Analysis

October 6, 2017

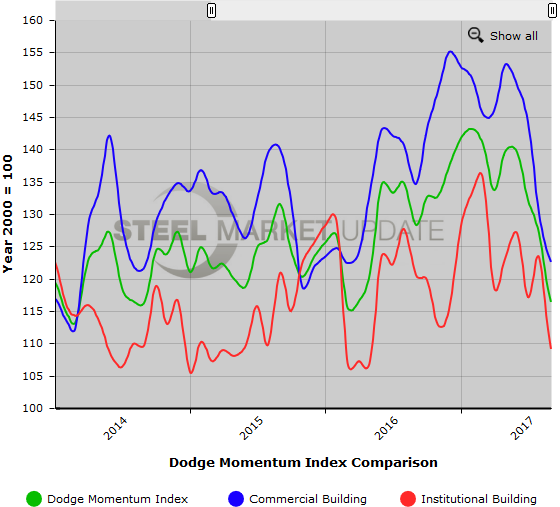

Dodge Index Declines for Fourth Month

Written by Sandy Williams

The Dodge Momentum Index slumped 8.4 percent to a reading of 116.4 in September. The index, published by Dodge Data & Analytics, is a monthly measure of the first (or initial) report for nonresidential building projects in planning, which has been shown to lead construction spending for nonresidential buildings by a full year.

Planning for institutional building plunged 11.5 percent, while planning for commercial building fell 6.1 percent. August marks the fourth month of decline for the index, although Dodge said it should not be interpreted as a turn in the building market.

“Prior to the previous peak of the Momentum Index in January 2008 it had suffered similar significant declines, only to rebound and post strong gains in subsequent months in line with overall economic growth,” wrote Dodge. “Similarly, the Momentum Index posted healthy gains from late 2016 through early 2017. Economic growth remains solid, and building market fundamentals are supportive of further growth in construction activity.”

Ten projects entered the planning phase in September with a value of $100 million or more.

Below is a graph showing the history of the Dodge Momentum Index. You will need to view the graph on our website to use its interactive features; you can do so by clicking here. If you need assistance logging into or navigating the website, please contact our office at 800-432-3475 or info@SteelMarketUpdate.com.