Prices

August 22, 2017

SMU Price Ranges & Indices: Prices Move Higher

Written by John Packard

Last week, the flat rolled and plate steel mills announced price increases. Steel Market Update has seen prices rise in the mill spot markets (not in the service center spot markets) by $10 to $20 per ton. We are hearing from steel buyers (and a couple of mills) that the number of spot orders have slowed. As one steel mill put it to SMU earlier today, “…We did increase price and, as expected, not much action yet first couple days of the week. But costs are still exploding. So, I would rather sell less and make more money than sell more and get killed.”

Here is how we see prices this week:

Hot Rolled Coil: SMU price range is $610-$640 per ton ($30.50/cwt-$32.00/cwt) with an average of $625 per ton ($31.25/cwt) FOB mill, east of the Rockies. The lower end of our range increased $20 per ton compared to one week ago, while the upper end remained the same. Our overall average is up $10 per ton compared to last week. Our price momentum on hot rolled steel is pointing to Neutral indicating prices are expected to remain steady over the next 30-60 days.

Hot Rolled Lead Times: 3-6 weeks

Cold Rolled Coil: SMU price range is $790-$840 per ton ($39.50/cwt-$42.00/cwt) with an average of $815 per ton ($40.75/cwt) FOB mill, east of the Rockies. The lower end of our range increased $40 per ton compared to last week, while the upper end remained the same. Our overall average is up $20 per ton compared to one week ago. Our price momentum on cold rolled steel is pointing to Neutral indicating prices are expected to remain steady over the next 30-60 days.

Cold Rolled Lead Times: 4-8 weeks

Galvanized Coil: SMU base price range is $39.50/cwt-$42.00/cwt ($790-$840 per ton) with an average of $40.75/cwt ($815 per ton) FOB mill, east of the Rockies. The lower end of our range increased $20 per ton compared to one week ago, while the upper end remained the same. Our overall average is up $10 per ton compared to last week. Our price momentum on galvanized steel is pointing to Neutral indicating prices are expected to remain steady over the next 30-60 days.

Galvanized .060” G90 Benchmark: SMU price range is $868-$918 per net ton with an average of $893 per ton FOB mill, east of the Rockies.

Galvanized Lead Times: 4-10 weeks

Galvalume Coil: SMU base price range is $40.50/cwt-$42.00/cwt ($810-$840 per ton) with an average of $41.25/cwt ($825 per ton) FOB mill, east of the Rockies. The lower end of our range increased $20 per ton compared to last week, while the upper end remained the same. Our overall average is up $10 per ton compared to one week ago. Our price momentum on Galvalume steel is pointing to Neutral indicating prices are expected to remain steady over the next 30-60 days.

Galvalume .0142” AZ50, Grade 80 Benchmark: SMU price range is $1,101-$1,131 per net ton with an average of $1,116 per ton FOB mill, east of the Rockies.

Galvalume Lead Times: 5-8 weeks

Plate: SMU price range is $680-$740 per ton ($34.00/cwt-$37.00/cwt) with an average of $710 per ton ($35.50/cwt) FOB delivered. The lower end of our range increased $10 per ton compared to one week ago, while the upper end increased $20 per ton. Our overall average is up $15 per ton compared to last week. Our price momentum on plate steel is pointing to Neutral indicating prices are expected to remain steady over the next 30-60 days.

Plate Lead Times: 4-6 weeks

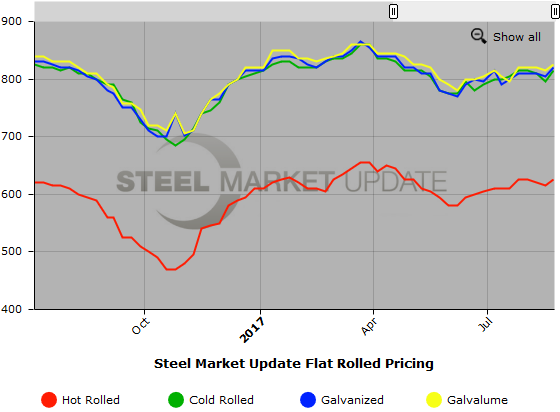

SMU Note: Below is a graphic showing our hot rolled, cold rolled, galvanized, and Galvalume price history. We will add plate prices to this graph once we have gathered a few months of data. To use the graph’s interactive capabilities, you must view it on our website here. If you need help navigating the website or need to know your login information, contact us at info@SteelMarketUpdate.com or by calling 800-432-3475.

Written by John Packard, John@SteelMarketUpdate.com