Prices

January 6, 2015

Flat, Long, and Semi-Finished Imports through December 2014

Written by Peter Wright

This is our second article about foreign steel imports where we look deeper into imports from a three month moving average perspective. We also look at the complete picture by analyzing both long and flat rolled steel products.

License data for December was updated on January 6th through the Steel Import Monitoring System of the US Commerce Department. The SMU publishes several import reports ranging from this very early look using licensed data to the very detailed analysis of final volumes by district of entry and source nation which is published in our premium product.

![]() The early look, the latest of which you are reading now has been based on three month moving averages, (3MMA) using December licensed data, November preliminary and October final data. We recognize that the license data is subject to revisions but believe that by combining it with earlier months data in this way gives a reasonably accurate assessment of volume trends by product as early as possible. The main issue with the license data is the month in which the tonnage arrives. We are currently investigating the relationship between licensed tonnage and month of arrival and will publish our summary of the accuracy of license data for the whole of 2014 in this newsletter in early February. Total rolled product licensed imports in the month of December were 2,897,354 short tons which was almost a million tons higher than December last year and was down by 148,000 tons from November.

The early look, the latest of which you are reading now has been based on three month moving averages, (3MMA) using December licensed data, November preliminary and October final data. We recognize that the license data is subject to revisions but believe that by combining it with earlier months data in this way gives a reasonably accurate assessment of volume trends by product as early as possible. The main issue with the license data is the month in which the tonnage arrives. We are currently investigating the relationship between licensed tonnage and month of arrival and will publish our summary of the accuracy of license data for the whole of 2014 in this newsletter in early February. Total rolled product licensed imports in the month of December were 2,897,354 short tons which was almost a million tons higher than December last year and was down by 148,000 tons from November.

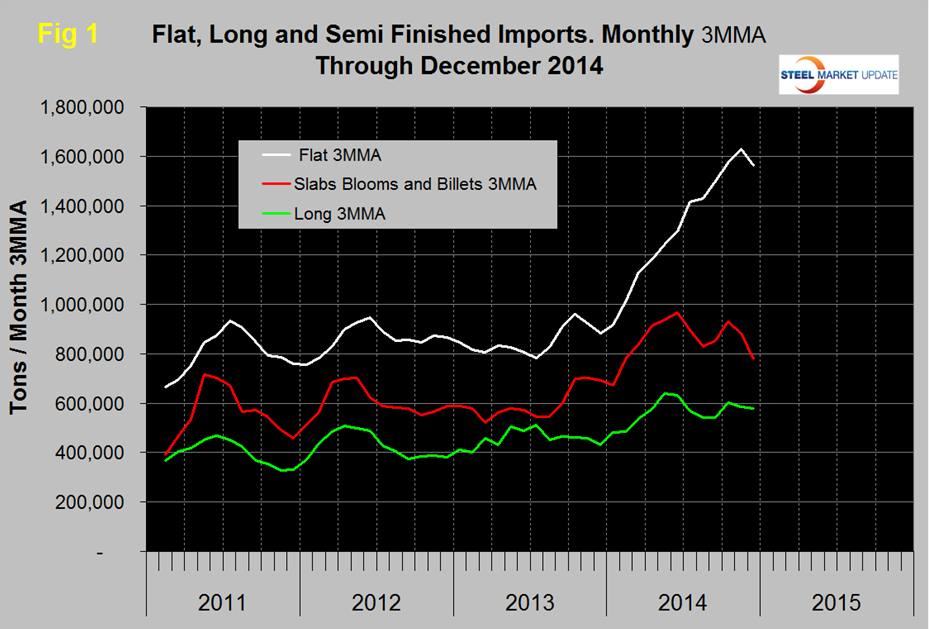

Figure 1 shows the 3MMA through December licenses for semi-finished, flat and long products. Flat includes all hot and cold rolled sheet and strip plus all coated sheet products plus both discrete and coiled plate plus tin plate. The import surge took a breather for flat rolled in December, semi-finished has been trending down since mid-year and longs have also trended down slightly since May.

