Prices

July 30, 2015

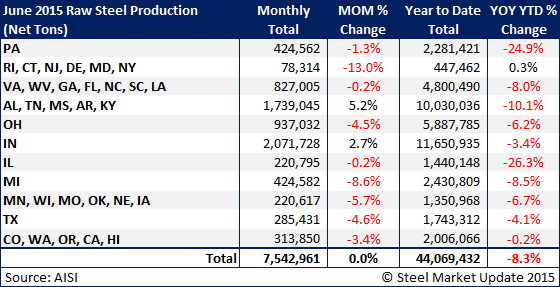

June Raw Steel Production Flat & Capacity Utilization Hits 74.4%

Written by Brett Linton

The American Iron & Steel Institute (AISI) recently reported final raw steel production estimates for the month of June 2015. The monthly estimates are different than the weekly estimates we report in our Tuesday issues; the AISI bases the monthly estimates on 75 percent of the domestic mills reporting vs. only 50 percent for the weekly estimates.

Total raw steel production for the month of June was reported to be 7,542,961 net tons with 4,604,391 tons being produced by electric arc furnaces (EAF) and 2,938,570 tons produced by blast furnaces. June raw steel production was reported by the AISI to have been 1,518 tons or 0.02 percent lower than the previous month.

Compared to the first six months of 2014, 2015 YTD production is down 8.3 percent to 44,069,432 tons. The table below shows that 10 of the 11 state-groups in the yearly comparison were reported as down.

The capacity utilization rate for the month of June 2015 was reported to be 74.4 percent, up from 72.1 percent in May but down from 78.5 percent in June 2014. However, our readers need to be aware that the AISI adjusted the available capacity figure from May to June: May’s production capability was 10.5 million tons, while June capacity was 10.1 million tons.

SMU Note: An interactive graphic of our raw steel production history can be seen in the Analysis section of our website here. If you need help logging into the website or navigating through it, please contact us at info@SteelMarketUpdate.com or 800-432-3475.