Market Data

May 31, 2018

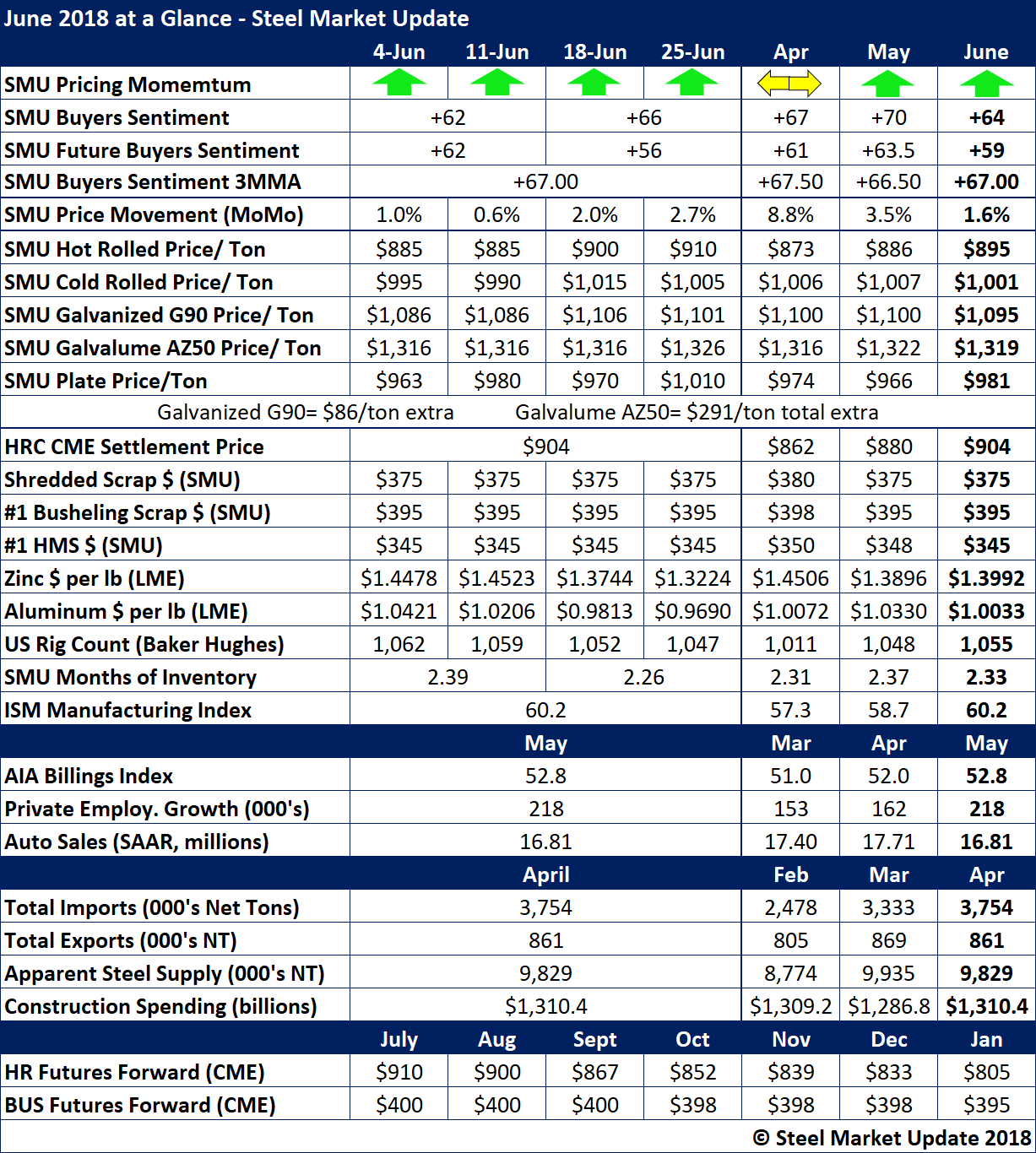

June 2018 at a Glance

Written by Tim Triplett

In the table below, Steel Market Update provides a snapshot of flat rolled steel pricing, commodities that affected steel prices, and economic data of importance to the flat rolled steel industry in June.

Looking back at the past month, SMU’s Pricing Momentum Indicator continued to point higher as the domestic mills reacted to the Trump administration tariffs on steel imports, pushing the price of hot rolled over $900 per ton. The price of cold rolled topped $1,000, while galvanized was near $1,100 a ton, about the same as in April and May.

Buyers’ sentiment declined a bit in June over the uncertainty on the trade front, but SMU’s Steel Buyers Sentiment Index remained at very optimistic levels. Measured as a single data point, buyers’ sentiment averaged +64, down from +70 in May. Future buyers’ sentiment was at +59, down from +63.5 the prior month. The three-month moving average has shown little change in buyers’ attitudes since April, however.

Steel demand remained positive in June. The Institute for Supply Management’s Manufacturing Index hit 60.2, up from 57.3 in April and 58.7 in May (any reading above 50.0 indicates growth). ISM’s monthly survey of corporate purchasing executives defied expectations of a summer slowdown. In the energy sector, the U.S. rig count reached 1,055, up by 44 rigs from April, which is good news for suppliers of oil country tubular goods.

Industry inventory in June remained at a lean level around 2.3 months of supply as service centers were conservative in their purchasing in the uncertain pricing and political environment.

Refer to the chart below for other key economic data points.

To see a history of our monthly review tables, visit our website.