Prices

July 8, 2015

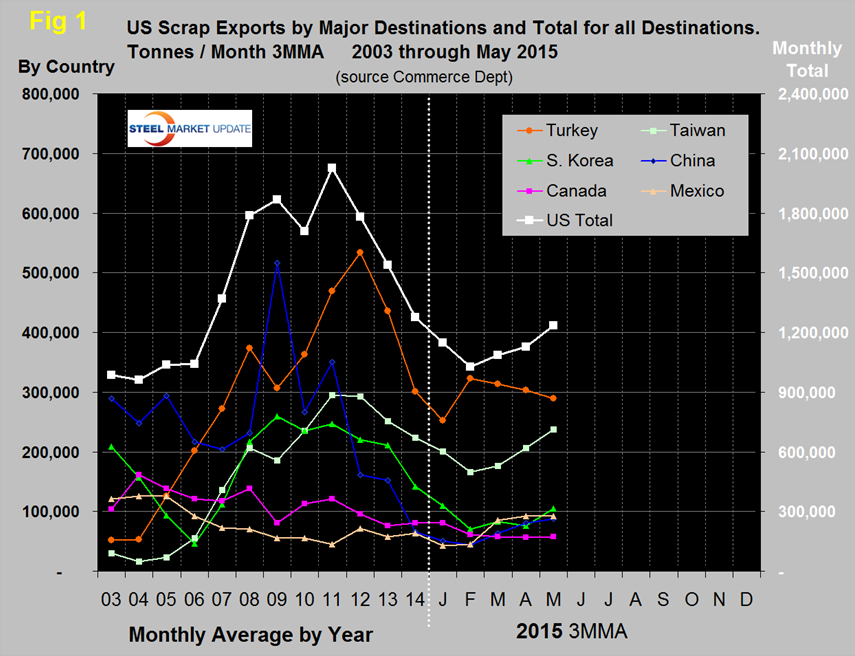

Scrap Exports Down 9.3 Percent Year to Date

Written by Peter Wright

In the first five months of this year bulk scrap exports were 5,724,456 tonnes for an annual rate of 13,741,000 tonnes, down by 9.3 percent from the first five months of last year. The tonnages shown in Figure 1 are based on three month moving averages for 2015 and on the twelve month monthly average for previous years.

The graph shows that exports declined for three consecutive years, 2012 through 2014 and continued through January and February this year. March saw a trend reversal that continued through May. In the twelve months of 2014, scrap exports totaled 15,308,000 tonnes, down by 17.1 percent from the same period in 2013. Reports in the American Metal Market on June shipments were depressed. On June 11th it was reported that Turkish buyers had booked no cargoes in the last two weeks due to a price standoff between East Coast dealers and Turkish buyers. On June 25th, “Turkey has been out of the US market for six weeks. Europe has sold two cargoes to Turkey in that time frame.

In the single month of May, Turkey was the major destination with 349,917 tonnes, followed by Taiwan with 218,588 tonnes and India with 172,765 tonnes. Turkey’s buy is still low by historical standards and continues to be depressed by the depreciated values of the Euro and Ruble. Figure 1 is calculated on a 3MMA basis and by that reckoning Turkey’s purchases declined in March, April and May. Shipments to the Far East through the first five months were up by 13.8 percent from last year. YTD through May exports to Canada were down by 25.4 percent and to Mexico were up by 8.8 percent. Exports to India have almost tripled y/y and to South Korea have been almost cut in half. China has received almost the same volume year over year.

Shipments to secondary buying nations totaled 124,735 tonnes in May. Of this 33,343 tonnes shipped to Pakistan, 32,000 tonnes to Peru and 40,700 to Saudi Arabia.

Scrap export prices are reported by the AMM every Tuesday for an 80:20 mix of #1 and #2 heavy melt in US $ per tonne FOB New York and Los Angeles for bulk tonnage sales. The price on the East coast collapsed by $36/gross ton on July 1st to $235. The West coast price was unchanged at $243 week on week but was down by $12 since June 3rd. The price of Chicago shredded was up by $30 in June to $275. Chicago #1 busheling was unchanged in May and was also up $30 in June to $270. Note; Busheling was $5 cheaper than shredded in both May and June.