Prices

January 12, 2016

November Final Imports & December Expectations

Written by John Packard

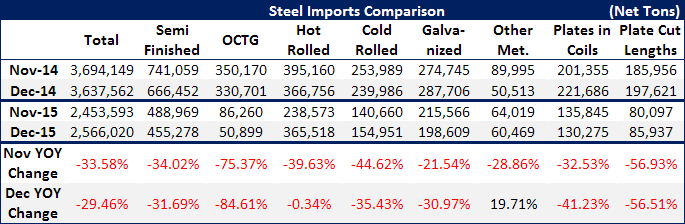

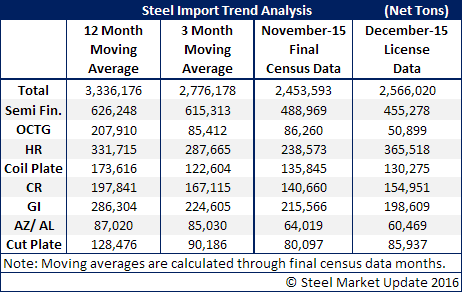

The U.S. Department of Commerce announced the final census data for foreign steel imports for the month of November. November imports were 2,453,593 net tons (not metric tons as we have already made the conversion from the US DOC charts) which is significantly below both the 3 month and 12 month moving averages (see table below). The November total is 33.58 percent lower in 2015 than it was the previous year.

December imports, based on license data collected through the 6th of January, are expected to be 2.5 million net tons or very close to the November number.

We thought our readers would enjoy looking at these two months – November 2015 and December 2015 and comparing them against the same two months in 2014. This will give you a sense of the changes the market has been going through and what might be in store for the domestic mills as we move into 2016 (assumption are inventories are declining on virtually all flat rolled products):