Market Data

March 8, 2018

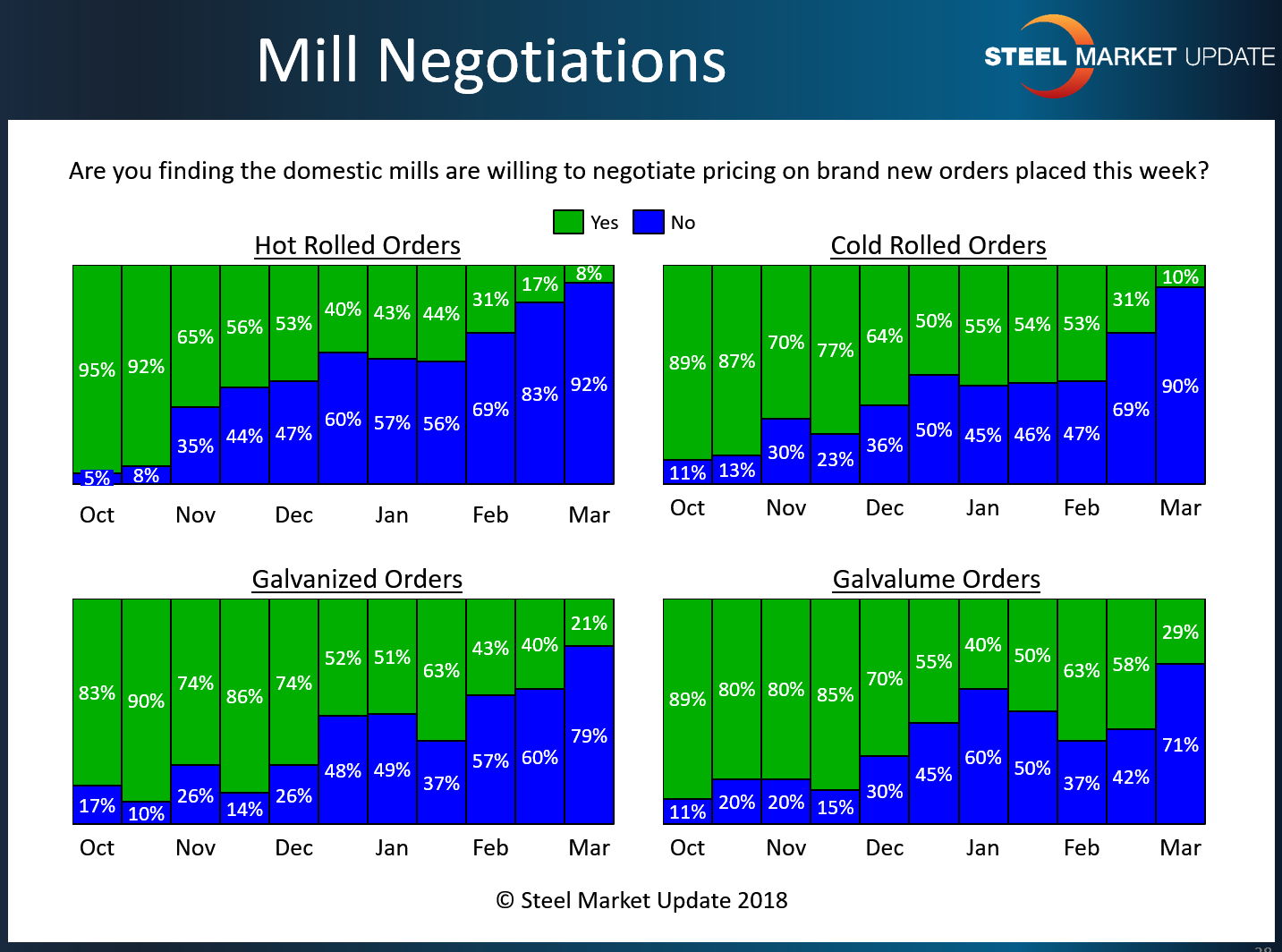

Steel Mill Negotiations: Mills Holding the Line

Written by Tim Triplett

With foreign steel offers largely on hold as the market awaits President Trump’s final decision on steel tariffs, domestic steel mills are in a strong bargaining position and are taking full advantage of it. Nine out of 10 steel buyers responding to Steel Market Update’s market trends questionnaire this week say the mills are unwilling to negotiate on hot rolled and cold rolled orders, and nearly as many are holding the line on galvanized and Galvalume.

By market segment, 92 percent of SMU respondents said the mills are holding firm on hot rolled steel orders, while only 8 percent have found mills willing to negotiate. That compares to 83 percent holding the line and 17 percent open to price negotiations on hot roll two weeks ago.

In the cold rolled segment, only 10 percent said they have found some mills willing to talk price, while the vast majority (90 percent) reported mill prices on cold rolled as non-negotiable.

In the galvanized sector, about 79 percent of respondents said the mills are now standing firm on galvanized prices, while 21 percent said some mills are still open to negotiation on coated products. That’s nearly a 20-point shift from just two weeks ago when 60 percent said mills were holding the line.

Negotiations have tightened considerably for Galvalume. Two weeks ago, the majority of buyers reported that mills were still open to price discussions. Today, 71 percent said mills are unwilling to compromise on Galvalume prices.

Buyers tell SMU that only a few mills are flexible on price, depending on the product, and only on large tonnages.

Note: SMU surveys active steel buyers twice each month to gauge the willingness of their steel suppliers to negotiate pricing. The results reflect current steel demand and changing spot pricing trends. SMU provides our members with a number of ways to interact with current and historical data. To see an interactive history of our Steel Mill Negotiations data, visit our website here.