Prices

December 6, 2016

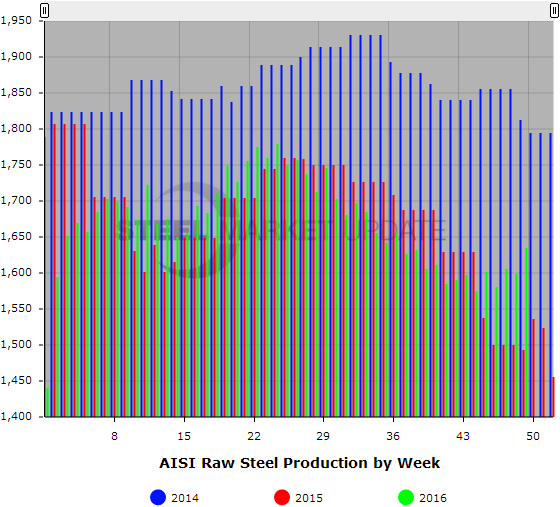

Weekly Raw Steel Production: Picking Back Up or Just A Bounce?

Written by Brett Linton

For the week ending December 3, 2016, the American Iron & Steel Institute (AISI) estimated the U.S. steel industry produced 1,635,000 net tons of raw steel, a 2.3 percent increase over the previous week and a 9.5 percent increase over the same week one year ago (revised). The estimated capacity utilization rate is 68.9 percent, up from 67.4 percent last week and up from 62.5 percent this time last year.

This is the highest production level seen since the week ending September 3, 2016 when 1,656,000 tons were produced at a capacity utilization rate of 70.8 percent. This is the highest capacity utilization rate since he week ending October 1, 2016 when 1,611,000 tons were produced at a capacity utilization rate of 68.9 percent.

Estimated total raw steel produced for 2016 YTD is reported to be 81,376,000 tons, down 1.3 percent from the 82,481,000 tons produced during the same period in 2015. The average capacity utilization rate for 2016 YTD is estimated to be 70.9 percent, up from 70.8 for 2015 YTD.

Week-over-week changes per district are as follows: Northeast at 199,000 tons, down 3,000 tons. Great Lakes at 652,000 tons, up 22,000 tons. Midwest at 154,000 tons, down 4,000 tons. South at 563,000 tons, up 16,000 tons. West at 67,000 tons, up 6,000 tons. Total production was 1,635,000 tons, up 37,000 tons.

Note that the AISI estimates capability for Q4 2016 at approximately 31.2 million tons compared to 31.4 million tons for the same period last year and 30.7 million tons for Q3 2016.

About Weekly Raw Steel Production Data

The weekly raw steel production tonnage provided by the AISI is estimated. The figures are compiled from weekly production tonnage provided by 50 percent of the domestic producers combined with monthly production data for the remainder. Therefore, this report should be used primarily to assess production trends. The monthly AISI production report provides a more detailed summary of steel production based on data supplied by companies representing over 75 percent of U.S. production capacity.

SMU Note: Below is a graphic showing the weekly raw steel production history. To use the graphs interactive capabilities, you must view it on our website. You can do this by clicking here. If you need help navigating the website or need to know your login information, contact us at info@SteelMarketUpdate.com or by calling 800-432-3475.