Market Data

April 17, 2017

Shipments and Supply of Sheet Products through February 2017

Written by Peter Wright

This report summarizes total steel supply from 2003 through February 2017 and year on year changes. It then compares domestic mill shipments with total supply to the market. It quantifies market direction by product and enables a side by side comparison of the degree to which imports have absorbed demand. Sources are the American Iron and Steel Institute and the Department of Commerce with analysis by SMU.

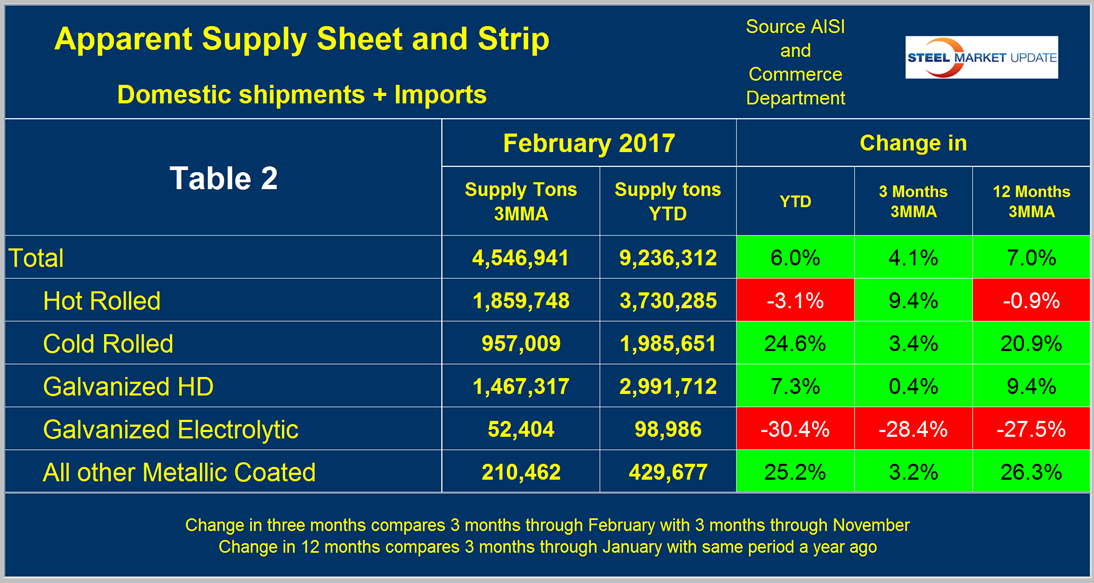

Table 1 describes both apparent supply and mill shipments of sheet products (shipments includes exports) side by side as a three month average through February, for both 2016 and 2017.

Apparent Supply

Apparent supply is a proxy for market demand. Comparing these two time periods total supply to the market was up by 7.0 percent and shipments were also up by 7.0 percent. The fact that the changes in supply and shipments were the same overall means that imports did not influence the market balance compared to the same three months last year. This was not the case with individual products. Table 1 breaks down the total into product detail and it can be seen that supply grew by more than shipments for every product except hot rolled. Electro-galvanized is an odd ball because it has net exports.

A review of supply and shipments separately for individual sheet products is given below.

Apparent Supply is defined as domestic mill shipments to domestic locations plus imports. In the three months through February 2017 the average monthly supply of sheet and strip was 4.547 million tons, up by 7.0 percent year over year compared to the same period ending February 2016. In the three months through February compared to the 3 months through November, supply was up by 4.1 percent. The short term increase (3 months) compared to the long term improvement (12 months) means that through February momentum was negative. This was probably a seasonal effect. There is no seasonal manipulation of any of these numbers but by definition, y/y comparisons have seasonality removed but 3m/3m comparisons do not. Table 2 shows the change in supply by product on this basis through February. Momentum was negative for all products except hot rolled coil.

