month low at the start of the second quarter. At 51.9 in April, the J.P.Morgan Global Manufacturing PMI – a composite index1 produced by JPMorgan and Markit in association with ISM and IFPSM – still signaled expansion for the seventeenth successive month. The slower rate of improvement highlighted by the headline global PMI partly reflected weaker increases in production and new orders. In both cases, the world aggregates were affected by a marked turnaround in the performance of Japan. Japanese manufacturing output and new business fell sharply following a recent increase in sales tax. However, other evidence from the Japan survey suggests the downturn may be brief, providing a boost to the global indices in coming months. In contrast, the UK and the US remained bright spots, with output and new order growth accelerating from already elevated rates. In the euro area, output growth reached a three-month high and was only slightly off of January’s near three-year high. Conditions in Asia remained subdued in comparison. Apart from the sharp downturn in Japan, there was also a solid decline in Chinese output. South Korean and Indonesian output also contracted, while growth slowed in India and Taiwan. Elsewhere, Brazil and Russia both registered lower production. International trade flows also rose again during April, although the rate of increase was modest and among the weakest during the current ten-month sequence of expansion. Global manufacturing employment increased for the ninth successive month in April. Jobs growth was recorded in 22 out of the 26 nations for which April data were available, with China, France, Brazil and Russia the sole exceptions. The Global Report on Manufacturing is compiled by Markit based on the results of surveys covering over 10,000 purchasing executives in 32 countries. Together these countries account for an estimated 89 percent of global manufacturing output. Questions are asked about real events and are not opinion based. Data are presented in the form of diffusion indices, where an index reading above 50.0 indicates an increase in the variable since the previous month and below 50.0 a decrease.

Inflationary pressures remained generally subdued during the latest survey period, with input costs rising at the slowest pace for ten months and selling prices falling for the second straight month. (Source: World Steel Assiciation)