Prices

May 22, 2018

SMU Price Ranges & Indices: Mills Making a Move to Push Prices Higher?

Written by John Packard

A large manufacturing company that buys a tremendous amount of hot rolled in the spot markets explained to SMU what they were seeing out of the domestic steel mills this week: “The market is relatively calm at the moment. Steel prices have been hovering in the same range for the last four to five weeks. We are starting to see more mills trying to push prices higher this week. Currently, we are being quoted HRC base of $880 to $920. Lead time is July with most mills.” We are seeing that same price pressure from a number of our sources, not everyone, but more than a handful. Steel buyers are telling SMU that there will not be any more price increase announcements due to “bad optics” in light of the Section 232 tariffs, etc. Steel buyers should expect the domestic mills to at least make a run at higher prices.

In the meantime, SMU’s Price Momentum Indicator continues to point sideways (Neutral) on flat rolled and up (Higher) on plate.

Here is how we see prices this week:

Hot Rolled Coil: SMU price range is $880-$920 per ton ($44.00/cwt-$46.00/cwt) with an average of $900 per ton ($45.00/cwt) FOB mill, east of the Rockies. The lower end of our range rose $30 per ton compared to one week ago, while the upper end rose $10. Our overall average is up $20 per ton compared to last week. Our price momentum on hot rolled steel is now pointing to Neutral indicating prices are expected to remain steady over the next 30-60 days.

Hot Rolled Lead Times: 4-8 weeks

Cold Rolled Coil: SMU price range is $980-$1,030 per ton ($49.00/cwt-$51.50/cwt) with an average of $1,005 per ton ($50.25/cwt) FOB mill, east of the Rockies. The lower end of our range fell $10 per ton compared to last week, while the upper end remained the same. Our overall average is down $5 per ton compared to one week ago. Our price momentum on cold rolled steel is now pointing to Neutral indicating prices are expected to remain steady over the next 30-60 days.

Cold Rolled Lead Times: 5-8 weeks

Galvanized Coil: SMU base price range is $49.00/cwt-$52.00/cwt ($980-$1,040 per ton) with an average of $50.50/cwt ($1,010 per ton) FOB mill, east of the Rockies. Both the lower and upper ends of our range declined $10 per ton compared to one week ago. Our overall average is down $10 per ton compared to last week. Our price momentum on galvanized steel is now pointing to Neutral indicating prices are expected to remain steady over the next 30-60 days.

Galvanized .060” G90 Benchmark: SMU price range is $1,066-$1,126 per net ton with an average of $1,096 per ton FOB mill, east of the Rockies.

Galvanized Lead Times: 5-12 weeks

Galvalume Coil: SMU base price range is $50.50/cwt-$52.50/cwt ($1,010-$1,050 per ton) with an average of $51.50/cwt ($1,030 per ton) FOB mill, east of the Rockies. Both the lower and upper ends of our range remained the same compared to last week. Our overall average is unchanged compared to one week ago. Our price momentum on Galvalume steel is now pointing to Neutral indicating prices are expected to remain steady over the next 30-60 days.

Galvalume .0142” AZ50, Grade 80 Benchmark: SMU price range is $1,301-$1,341 per net ton with an average of $1,321 per ton FOB mill, east of the Rockies.

Galvalume Lead Times: 6-10 weeks

Plate: SMU price range is $960-$1,020 per ton ($48.00/cwt-$51.00/cwt) with an average of $990 per ton ($49.50/cwt) FOB delivered. The lower end of our range rose $30 per ton compared to one week ago, while the upper end jumped up $50 per ton. Our overall average is up $40 compared to last week. Our price momentum on plate steel is pointing to Higher indicating prices are expected to rise over the next 30-60 days.

Plate Lead Times: 5-8 weeks, allocation/controlled order entry

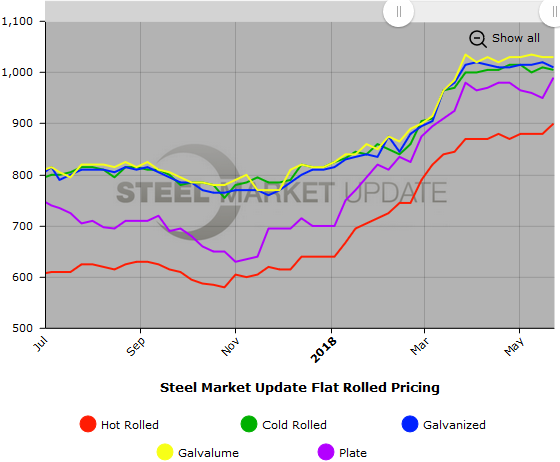

SMU Note: Below is a graphic showing our hot rolled, cold rolled, galvanized, Galvalume, and plate price history. This data is available here on our website with our interactive pricing tool. Note that plate prices are not yet available on our website, but we are in the process of adding that dataset. If you need help navigating the website or need to know your login information, contact us at info@SteelMarketUpdate.com or 800-432-3475.