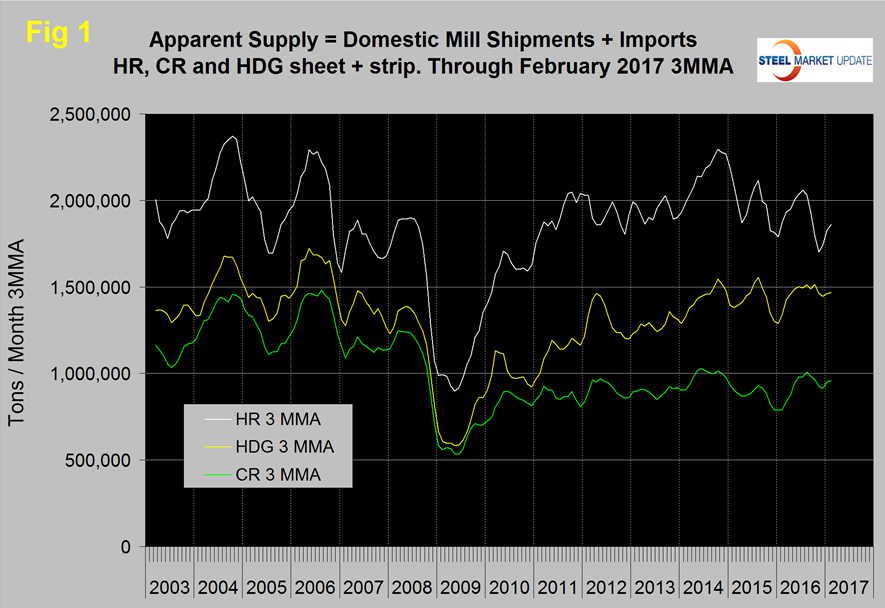

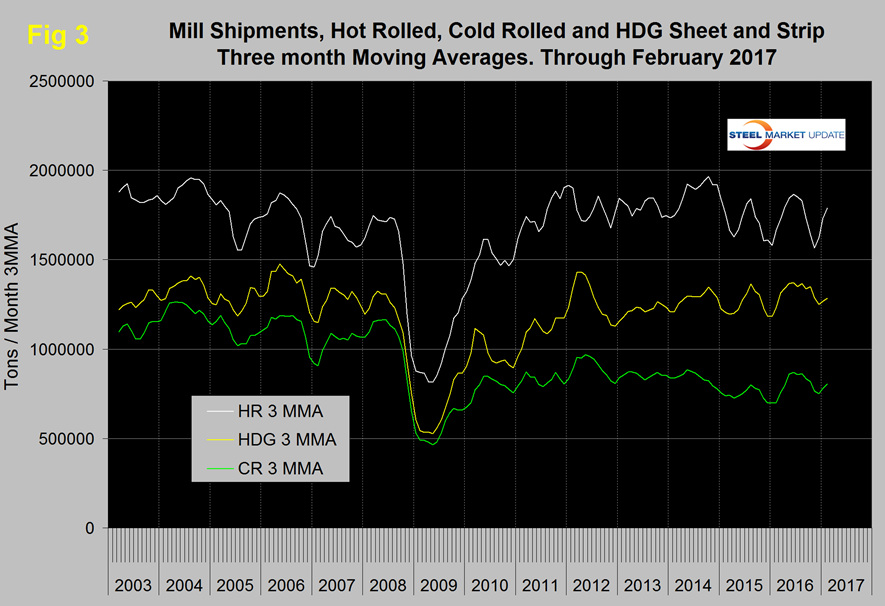

Figure 1 shows the long term supply picture for the three major sheet and strip products, HR, CR and HDG since January 2003 as three month moving averages.

All three products had an uptick in supply this year on a 3MMA basis.

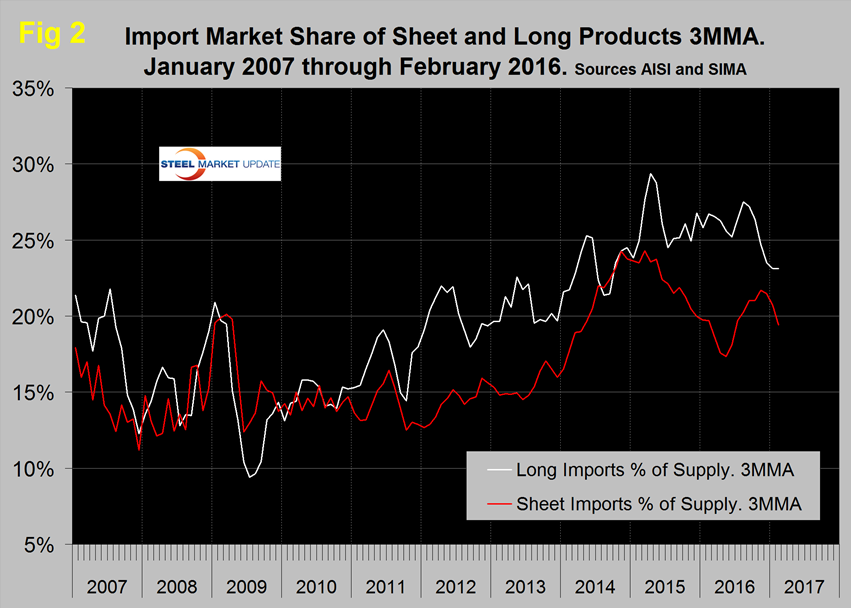

Figure 2 shows import market share of sheet products and includes long products for comparison.