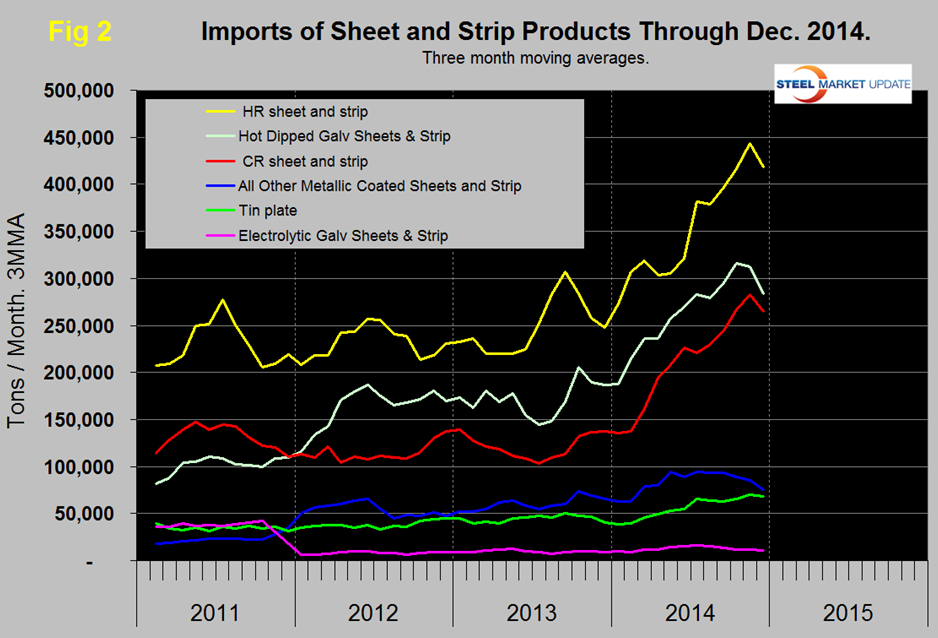

Figure 2 shows the trend of sheet and strip products since January 2011 as three month moving averages. The big three tonnage items, HR, CR and HDG all declined in December. All other metallic coated, (mainly Galvalume), has declined slightly since mid-year. Tin plate has been trending up for all of 2014. In the single month of December hot rolled sheet and strip licenses were 342,401 tons, HDG was 233,223 and cold rolled came in at 235,270 tons.

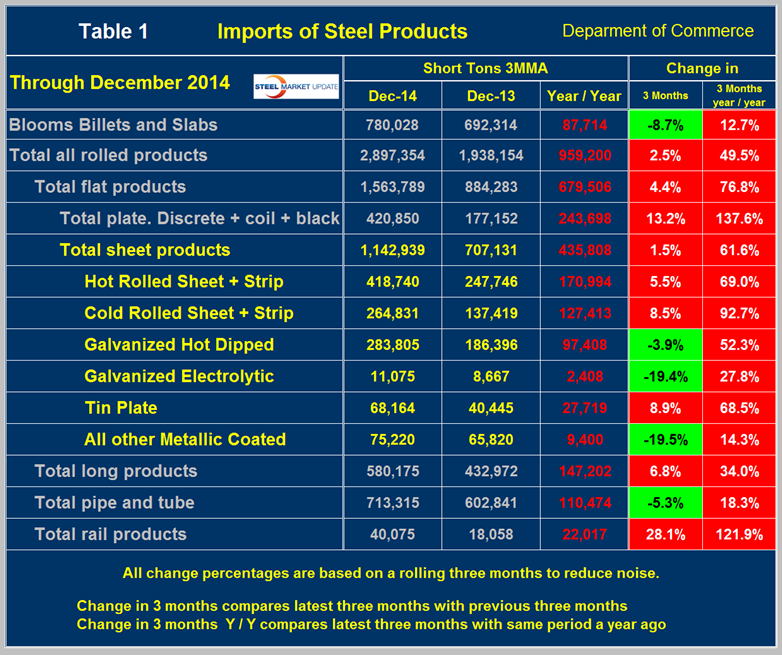

Table 1 provides a detailed import analysis and compares the average monthly tonnage of the three months through December, with both the same period last year and with July through September 2014. The total tonnage of hot worked products averaged 2,897,354 tons per month in three months through December, up by 49.5 percent year over year and by 2.5 percent in concurrent three month periods. Year over year semi-finished imports were up by 12.7 percent, flat rolled products were up by 76.8 percent, long products fared better, up by 34.0 percent. Table 1 shows the tonnage and percent change for all the major product groups and for sheet products in detail. The average monthly tonnage of sheet products in three months through December increased by 435,808 tons or 61.6 percent year over year.