Based on a 3MMA, the import market share of sheet products declined from 21.7 percent in November to 19.4 percent in February which was the lowest share since June. Long product import market share is now below its trend since 2010 and in 3 months through February was 23.1 percent.

Mill Shipments

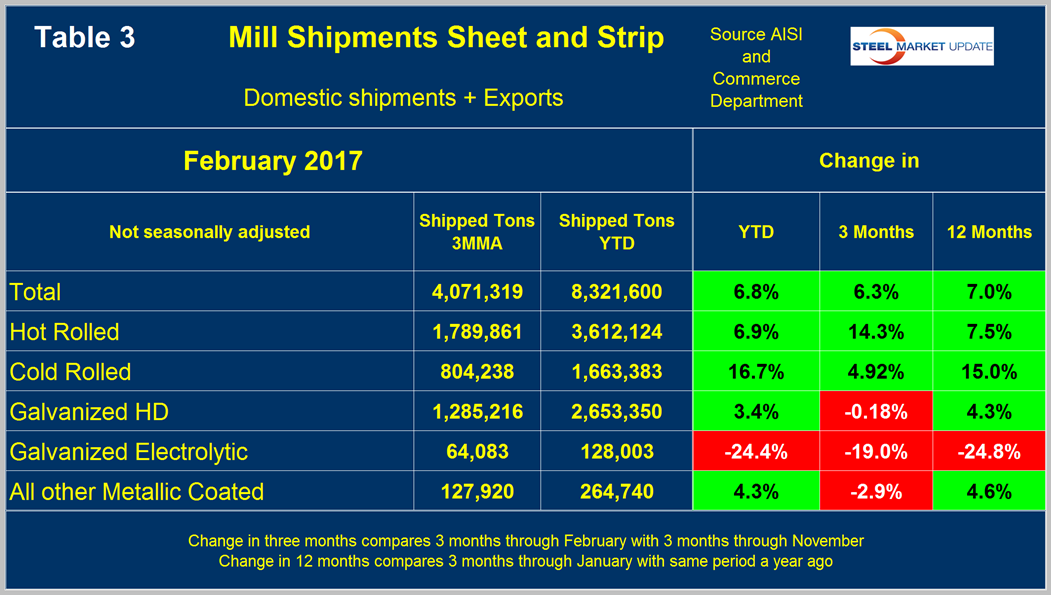

Table 3 shows that total shipments of sheet and strip products including hot rolled, cold rolled and all coated products were up by 7.0 percent in 3 months through February year over year and up by 6.3 percent comparing three months through February with three months through November.

These February/November numbers are close enough to say that shipments had no momentum in either direction in the February data. This balancing act was a combination of positive momentum in HRC and negative in the other sheet products. Figure 3 puts the shipment results for the three main products into the long-term context since January 2003.

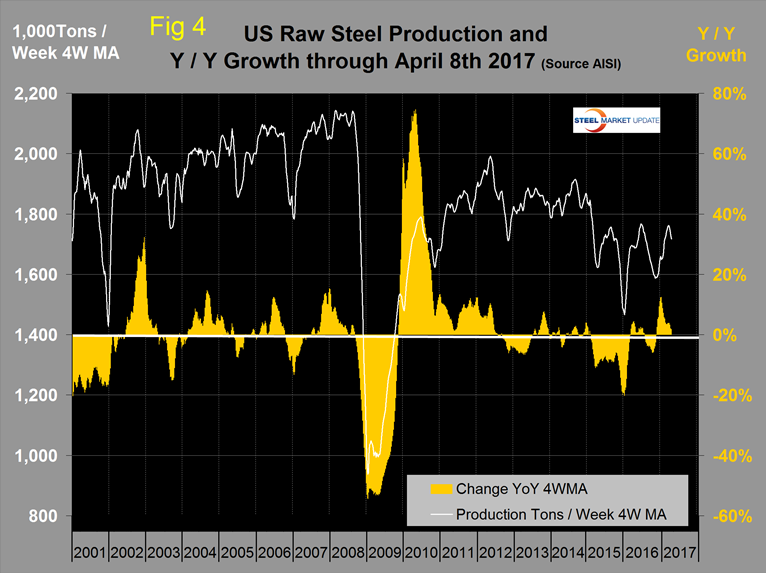

SMU Comment: A problem with this data is that it’s now well into April and the latest data we have for shipments and supply is for February. The AISI puts out weekly data for crude steel production the latest for which was w/e April 8th. This provides the most current data for steel mill activity. Figure 4 shows the y/y change in weekly crude output on a four week moving average basis.

Growth became positive year/year in w/e November 19th and has been positive for the last 21 weeks. Based on the strength of the economic indicators analysis that SMU performs and our proprietary measure of buyer sentiment, we are expecting demand for sheet products to continue to increase through the 3rd quarter.